Payment Tokenization and Chargebacks: A Guide

Why tokenized transactions still trigger disputes — and what eCommerce operators can do to protect revenue

Learn why payment tokenization reduces fraud but doesn’t eliminate chargeback liability. This guide explains how dispute flows work with tokens and outlines operational steps to protect your revenue.

TL;DR

- Tokenization reduces fraud but not chargebacks – Mobile wallets like Apple Pay protect card data from theft, but merchants still carry liability for disputes related to friendly fraud, product issues, and billing confusion.

- 3D Secure is your liability shift lever – Activating 3DS on tokenized transactions moves fraud-coded chargeback liability from your account to the issuing bank, often with minimal friction for the customer.

- Prevention beats representment – Pre-dispute alerts, clear billing descriptors, and accessible customer service resolve more chargebacks (at lower cost) than fighting disputes after they’re filed.

- Evidence capture must be automatic – Build transaction records, delivery confirmations, and customer communications into your fulfillment workflow so representment packages are ready before you need them.

- Your payment processor is a strategic partner – Evaluate processors on chargeback defense tools, reporting clarity, and support responsiveness, not just transaction fees. The right partner prevents losses that far exceed any per-transaction cost difference.

Guide Orientation: What This Guide Covers and Who It’s For

This guide addresses a specific blind spot in eCommerce payments: the gap between payment tokenization as a fraud prevention tool and the merchant liability that persists even after you adopt it. If you run or manage an online store processing mobile wallet payments (Apple Pay, Google Pay, or similar), this is for you.

By the end, you’ll understand exactly why tokenized transactions still generate chargebacks, how dispute flows differ when tokens are involved, and what operational steps you can take to protect revenue without overhauling your entire payment stack.

This guide does not cover the deep technical architecture of tokenization (DPANs, MPANs, cryptograms). It does not address enterprise-level payment orchestration. Instead, it translates payment security concepts into cash flow consequences and actionable decisions for small-to-midsize eCommerce operators managing 10 to 50 employees.

Why Protecting Revenue from Chargeback Rates Matters Now

Mobile wallet adoption is accelerating. Global token adoption increased by 6% from Q1 2024 to Q1 2025, and every major card network is pushing tokenized checkout as the default. For eCommerce operators, this creates an uncomfortable paradox: your transactions are technically more secure, but your liability exposure hasn’t decreased proportionally.

Here’s why. Tokenization replaces sensitive card data with a unique token, which means stolen card numbers from breaches are less useful to fraudsters. Research shows tokenization reduced fraud rates from 2.5% to 0.8%, a 68% decrease. That’s a real improvement. But fraud and chargebacks are not the same thing.

A customer can still claim they didn’t authorize a purchase, didn’t receive the product, or received something materially different from what was described. Those disputes land on your account regardless of whether the payment was tokenized. As Dr. Sarah Chen of Nuvei noted in a 2023 report, “While tokenization slashes fraud rates by over 60%, it does not absolve merchants from chargeback liability for customer disputes, a critical gap many only discover post-dispute.”

Merchant losses from online payment fraud are forecast to exceed $91 billion by 2028. The cost of assuming tokenization has solved your chargeback problem is measured in real dollars deducted from your account, fees stacked on top, and the risk of landing in a card network monitoring program that makes every future transaction more expensive.

Core Concepts: Payment Tokenization, Chargebacks, and Merchant Liability

What Tokenization Actually Does (and Doesn’t Do)

When a customer pays with Apple Pay or another mobile wallet, the card network replaces their actual card number with a device-specific token. This token is useless if intercepted because it can only be used by that specific device, for that specific merchant relationship. This is why tokenization saved approximately $650 million in fraud prevention globally in the past year alone.

But tokenization is a data security mechanism, not a dispute resolution mechanism. It prevents card-not-present fraud that originates from stolen credentials. It does not prevent a legitimate cardholder from filing a chargeback.

