Apple Pay Fraud Chargebacks: A Merchant Defense Guide

Why tokenization doesn’t protect your revenue—and the operational steps that actually do

Learn how Device Account Numbers work, why tokenized Apple Pay transactions still generate chargebacks, and how to build a dispute defense process that protects your revenue from mobile wallet fraud.

TL;DR

- Tokenization protects card data, not your revenue — Apple Pay’s Device Account Number system prevents data breaches but doesn’t change chargeback rules. You still carry full merchant liability when disputes arrive.

- The DAN mismatch is your biggest operational risk — The Device Account Number differs from the customer’s actual card number, making it difficult to match chargebacks to orders. Fix this mapping problem first.

- Don’t over-trust biometric authentication — Apple Pay’s fraud rate is roughly 60% lower than traditional cards, but stolen cards can still be provisioned to devices. Calibrate fraud filters for wallet-specific patterns instead of whitelisting all Apple Pay transactions.

- Evidence architecture wins disputes — Automate the collection of order confirmations, shipping tracking, delivery proof, and customer communication logs so you can assemble a chargeback response in under 15 minutes.

- Track Apple Pay chargebacks separately — Segment dispute data by payment method to spot patterns, improve win rates, and keep your dispute ratio below network monitoring thresholds as mobile wallet volume grows.

Guide Orientation: What This Guide Covers and Who It’s For

This guide addresses a specific, growing problem: Apple Pay fraud chargebacks landing on your desk even though tokenization was supposed to make transactions safer. It’s built for eCommerce managers at small-to-midsize online businesses who accept (or plan to accept) mobile wallet payments and need to understand where merchant liability actually sits.

By the end, you’ll understand how the Device Account Number system works at a practical level, why tokenized transactions still generate chargebacks, and what operational steps you can take to defend your revenue. You’ll walk away with a concrete framework for matching Apple Pay disputes to evidence, adjusting fraud filters, and building a chargeback defense process that accounts for mobile wallet transactions specifically.

This guide does not cover PCI compliance architecture, enterprise-level payment orchestration, or the technical cryptography behind tokenization. It focuses on what happens after the transaction clears and a dispute shows up in your queue.

Why Protecting Revenue from Apple Pay Fraud Matters Now

Mobile wallet adoption is no longer an emerging trend. Apple Pay processed an estimate of about $ trillion in transactions in 2025, capturing over 50% of in-store mobile wallet transactions in the U.S. alone. For eCommerce merchants, the shift is equally dramatic: customers increasingly expect Apple Pay as a checkout option, and declining to offer it means losing conversions.

The security narrative around Apple Pay is compelling and largely accurate. Apple Pay runs a fraud rate roughly 60% lower than traditional credit and debit card transactions, and its tokenized architecture means card numbers are never shared with merchants. That materially reduces breach risk. But here’s the gap most merchants miss: lower fraud rates across the ecosystem do not translate to zero chargebacks for your business.

PCI Security Standards Council guidance explains how tokenization protects payment credentials by replacing sensitive card data with secure payment tokens.

When a customer disputes an Apple Pay transaction, the chargeback follows standard card network rules. The token protected the card number in transit, but it did nothing to prove you delivered the product, that the buyer authorized the purchase, or that the transaction was legitimate. You still carry the burden of proof. And because the transaction data you receive from Apple Pay looks different from a standard card-not-present transaction, many merchants struggle to match disputes to evidence, losing cases they should win.

The cost of inaction is straightforward: lost revenue from preventable chargebacks, rising dispute ratios that trigger monitoring programs, and potential increases in processing fees. As mobile wallet volume grows, so does your exposure if your dispute workflow hasn’t adapted.

Core Concepts: What Tokenization Actually Protects (and What It Doesn’t)

The Device Account Number Explained

When a customer adds a credit or debit card to Apple Pay, the card network (Visa, Mastercard, Amex) issues a Device Account Number (DAN), sometimes called a DPAN (Device Primary Account Number). This is a unique, device-specific number that replaces the actual card number (the FPAN, or Funding Primary Account Number). The DAN is stored in the device’s Secure Element, a dedicated hardware chip.

