Payment Processing Speed: A Stage-by-Stage Guide

Map the checkout-to-deposit pipeline so you can pinpoint delays and unlock faster merchant funding

Learn what happens at every stage between an eCommerce sale and your bank deposit. This guide breaks down authorization, batching, clearing, and settlement so you can identify which delays are structural and which you can fix to achieve next-day funding.

TL;DR

- Funding speed is a system, not a feature – Every deposit passes through five stages (authorization, batching, clearing, settlement, deposit), and delays at any stage cascade through the rest. Comparing “same-day” vs. “next-day” without understanding the pipeline misses the point.

- Batch timing is your biggest controllable lever – If your platform batches transactions after your processor’s daily cutoff, you’re adding a full business day of delay by default. Check and align these times immediately.

- Next-day funding beats same-day for most eCommerce operations – Same-day rails cost more per transaction. For steady daily volume, next-day funding delivers the best balance of speed and cost. Reserve same-day for high-value or urgent scenarios.

- Weekends and holidays create a hidden cash flow tax – Standard settlement doesn’t operate on non-business days. Weekend sales (often your peak) may not deposit until mid-week. Build this into your cash flow model explicitly.

- Proactive communication prevents the worst delays – Volume spikes, high chargeback ratios, and incomplete transaction data trigger holds and reserves. Notify your processor before promotions, monitor dispute rates, and keep your transaction data clean to protect your funding timeline.

Guide Orientation: What This Covers and Who It’s For

This guide maps the complete journey your eCommerce revenue takes from checkout to your bank account. It breaks down each processing stage (authorization, batching, clearing, settlement, deposit) so you can see exactly where delays happen and which ones you can control.

It’s built for eCommerce managers at established online businesses who are tired of treating payment processing speed as a mystery. If you manage daily revenue cycles, restock inventory on tight timelines, or scale ad spend based on available cash, this is for you.

By the end, you’ll understand the mechanical differences between same-day and next-day merchant funding, know which delays are structural and which are operational, and have a framework for optimizing your specific setup. This guide does not compare individual processor pricing or review specific gateways. It focuses on the system itself.

Why Payment Processing Speed and Merchant Funding Timing Actually Matter

Most eCommerce operators treat the gap between a sale and a deposit as fixed. It isn’t. That gap is a system with moving parts, and each part introduces a delay you either accept or address.

The cost of ignoring this is concrete. When your deposits arrive in three to five business days instead of one, you’re financing your own operations with invisible float. You restock slower. You pause ad campaigns waiting for cash to clear. You negotiate worse terms with suppliers because you can’t pay on receipt. Over a year, that compounding drag on cash velocity can mean tens of thousands of dollars in missed opportunity or unnecessary credit costs. According to the Federal Reserve’s 2025 Small Business Credit Survey, cash flow management and operating expenses remain significant concerns for many businesses, making funding speed an important operational consideration.

The landscape has shifted. The landscape has shifted. The ACH Network continues to expand electronic payment capabilities, while newer payment infrastructure is increasing the availability of faster settlement options. Same-Day ACH windows have expanded. Push-to-card technology can accelerate fund availability. Yet many merchants still operate on legacy settlement schedules.

The expansion of faster payment infrastructure through the Federal Reserve’s FedNow Service continues to increase the availability of near real-time payment capabilities for participating institutions.

Push-to-card technology can deliver funds in under a minute. Yet most merchants are still on legacy settlement timelines because nobody explained the pipeline clearly enough to act on it.

Understanding this pipeline isn’t academic. It’s the difference between a business that reacts to cash flow and one that engineers it. The operators who map this system gain a structural advantage: they can forecast deposits accurately, time purchases strategically, and treat their payment processor as a cash velocity engine rather than a cost center.

Core Concepts: The Language of the Funding Pipeline

Before dissecting the pipeline, you need clarity on a few terms that processors use loosely and merchants often conflate.

Settlement vs. Funding vs. Deposit

Settlement is when the card network (Visa, Mastercard) transfers money from the cardholder’s bank to the acquiring bank. Funding is when your processor releases those settled funds to your account. Deposit is when the money actually appears in your bank. These are three distinct events, and the gap between them is where most confusion (and most delays) lives.