The Chargeback Liability Gap

Chargebacks fall into three broad categories: true fraud (unauthorized use of stolen payment credentials), friendly fraud (the cardholder made the purchase but disputes it anyway), and merchant error (shipping mistakes, billing descriptor confusion, product quality issues). Tokenization addresses the first category effectively. It has almost no impact on the second and third.

This distinction matters because friendly fraud and merchant error account for a significant share of disputes in eCommerce. When a customer pays via Apple Pay and later claims the item never arrived, the chargeback hits your account the same way it would with a traditional card payment. The token doesn’t help you win that dispute.

Why Mobile Wallets Complicate Dispute Matching

Tokenized transactions can create an additional operational challenge: matching a chargeback notification to the original order. Because the token differs from the card number, and because mobile wallet transactions sometimes display differently in your payment processor’s dashboard, identifying which order triggered the dispute can take longer. That delay compresses your response window and reduces your odds of a successful representment.

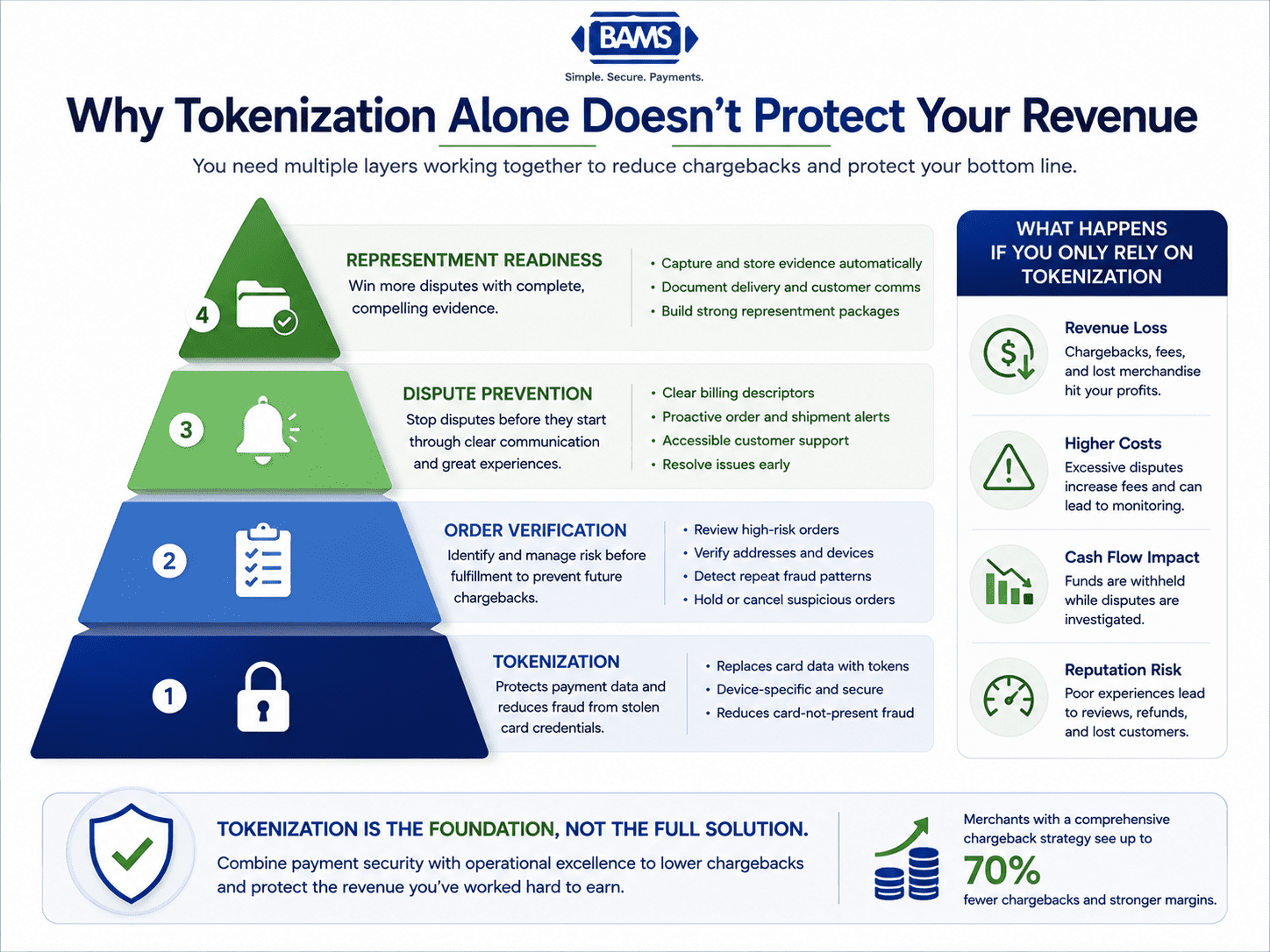

The Framework: Four Layers of Revenue Protection

Tokenization is only the foundation of payment security. Merchants need multiple operational layers to prevent chargebacks and protect revenue.

Protecting revenue as mobile wallet adoption grows requires a layered approach. No single tool or policy eliminates chargeback risk. Instead, think of your defense as four interconnected layers:

- Layer 1: Transaction Authentication — Shift liability before the sale completes

- Layer 2: Order Verification — Confirm legitimacy between authorization and fulfillment

- Layer 3: Dispute Prevention — Intercept chargebacks before they become formal disputes

- Layer 4: Representment Readiness — Build the evidence package to win disputes you can’t prevent

Each layer reduces a different type of risk. Skipping a layer doesn’t break the system entirely, but it creates a predictable gap that chargebacks will exploit. The steps below walk through each layer with specific actions you can take.

Step-by-Step: Building Your Revenue Protection System

Step 1: Activate 3D Secure for Liability Shift

Objective: Move chargeback liability from your account to the card issuer for fraud-coded disputes.