Mastercard Developers documents how device-based payment credentials and tokenized payment data are used throughout modern digital wallet transactions.

Every transaction generates a one-time dynamic security code tied to that DAN. You, the merchant, never see the real card number. This is why Apple Pay’s tokenized architecture materially reduces the surface area for breach-driven card-data theft compared with traditional card-present and card-not-present transactions.

The Liability Gap

Tokenization protects card data. It does not protect merchant dispute outcomes. This is the critical distinction. When a cardholder calls their bank and says “I didn’t make that purchase” or “I never received that item,” the chargeback process is identical whether the original transaction used a raw card number or a Device Account Number. The card networks treat the DAN as a valid payment credential. Dispute rules, evidence requirements, and liability assignments remain unchanged.

Visa’s payment processing guidance explains the roles of merchants, issuers, acquirers, and payment networks throughout the transaction lifecycle, illustrating why merchants remain responsible for responding to eligible disputes.

Why Apple Pay Disputes Look Different in Your System

Because the DAN is different from the cardholder’s actual card number, you may see unfamiliar digits in your transaction records when a chargeback arrives. If your order management system or CRM indexes transactions by the last four digits of the card, an Apple Pay dispute can appear disconnected from the original order. This mismatch is a leading cause of merchants failing to respond to winnable disputes simply because they couldn’t locate the right evidence.