Payment Rails: The Tracks Your Money Rides

A payment rail is the infrastructure that physically moves money between institutions. Standard ACH, Same-Day ACH, and FedNow are all different rails with different speeds, costs, and availability windows. Your processor chooses which rail to use for your deposits, and that choice directly determines when you get paid. For a deeper comparison of these rails, see this breakdown of same-day vs. next-day payment rails.

Batch vs. Real-Time

Most card processing still operates on a batch model: your transactions accumulate throughout the day, then get submitted as a group at a specific cutoff time. Real-time processing, by contrast, handles each transaction individually and continuously. The batch model is why your 11 PM sale and your 9 AM sale can land in the same deposit, or in deposits two days apart, depending on when your batch closes.

The Misconception to Correct Now

“Same-day funding” and “next-day funding” are not just speed tiers you pick from a menu. They describe the outcome of a system with multiple variables: your batch cutoff time, the payment rail your processor uses, your bank’s posting schedule, and the day of the week. Changing the outcome requires understanding the inputs.

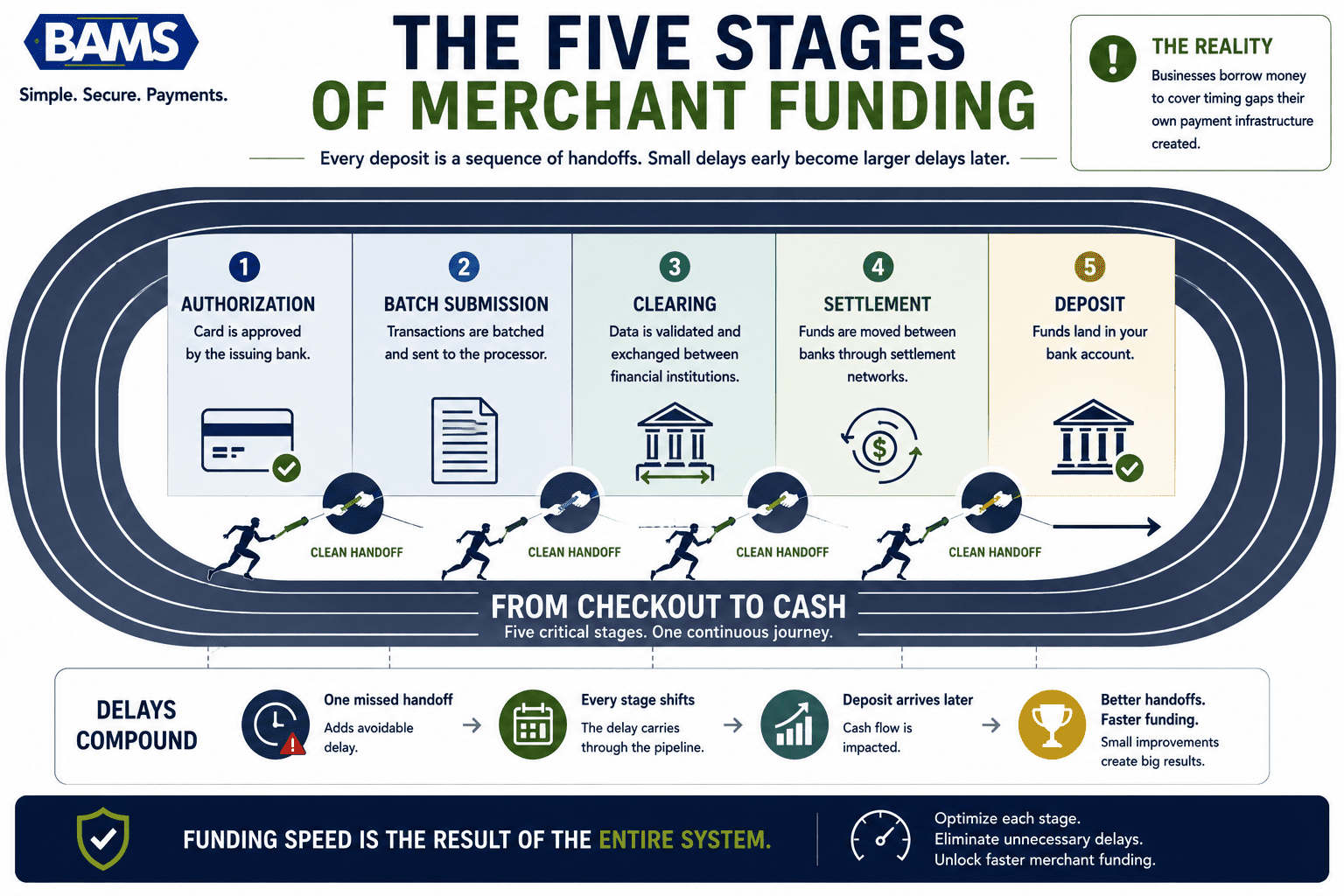

The Framework: Five Stages from Checkout to Deposit

Every deposit is a sequence of handoffs. Small delays early become larger delays later.

Every eCommerce transaction passes through five stages before money reaches your bank. Think of it as a relay race: the total time depends not just on how fast each runner is, but on how clean each handoff goes.

The five stages are:

- Authorization — The instant approval check at checkout

- Batch Submission — When your accumulated transactions get sent to the processor

- Clearing — When the card network reconciles the transaction between banks

- Settlement — When funds transfer from the issuing bank to the acquiring bank

- Deposit — When your processor releases funds to your business bank account via a payment rail

Each stage has its own timeline, its own potential failure points, and its own optimization levers. The stages are sequential: a delay at stage two cascades through stages three, four, and five. This is why two merchants using the same processor can experience wildly different funding timelines. Their setups create different handoff conditions at each stage.

Step-by-Step Breakdown: Mapping and Optimizing Each Stage

Step 1: Authorization — The 2-Second Gate That Sets the Clock