3D Secure (3DS) is an authentication protocol that adds a verification step during checkout. When a customer completes 3DS authentication, the liability for fraud chargebacks shifts to the issuing bank. This is the single most effective way to protect yourself from unauthorized-use disputes on tokenized transactions.

Most modern implementations (3DS2) are low-friction. The issuing bank evaluates risk signals behind the scenes and only challenges the customer with a verification prompt when the transaction looks unusual. For many mobile wallet transactions, the biometric authentication built into Apple Pay or Google Pay satisfies the 3DS requirement automatically, meaning your customer experience stays smooth.

As Mark Thompson, VP of Merchant Risk Solutions at Mastercard, has stated: “Tokenization is the cornerstone of fraud prevention, but merchants must layer liability-shift solutions like 3D Secure to avoid bearing the financial burden of fraud-coded chargebacks.”

Anti-patterns to avoid: Don’t assume mobile wallet biometrics automatically trigger a liability shift. The shift depends on your gateway’s 3DS configuration and the card network’s specific rules. Verify with your payment processor that 3DS is active and returning successful authentication results on mobile wallet transactions.

Success indicators: You should see authentication data (ECI indicators) attached to your tokenized transactions. Your processor’s reporting should show a clear distinction between liability-shifted and non-shifted transactions.

Step 2: Tighten Order Verification Before Fulfillment

Objective: Catch suspicious orders between payment authorization and shipment, before you lose both the product and the revenue.

Tokenization tells you the payment credential is valid. It doesn’t tell you whether the person placing the order intends to keep the product, whether the shipping address matches the cardholder’s profile, or whether the order pattern looks normal for your business.

Build a simple verification workflow for orders that trigger risk signals: unusually high order values, new customer accounts with expedited shipping, multiple orders to the same address from different payment methods, or shipping addresses that differ significantly from billing addresses. You don’t need an enterprise fraud platform for this. A checklist and a brief manual review process for flagged orders can prevent a large share of preventable losses.

For merchants processing a high volume of Apple Pay transactions, pay attention to orders where the device token is new but the shipping address has appeared in previous disputes. This pattern often indicates a repeat-offender testing whether tokenized payments bypass your existing fraud rules.