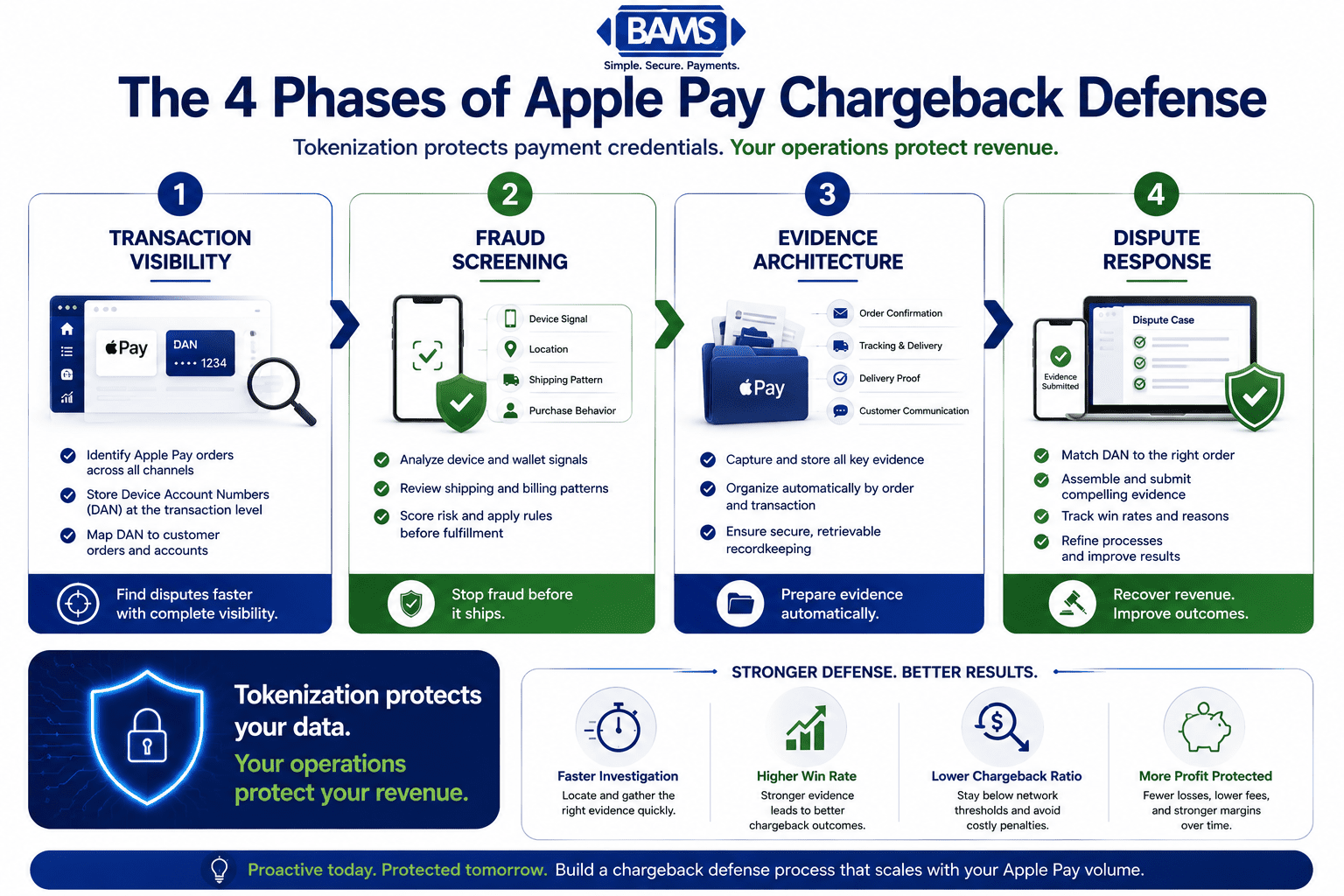

The Framework: Four Phases of Apple Pay Chargeback Defense

Protecting revenue from Apple Pay disputes requires more than tokenization. A structured defense process helps merchants reduce fraud losses and improve chargeback outcomes.

Protecting revenue from mobile wallet disputes requires a structured approach across four phases. Each phase addresses a different layer of the problem, from preventing fraudulent transactions before they settle, to winning disputes when they arrive.

- Phase 1: Transaction Visibility — Ensure your systems can identify, track, and reconcile Apple Pay transactions distinctly from standard card payments.

- Phase 2: Pre-Authorization Fraud Screening — Apply fraud detection rules calibrated for mobile wallet transaction patterns, not just traditional card-not-present signals.

- Phase 3: Evidence Architecture — Build your order fulfillment and customer communication workflows to produce chargeback-ready evidence automatically.

- Phase 4: Dispute Response Execution — Match disputes to evidence quickly, respond within deadlines, and track outcomes to refine your process.

These phases are sequential in setup but operate concurrently once established. Weakness in any single phase undermines the others.

Step-by-Step: Building Your Mobile Wallet Chargeback Defense

Step 1: Map Your Apple Pay Transaction Data Flow

Objective: Achieve full visibility into which transactions originate from Apple Pay and how their identifiers flow through your systems.

Start by auditing how Apple Pay transactions appear in your payment gateway, your order management system, and your accounting software. Specifically, identify where the Device Account Number shows up versus the cardholder’s actual card number. Most gateways flag Apple Pay transactions with a wallet indicator or token type field. Confirm this field is being captured and stored alongside each order.

Next, verify that you can search and filter transactions by payment method. If a chargeback arrives referencing a DAN you’ve never seen, you need a reliable path from that number back to the original order, the shipping confirmation, and the customer record. Many eCommerce platforms store the token type but don’t surface it in their dispute management interface. If yours doesn’t, export transaction data regularly and maintain a cross-reference table.

Anti-patterns to avoid: Don’t assume your existing transaction search will work for Apple Pay disputes. Don’t rely solely on the last four digits of the card number to match chargebacks to orders, as the DAN’s last four digits will differ from the card the customer actually holds. Don’t ignore wallet-type metadata in your gateway reports.

Success indicators: You can take any Apple Pay chargeback notification, locate the corresponding order within five minutes, and pull the associated fulfillment records without manual guesswork.

Device Account Numbers differ from customers’ actual card numbers. Mapping them correctly is essential for locating evidence and responding to Apple Pay disputes quickly.