Objective: Confirm the transaction is valid and the cardholder has available funds, triggering the start of the funding timeline.

When a customer clicks “Pay,” your payment gateway encrypts the card data and sends an authorization request through the card network to the cardholder’s issuing bank. Authorization typically happens within a matter of seconds, allowing the transaction to enter the payment processing pipeline almost immediately after the customer completes checkout. If approved, a hold is placed on the cardholder’s funds, and your system records a successful transaction.

Authorization itself rarely causes deposit delays. But here’s what can: failed authorizations that require retry logic, fraud screening holds that pause the transaction before it enters your batch, and gateway timeouts that leave transactions in a limbo state. Each of these scenarios means the transaction doesn’t enter the pipeline cleanly, which pushes everything downstream later.

Anti-patterns to avoid: Overly aggressive fraud filters that flag legitimate transactions and hold them for manual review. If your fraud screening adds hours before a transaction clears into your batch queue, you’re silently delaying your own funding. Also avoid ignoring authorization decline rates. High decline rates often signal configuration issues with your gateway or mismatches between your eCommerce platform and processor setup.

Success indicators: Authorization approval rates above 95%. Fraud review queues that clear within minutes, not hours. Zero transactions stuck in pending states at batch time.

Step 2: Batch Submission — The Controllable Chokepoint

Objective: Submit all authorized transactions to your processor before the cutoff time that determines your funding date.

This is the single most impactful stage for merchants to optimize, and the one most often ignored. Your authorized transactions sit in a queue until they’re submitted as a batch to your processor. Most processors have a daily cutoff time (often between 3 PM and 6 PM ET). Transactions submitted before the cutoff enter that day’s settlement cycle. Transactions submitted after the cutoff wait until the next cycle.

Here’s where it gets practical. If your eCommerce platform auto-batches at midnight, but your processor’s cutoff is 5 PM, every transaction from 5:01 PM to 11:59 PM misses today’s cycle and gets pushed to tomorrow’s. That’s a full extra day of delay, built into your system by default. Many platforms let you configure batch submission times, but few merchants ever change the default.