Anti-patterns to avoid: Don’t auto-approve every tokenized transaction because it “passed” biometric authentication. Biometrics confirm the device holder’s identity, not their intent. Also, don’t create so much friction that legitimate customers abandon their carts. The goal is targeted verification, not blanket suspicion.

Success indicators: Your fulfillment team has a clear, documented process for reviewing flagged orders. You can measure the percentage of flagged orders that result in cancellation versus successful delivery.

Step 3: Deploy Pre-Dispute Alerts and Deflection

Objective: Resolve customer complaints before they escalate to formal chargebacks.

The most cost-effective chargeback is the one that never happens. Pre-dispute alert services (offered through networks like Verifi and Ethoca) notify you when a cardholder contacts their bank to initiate a dispute, giving you a narrow window to issue a refund before the chargeback is formally filed. This avoids the chargeback fee, prevents the dispute from counting against your chargeback ratio, and keeps you out of monitoring programs.

Equally important: make it easy for customers to reach you directly. A surprising number of chargebacks originate from customers who couldn’t find your contact information, didn’t recognize the billing descriptor on their statement, or gave up waiting for a customer service response. Clear billing descriptors, prominent contact information, and fast response times are unglamorous but highly effective chargeback prevention tools.

This is an area where your payment processor’s capabilities matter significantly. BAMS, for example, offers proactive chargeback defense that includes alert-based interception, helping merchants resolve disputes before they become formal chargebacks and protecting both revenue and chargeback ratios.

Anti-patterns to avoid: Don’t rely solely on alerts without fixing the root causes of disputes. If your billing descriptor says “PARENT CORP LLC” instead of your store name, customers will keep filing chargebacks because they don’t recognize the charge. Alerts are a safety net, not a substitute for clear communication.

Success indicators: You can track the number of alerts received versus chargebacks filed. Your chargeback-to-transaction ratio stays below network thresholds (typically 0.9% for Visa and 1.0% for Mastercard).

Step 4: Build a Representment-Ready Evidence System

Objective: Win the disputes you can’t prevent by having organized, compelling evidence ready before you need it.

When a chargeback does hit your account, you have a limited window (usually 20 to 30 days) to respond with a representment package. The quality of your evidence determines whether you recover the funds or absorb the loss. For tokenized transactions, this requires some additional preparation.

Start by ensuring your system captures and retains: the full transaction record (including token reference and authentication data), delivery confirmation with tracking and signature where applicable, screenshots of the product listing at the time of purchase, any customer communication (emails, chat logs, support tickets), and your refund/return policy as displayed during checkout.

For mobile wallet transactions specifically, document the authentication method used (biometric, passcode), the 3DS authentication result if applicable, and the device token identifier. This information helps demonstrate that the transaction was authorized by the device holder, which is your strongest argument against unauthorized-use claims.

Anti-patterns to avoid: Don’t wait until a chargeback arrives to start gathering evidence. By then, chat logs may have been purged, product listings may have changed, and delivery confirmations may be harder to retrieve. Build evidence capture into your fulfillment workflow so it happens automatically.

Success indicators: You can assemble a complete representment package within 48 hours of receiving a chargeback notification. Your representment win rate exceeds 40% (the industry average hovers around 30% for merchants without structured evidence systems).

Step 5: Monitor, Measure, and Adjust Your Chargeback Ratio

Objective: Keep your chargeback ratio below network thresholds and identify emerging patterns before they become costly.

Card networks monitor your chargeback ratio (chargebacks divided by total transactions) on a monthly basis. Exceed their threshold, and you enter a monitoring program that brings additional fees, mandatory remediation plans, and in severe cases, the loss of your ability to accept that card brand entirely. Even though tokenization has reduced chargeback rates from 1.8% to 0.6% on average, your specific ratio depends on your customer base, product category, and operational practices.

Set up a monthly review cadence. Track your chargeback ratio by payment method (card-on-file versus mobile wallet versus manual entry), by reason code (fraud, product not received, not as described), and by customer segment (new versus returning). This data tells you where your vulnerabilities are and whether your prevention efforts are working.