Step 2: Calibrate Fraud Screening for Mobile Wallet Signals

Objective: Adjust your fraud detection rules to account for the distinct risk profile of Apple Pay transactions rather than treating them identically to standard card-not-present orders.

Apple Pay transactions carry an approximate fraud rate of 0.01%, significantly lower than traditional card payments, largely because biometric authentication (Face ID or Touch ID) verifies the user at the point of purchase. This means your fraud filters should treat Apple Pay differently. Overly aggressive velocity checks or AVS mismatches that make sense for manual card entry may generate unnecessary false declines on legitimate Apple Pay orders.

However, lower average fraud rates don’t mean zero risk. Fraudsters can add stolen cards to Apple Pay using social engineering to intercept the bank’s verification step. Once a stolen card is provisioned to a device, every transaction from that device passes biometric checks and looks legitimate. Watch for patterns like new shipping addresses paired with high-value orders, multiple Apple Pay orders from different “devices” shipping to the same address, or sudden spikes in Apple Pay transaction volume from a single customer account.

Anti-patterns to avoid: Don’t whitelist all Apple Pay transactions because of the low overall fraud rate. Don’t apply the same AVS/CVV rules you use for keyed-in card transactions. Don’t ignore device fingerprinting data available through your gateway.

Success indicators: Your false decline rate on Apple Pay transactions decreases while your fraud catch rate on suspicious Apple Pay orders remains stable or improves. You can articulate exactly which fraud rules apply differently to wallet-based transactions.

Step 3: Build Evidence Architecture into Your Fulfillment Workflow

Objective: Ensure every Apple Pay order automatically generates the documentation you’ll need if a chargeback arrives weeks or months later.

Chargeback defense is won or lost on evidence quality. For Apple Pay transactions, you need the same core evidence as any card-not-present dispute, but you need it organized in a way that accounts for the DAN-to-order mapping challenge. Build these evidence collection points into your standard workflow:

- Order confirmation emails sent immediately, with the order number, items, price, and the customer’s billing and shipping address clearly listed.

- Shipping confirmation with tracking sent as soon as the order ships, including carrier name, tracking number, and expected delivery date.

- Delivery confirmation captured from the carrier, ideally with signature or photo proof for orders above a threshold you define (many merchants use $75-$150).

- Customer communication logs preserved in your helpdesk or CRM, including any post-purchase messages about the order.

- IP address and device data logged at checkout, which can help demonstrate that the transaction originated from a device consistent with the customer’s profile.

For merchants processing significant Apple Pay volume, consider tagging wallet-based orders in your fulfillment system so you can prioritize evidence collection for these transactions. This is particularly important because the DAN mismatch issue means you can’t afford slow evidence retrieval.

Anti-patterns to avoid: Don’t rely on verbal or informal delivery confirmation. Don’t delete customer service chat logs after 30 days. Don’t treat digital goods differently from physical goods when it comes to evidence (access logs, download timestamps, and usage data serve the same purpose as shipping records).

Success indicators: For any order placed in the last 120 days, you can assemble a complete evidence package (order confirmation, shipping/delivery proof, customer communication) within 15 minutes.

Step 4: Respond to Apple Pay Chargebacks with Precision

Objective: Submit compelling, well-organized dispute responses that address the specific reason code and include evidence matched to the DAN-referenced transaction.

When an Apple Pay chargeback arrives, your first task is identification: match the DAN referenced in the dispute to the original order using the cross-reference process you built in Step 1. Then identify the reason code. The most common Apple Pay chargeback reason codes fall into two categories: fraud (the cardholder claims they didn’t authorize the transaction) and service (the cardholder claims non-receipt or the product wasn’t as described).

For fraud-related disputes, your strongest evidence includes the biometric authentication inherent in Apple Pay (which you can reference but not prove directly), combined with IP geolocation matching the cardholder’s known location, consistent shipping-to-billing address, and any prior purchase history from the same customer. For service-related disputes, delivery confirmation with tracking and any post-delivery communication from the customer is decisive.