Anti-patterns to avoid: Leaving batch times at platform defaults without checking your processor’s cutoff. Running manual batch submissions inconsistently. Assuming “auto-batch” means “optimal batch.” Also, be cautious during high-volume sale events (Black Friday, flash sales) where transaction volume spikes can cause batch processing queues to back up.

Success indicators: Your batch closes at least 30 minutes before your processor’s daily cutoff. You can verify batch submission timestamps in your gateway dashboard. Weekend and holiday batches are accounted for in your cash flow projections.

Step 3: Clearing — The Network Reconciliation You Can’t Speed Up (But Can Stop Slowing Down)

Objective: Allow the card network to reconcile transaction details between the acquiring bank and issuing bank without triggering exceptions.

Once your batch is submitted, the card network (Visa, Mastercard, etc.) takes over. Clearing is the process of matching your transaction records with the issuing bank’s records, calculating interchange fees, and preparing the net settlement amount. This stage typically takes a few hours to one business day.

You can’t directly accelerate clearing. But you can stop accidentally slowing it down. Clearing exceptions occur when transaction data doesn’t match: incorrect tax amounts, mismatched currency codes, incomplete Level 2/Level 3 data for B2B transactions, or address verification mismatches. Each exception requires manual resolution, which can add one to three days to your timeline.

A standard card transaction moves through authorization, batch submission, clearing, settlement, and deposit, with the overall timeline varying depending on processor configuration, settlement schedules, and the payment rail used for funding. Clearing exceptions are one of the primary reasons merchants experience the longer end of that range.

Anti-patterns to avoid: Submitting incomplete transaction data (missing AVS results, incorrect merchant category codes). Ignoring clearing exception reports from your processor. Processing cross-border transactions without proper currency handling, which triggers additional reconciliation steps.

Success indicators: Clearing exception rate below 1%. Consistent settlement amounts that match your batch totals minus expected fees. No surprise holds or reserves triggered by data quality issues.

Step 4: Settlement — Where the Money Actually Moves Between Banks

Objective: Ensure the net settlement amount transfers from the card network to your acquiring bank without reserve holds or delays.

Settlement is the actual movement of money. The card network calculates the net amount (your gross sales minus interchange fees, assessments, and any processor markup) and transfers it to your acquiring bank. This typically happens within one business day of clearing, but several factors can extend it.

Reserve holds are the most common delay at this stage. If your processor considers your business higher risk (high average ticket size, elevated chargeback ratio, new account, or sudden volume spikes), they may hold a percentage of your settlement in reserve. This isn’t a processing delay in the technical sense, but the effect on your cash flow is identical.

Volume spikes deserve special attention for ecommerce. If your typical daily volume is $5,000 and you suddenly process $50,000 during a sale event, many processors will flag this and hold funds for review. The fix isn’t reactive; it’s proactive. Notify your processor before major promotions. Provide documentation of expected volume increases. Build a track record of consistent processing so your risk profile supports higher thresholds.

Anti-patterns to avoid: Ignoring your chargeback ratio until it triggers a reserve. Failing to notify your processor before promotional events. Not understanding your reserve terms (rolling reserve vs. fixed reserve vs. capped reserve).

Success indicators: Settlement amounts consistently match expected net revenue. No surprise reserve holds. Your processor’s risk team knows your business patterns and seasonal cycles.

Step 5: Deposit — The Last Mile Where Payment Rails Determine Everything

Objective: Get settled funds from your acquiring bank into your business bank account as fast as the chosen payment rail allows.

This is where the same-day vs. next-day distinction becomes tangible. Your processor has your settled funds. Now they need to send them to your bank. The rail they use determines the speed.

Standard ACH: The traditional rail. Deposits typically arrive in 1 to 2 business days after settlement. Does not operate on weekends or bank holidays. This is what most merchants default to, and it’s why Friday sales often don’t hit your account until Tuesday or Wednesday.

Same-Day ACH: Funds can be available in about 3 to 4 hours if submitted before the cutoff time, or by 9 AM local time the next banking day if submitted after. Faster, but still bound by banking hours and business days.