Pay special attention to seasonal patterns. If you run promotions that attract new customers, your chargeback ratio may spike 30 to 60 days later as disputes from those transactions arrive. Anticipating these spikes lets you adjust your verification thresholds proactively.

Anti-patterns to avoid: Don’t track chargebacks only as a dollar amount. A low-dollar chargeback counts the same as a high-dollar one in your ratio calculation. Ten $15 chargebacks can push you into a monitoring program just as fast as one $150 chargeback.

Success indicators: You have a dashboard or report that shows your chargeback ratio by month, by payment method, and by reason code. You can identify trends within one billing cycle rather than discovering problems retroactively.

Step 6: Align Your Payment Processor with Your Protection Strategy

Objective: Ensure your processor provides the reporting, tools, and support needed to execute the layers above.

Your payment processor is not just a transaction pipe. It’s a critical partner in chargeback defense. Evaluate whether your current processor gives you: clear visibility into which transactions are liability-shifted, timely chargeback notifications with enough detail to respond effectively, access to pre-dispute alert networks, and reporting that separates tokenized from non-tokenized transaction performance.

Many eCommerce operators discover too late that their processor’s chargeback reporting is minimal, their alert coverage is incomplete, or their dispute response tools are cumbersome. If you’re managing a growing volume of mobile wallet transactions, these gaps translate directly into lost revenue.

This is also where expanding your payment options intersects with revenue protection. Adding mobile wallets should be part of a broader strategy that includes next-day funding to maintain cash flow, transparent fee structures so you can accurately calculate the cost of disputes, and dedicated account management so you have a human to call when a chargeback pattern emerges.

Anti-patterns to avoid: Don’t evaluate processors solely on transaction fees. A processor that charges slightly more per transaction but provides proactive chargeback defense and faster funding can save you significantly more than the fee difference when disputes arise.

Success indicators: You can name your account manager. You receive chargeback notifications within 24 hours. Your processor’s reporting distinguishes between payment methods and authentication outcomes.

Practical Examples: How This Plays Out

Scenario A: The “I Didn’t Order This” Apple Pay Chargeback

A customer purchases a $120 item using Apple Pay on your Shopify store. Three weeks later, you receive a chargeback coded as “unauthorized transaction.” The customer’s bank accepted the dispute because the cardholder claimed they didn’t make the purchase.

Without 3DS: You bear full liability. You lose the $120, pay a $25 chargeback fee, and the dispute counts against your ratio. With 3DS active and authentication confirmed: Liability shifts to the issuing bank. You keep the revenue. The dispute doesn’t count against your ratio.

The difference between these two outcomes is a configuration setting in your payment gateway. The product, the customer, and the token are identical. Only the authentication layer changes the financial result.

Scenario B: The Billing Descriptor Problem

An eCommerce store selling specialty kitchen tools processes 200 Apple Pay transactions per month. Their billing descriptor reads “ACME HOLDINGS LLC.” Over six months, they accumulate 14 chargebacks coded as “transaction not recognized,” all from customers who simply didn’t recognize the charge on their statement.

Those 14 chargebacks cost the merchant $350 in fees alone, plus the lost revenue on any disputes they couldn’t successfully represent. Updating the billing descriptor to the store’s actual brand name, a change that takes minutes with most processors, would have prevented the majority of those disputes.

Scenario C: The Friendly Fraud Pattern

A mid-size apparel brand notices that chargebacks from mobile wallet transactions spike every January, following holiday gift purchases. The pattern: gift recipients contact their bank rather than the merchant when they want to return an item, often because the merchant’s return policy is buried in a footer link.

The fix involves making the return process more visible (confirmation emails, packing slip instructions, prominent website placement) and enrolling in pre-dispute alerts to intercept these disputes before they formalize. Combined, these changes reduce January chargebacks by over 50% without any change to the payment technology itself.

Common Mistakes and Pitfalls

The most common mistake is treating tokenization as a complete fraud solution. It’s a powerful data security tool, but it doesn’t address the full spectrum of chargeback risk. Merchants who assume “Apple Pay is secure, so chargebacks won’t be a problem” are consistently surprised when disputes arrive.