Structure your response clearly: lead with a summary statement, follow with the evidence that directly contradicts the cardholder’s claim, and attach supporting documents in the order the reviewer will need them. Card network reviewers handle hundreds of cases. Make yours easy to adjudicate in your favor.

A merchant services partner with proactive chargeback defense capabilities, like BAMS, can help you identify which disputes are worth fighting, prepare evidence packages, and track win rates so you can refine your approach over time. This is especially valuable when Apple Pay dispute volume is growing but your team’s bandwidth isn’t.

Anti-patterns to avoid: Don’t submit generic response templates without customizing evidence to the specific reason code. Don’t miss response deadlines (typically 20-30 days depending on the network). Don’t ignore low-dollar chargebacks, as they still count toward your dispute ratio.

Success indicators: Your chargeback response rate is above 90%, your win rate on responded disputes trends upward over time, and your overall dispute ratio stays well below the 1% threshold that triggers network monitoring programs.

Step 5: Monitor, Measure, and Refine

Objective: Track Apple Pay-specific chargeback metrics separately from your overall dispute data to identify patterns and improve your defense over time.

Aggregate data hides the signal. If you lump Apple Pay chargebacks with all other disputes, you’ll miss patterns unique to mobile wallet transactions. Set up reporting that segments chargebacks by payment method, reason code, product category, and outcome (won, lost, or expired without response).

Review this data monthly. Look for clusters: Are Apple Pay chargebacks concentrated in a specific product category? Are they disproportionately fraud claims versus service claims? Are they coming from a particular customer demographic or geographic region? These patterns tell you where to tighten fraud screening, where to improve fulfillment documentation, and where to adjust your product or return policies.

Also track your evidence assembly time. If it takes your team more than 20 minutes to build a dispute response for an Apple Pay chargeback, there’s a process bottleneck worth fixing. As Apple Pay’s U.S. user base continues to grow past 60 million, your Apple Pay transaction volume will likely increase, and your dispute workflow needs to scale with it.

Anti-patterns to avoid: Don’t review chargeback data only when a problem becomes obvious. Don’t treat chargeback defense as a one-time setup. Don’t ignore seasonal patterns (holiday surges often bring both higher Apple Pay volume and higher dispute rates).

Success indicators: You can produce a monthly report showing Apple Pay chargeback volume, response rate, win rate, and average evidence assembly time. Trends are stable or improving.

Practical Examples: How This Plays Out

Scenario 1: The Mismatched DAN

An online apparel retailer receives a chargeback for $189. The dispute references a card number ending in 4821. The merchant searches their order system by last four digits and finds nothing. They assume it’s an error and let the deadline pass. In reality, the transaction was an Apple Pay order where the Device Account Number ended in 4821, but the customer’s actual card ended in 7603. The order, shipping confirmation, and delivery signature all existed in the system, indexed under 7603. The merchant lost $189 plus a chargeback fee because of a data-matching failure, not a fraud problem.

Fix: The retailer implements Step 1, mapping DAN identifiers alongside order records, and enables wallet-type filtering in their gateway dashboard. The next similar dispute is matched in under three minutes and won with delivery confirmation evidence.

Scenario 2: Over-Trusting Biometric Authentication

A specialty electronics store sees a cluster of five high-value Apple Pay orders ($400-$800 each) over two days, all shipping to different addresses in the same zip code. Because Apple Pay transactions include biometric verification, the store’s fraud filter assigns them a low risk score. All five orders ship. All five result in fraud chargebacks within 30 days. The cards had been provisioned to Apple Pay using intercepted verification codes.

Fix: The store adjusts its fraud screening (Step 2) to flag Apple Pay orders above $300 shipping to addresses not previously associated with the customer account. They add a manual review step for orders matching this pattern. The next attempted cluster is caught before fulfillment.

Common Mistakes and Pitfalls with Merchant Liability for Apple Pay

The most predictable failure is treating Apple Pay as inherently safe and therefore exempt from your normal fraud and dispute processes. Apple Pay eliminated more than $1 billion in fraud over the past year, but that protection operates at the ecosystem level. Your individual exposure depends on your own controls.