Push-to-card and real-time rails: Push-to-card payments can make funds available in 30 minutes and, in most cases, within seconds after approval. Real-time payment networks like FedNow operate continuously, but adoption among processors and banks is still growing.

For most eCommerce businesses processing steady daily volume, next-day funding via optimized ACH or Same-Day ACH offers the best balance of speed, cost, and reliability. Same-day funding adds marginal speed at higher per-transaction cost, which makes sense for specific scenarios (large single transactions, urgent cash needs) but rarely pencils out as a default for all transactions. This comparison of same-day vs. next-day funding for eCommerce breaks down the operational tradeoffs in detail.

This is where your processor relationship matters most.

BAMS, for example, offers next-day funding as a standard feature for qualifying merchants, which eliminates the most common deposit delay without the premium cost of same-day rails. If your current processor treats next-day funding as an upgrade tier, that’s worth questioning.

Anti-patterns to avoid: Assuming all “next-day funding” offers are identical (cutoff times and qualifying criteria vary significantly). Paying for same-day funding across all transactions when only a subset benefits from it. Using a business bank that posts ACH deposits slowly, negating your processor’s speed.

Success indicators: Deposits arrive predictably on the expected day. Weekend sales deposit by Tuesday at the latest. Your cash flow forecast matches actual deposit timing within one day, consistently.

Step 6: Weekend and Holiday Patterns — The Hidden Calendar Tax

Objective: Account for non-business-day gaps that silently extend your funding timeline, especially during peak eCommerce periods.

Standard ACH and most card settlement processes do not operate on weekends or federal holidays. This creates a predictable but often unplanned cash flow gap. Transactions processed Friday evening through Sunday don’t begin clearing until Monday, with deposits arriving Tuesday or Wednesday under standard timelines.

For eCommerce businesses, this is particularly painful because weekends often represent peak sales periods. A business doing 30% of weekly volume on Saturday and Sunday may not see those funds for three to four business days. Over a month, that’s a significant amount of capital sitting in transit.

The mitigation strategy is twofold. First, adjust your cash flow model to account for weekend float explicitly. Don’t forecast deposits based on sale dates; forecast based on business-day settlement cycles. Second, evaluate whether your processor offers weekend batch processing. Some processors will accept and begin processing weekend batches so they’re first in queue Monday morning, reducing the gap by up to a full day.

Anti-patterns to avoid: Planning inventory purchases or supplier payments based on weekend revenue without accounting for the deposit delay. Ignoring holiday weekends (three-day weekends can push deposits out by four or five calendar days). Assuming real-time payment rails that operate 24/7 are available through your current processor without verifying.

Success indicators: Your cash flow model includes a weekend/holiday adjustment. You’ve confirmed your processor’s weekend batch handling policy in writing. No cash crunches tied to predictable calendar gaps.

Practical Examples: How This Plays Out in Real Scenarios

Scenario A: The Default Setup

An eCommerce store processes $8,000 in sales on Thursday. Their platform auto-batches at midnight. Their processor’s cutoff is 5 PM ET. Result: Thursday’s sales batch at midnight, missing Thursday’s cutoff. They enter Friday’s settlement cycle. Settlement completes Monday (skipping the weekend). Deposit via standard ACH arrives Tuesday or Wednesday. Total time from sale to deposit: 5 to 6 calendar days.

Scenario B: The Optimized Setup

Same store, same $8,000 Thursday. But they’ve configured their platform to batch at 4 PM ET. Their processor (offering next-day funding) picks up the batch before the 5 PM cutoff. Settlement processes Friday. Deposit via Same-Day ACH arrives Friday afternoon or Monday morning. Total time from sale to deposit: 1 to 4 calendar days, depending on the day of the week.

Scenario C: The Flash Sale Trap

A merchant runs a 48-hour flash sale and processes $75,000, ten times their normal daily volume. They didn’t notify their processor. The volume spike triggers a fraud/risk review. Settlement is held for 48 hours while the processor verifies the transactions. Delays can stretch funding to up to 7 days in cases like these. The merchant misses a supplier payment deadline and loses a bulk discount. The fix: a five-minute phone call to their processor before the sale launched.