A second frequent error is neglecting the operational side of mobile wallet adoption. Enabling Apple Pay at checkout takes minutes. Building the supporting infrastructure (clear descriptors, evidence capture, dispute response workflows) takes deliberate effort that many merchants skip.

Third, many merchants don’t realize that chargeback fees and ratio penalties apply regardless of whether the underlying transaction was tokenized. A chargeback is a chargeback in the eyes of the card network, whether the payment came from a typed-in card number or a biometrically authenticated mobile wallet.

Finally, waiting to address chargebacks until you’re already in a monitoring program is far more expensive than building prevention into your operations from the start. The monitoring program fees alone can cost thousands per month, on top of the disputes themselves.

What to Do Next

You don’t need to implement all six steps simultaneously. Start with the one that addresses your most immediate vulnerability.

If you’re not sure whether 3DS is active on your mobile wallet transactions, contact your payment processor today and ask. That single question can reveal whether you’re currently absorbing liability you don’t need to carry.

If you already have 3DS in place, check your billing descriptor. Pull up a recent transaction on a test card or ask a recent customer what appeared on their statement. If it doesn’t clearly identify your store, update it.

Then, set a calendar reminder to review your chargeback ratio monthly. Even ten minutes of review can surface patterns that save thousands of dollars over the course of a quarter. Revenue protection isn’t a one-time project. It’s an ongoing practice that compounds in value as your mobile wallet transaction volume grows. Use this guide as a reference point, not a checklist to complete and forget.

Frequently Asked Questions

Does Apple Pay’s tokenization protect merchants from chargebacks?

Not entirely. Tokenization protects the card data from being stolen and reused, which reduces fraud from compromised credentials. But it does not prevent chargebacks from legitimate cardholders who dispute a transaction for reasons like “item not received,” “not as described,” or even false claims of unauthorized use. Merchants still bear liability for these disputes unless additional protections like 3D Secure authentication are in place.

What is the difference between fraud prevention and chargeback prevention?

Fraud prevention stops unauthorized transactions from being processed in the first place (tokenization, device fingerprinting, velocity checks). Chargeback prevention stops completed transactions from being reversed after the fact (pre-dispute alerts, clear billing descriptors, evidence-based representment). You need both. Tokenization handles the fraud prevention side well, but chargeback prevention requires separate operational practices.

How does 3D Secure shift liability away from merchants?

When a transaction is authenticated through 3D Secure and the cardholder later files a fraud-coded chargeback, the liability shifts from the merchant to the card-issuing bank. The bank bears the financial loss instead of you. This works because the authentication step provides evidence that the cardholder (or their device) verified the transaction. For mobile wallet payments, the biometric authentication can sometimes satisfy 3DS requirements automatically, but you should confirm this with your processor.

What chargeback ratio triggers a monitoring program?

Visa’s Dispute Monitoring Program activates when your chargeback ratio exceeds 0.9% and you have more than 100 chargebacks in a month. Mastercard’s Excessive Chargeback Program triggers at 1.0% with 100 or more chargebacks. Once you enter these programs, you face additional fees, mandatory action plans, and potential restrictions on your ability to process payments. Staying below these thresholds is essential for long-term business viability.

Why are mobile wallet chargebacks harder to match to orders?

Mobile wallet transactions use a device-specific token instead of the actual card number. When a chargeback notification arrives, it may reference the token or a truncated version of it, which can look different from what appears in your order management system. This mismatch slows down your ability to identify the disputed order, gather evidence, and respond within the required timeframe. Ensuring your payment processor provides clear token-to-order mapping in their reporting helps solve this problem.

Can a merchant be penalized for chargebacks even if the transactions were legitimate?

Yes. Card networks count all chargebacks against your ratio, regardless of whether the underlying transaction was legitimate or whether you eventually win the dispute through representment. Even friendly fraud (where the actual cardholder disputes a purchase they genuinely made) counts against you. This is why prevention and deflection before the formal chargeback is filed are so important to your bottom line.