A second common mistake is neglecting to update your payment acceptance infrastructure as Apple Pay adoption grows. If your gateway, CRM, and helpdesk aren’t configured to handle tokenized transaction data, you’re building a backlog of unwinnable disputes.

Third, many merchants underinvest in chargeback response because they view each individual dispute as too small to justify the effort. But dispute ratios are cumulative. Letting low-dollar chargebacks go uncontested inflates your ratio and can trigger monitoring programs that impose financial penalties far exceeding the value of any single dispute.

Finally, don’t assume this is purely a technology problem. Process discipline, consistent evidence collection, and timely responses matter more than any single tool.

What to Do Next

Start with Step 1. Pull your last 90 days of Apple Pay transactions and verify you can match each one to its corresponding order, shipping record, and customer communication. If you can, you’re ahead of most merchants. If you can’t, that’s your first project.

From there, work through the framework sequentially. Each phase builds on the one before it. You don’t need to overhaul everything at once. Improving your DAN-to-order mapping alone will make your next dispute response faster and more likely to succeed.

As your mobile payment volume grows, revisit this guide periodically. The card networks update dispute rules, Apple refines its tokenization architecture, and your own transaction patterns shift. A defense process that worked six months ago may need adjustment. Treat chargeback defense as an ongoing operational discipline, not a one-time fix, and your revenue stays where it belongs.

Frequently Asked Questions

What is Apple Pay and how does it work for eCommerce merchants?

Apple Pay is a digital wallet that lets customers pay using their iPhone, iPad, Apple Watch, or Mac. When a customer adds a card to Apple Pay, the card network issues a Device Account Number (DAN) that replaces the real card number. Each transaction generates a one-time security code, and the customer authenticates with Face ID or Touch ID. For eCommerce merchants, Apple Pay appears as a payment option at checkout. You receive the DAN and transaction authorization, but never the actual card number.

Does Apple Pay’s tokenization protect merchants from chargebacks?

No. Tokenization protects card data from being intercepted or stolen during the transaction. It does not change chargeback rules, evidence requirements, or merchant liability. When a cardholder disputes an Apple Pay transaction, the dispute follows the same card network process as any other card-not-present chargeback. You still need to prove the transaction was authorized and the product or service was delivered.

Why do Apple Pay chargebacks seem harder to fight than regular card disputes?

The primary reason is the Device Account Number mismatch. The DAN used in the Apple Pay transaction differs from the card number the customer actually holds. If your order management system indexes transactions by card number, you may not be able to locate the original order when a dispute arrives referencing the DAN. This data-matching failure causes merchants to miss response deadlines on disputes they could otherwise win.

Which fraud patterns are commonly associated with Apple Pay transactions?

The most common pattern involves stolen cards provisioned to Apple Pay using intercepted bank verification codes. Once a stolen card is added to a device, every subsequent transaction passes biometric checks and appears legitimate. Watch for high-value orders to new shipping addresses, multiple orders from different devices shipping to the same location, and sudden spikes in Apple Pay volume from a single customer account.

Should I apply the same fraud filters to Apple Pay transactions as I do to regular card-not-present orders?

Not exactly. Apple Pay’s biometric authentication means the person holding the device has been verified, which reduces certain types of fraud. Overly aggressive AVS or velocity checks designed for manually keyed card numbers can generate false declines on legitimate Apple Pay orders. Calibrate your fraud rules to account for the lower baseline risk while still flagging suspicious patterns like mismatched shipping addresses or unusual order values.

How can a merchant services partner help with Apple Pay chargeback defense?

A merchant services partner with proactive chargeback defense capabilities can help you identify which disputes are worth contesting, prepare evidence packages tailored to specific reason codes, and track win rates over time. They can also flag when your dispute ratio is approaching network thresholds and recommend adjustments to your fraud screening or fulfillment workflows before problems escalate.