These scenarios illustrate the same principle: the pipeline is a system, and small configuration changes at early stages compound into significant timing differences at the deposit stage.

Common Mistakes and Pitfalls

Treating funding speed as a fixed feature. It’s not. It’s the output of your entire processing configuration. Switching processors for “faster funding” without optimizing your batch times, data quality, and bank setup often produces the same results.

Optimizing for speed on every transaction. Same-day funding costs more per transaction. For most eCommerce operations, next-day funding on all transactions plus same-day funding on select high-value or urgent transactions is the cost-effective approach.

Ignoring the bank side of the equation. Your processor can release funds at 6 AM, but if your business bank posts ACH credits at 4 PM, you’ve lost most of the speed advantage. Ask your bank about their ACH posting schedule.

Not reading the fine print on “next-day funding.” Some processors advertise next-day funding but impose cutoff times so early (noon or 2 PM) that a large portion of your daily transactions miss the window. Verify the actual cutoff, not just the marketing claim.

Forgetting about chargebacks. High chargeback ratios don’t just cost you fees. They trigger reserve holds and can downgrade your funding speed tier. Proactive chargeback defense (a service BAMS includes for its merchants) protects your funding timeline, not just your dispute costs.

What to Do Next

You cannot control every stage, but you can remove many avoidable delays.

Start with one action: log into your payment gateway and find your batch submission time. Compare it to your processor’s published cutoff. If there’s a gap, close it. That single change can shave a full business day off your deposit timeline with zero cost.

Then, map your last 30 days of deposits against your sales dates. Look for patterns. Are weekend sales consistently arriving mid-week? Are certain transaction types (higher dollar amounts, international cards) settling slower? These patterns reveal which stages of your pipeline need attention.

Use this guide as a reference, not a one-time read. Each time you change platforms, switch processors, or enter a high-volume season, revisit the five stages and verify your configuration still matches your cash flow needs. The merchants who treat funding speed as an ongoing operational discipline, rather than a one-time processor feature, consistently outperform those who don’t.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your processor deposits the net proceeds from your card transactions into your business bank account by the next business day. The key qualifier is “business day.” Transactions processed on Friday may not deposit until Monday. The actual speed depends on your batch submission time, your processor’s cutoff, and the payment rail used for the deposit.

Why is next-day funding important for small businesses?

Faster deposits reduce the gap between earning revenue and having access to it. For small and midsize eCommerce businesses, this means you can restock inventory sooner, fund ad campaigns without waiting for cash to clear, and pay suppliers on tighter terms. Over time, faster funding compounds into better cash flow predictability and reduced reliance on credit lines to bridge gaps.

How can a business qualify for next-day funding?

Qualification typically depends on your processing history, chargeback ratio, average ticket size, and business type. Processors assess risk: merchants with consistent volume, low dispute rates, and established track records qualify more easily. Some processors, like BAMS, offer next-day funding as a standard feature for qualifying merchants rather than a premium add-on.

What are the differences between next-day funding and standard funding?

Standard funding typically takes 2 to 3 business days (sometimes longer) because it uses standard ACH rails and may involve additional clearing steps. Next-day funding uses optimized settlement processes and faster ACH windows to compress that timeline to one business day. The underlying transaction stages are the same; the difference is how quickly each handoff occurs and which payment rail delivers the final deposit.

When should a business consider using same-day funding services?

Same-day funding makes sense for specific situations: large individual transactions where you need immediate access to capital, urgent supplier payments with tight deadlines, or businesses with extremely thin cash reserves where even one day of float creates operational risk. For routine daily processing, next-day funding is typically more cost-effective because same-day rails carry higher per-transaction fees.

Which factors affect the speed of my deposits beyond my processor?

Your business bank’s ACH posting schedule is a major factor most merchants overlook. If your bank posts ACH credits once daily at 4 PM, a deposit released at 7 AM sits idle for nine hours. Your eCommerce platform’s batch configuration, your gateway’s fraud screening speed, and the quality of your transaction data (which affects clearing exceptions) all contribute to the total timeline from sale to deposit.