Cash Flow Challenges: Fix the Deposit Timing Gap

How eCommerce operators can end recurring liquidity crunches by rebuilding forecasts around daily settlement

Learn why deposit delays—not expenses or funding gaps—cause the same weekly cash crunch in eCommerce. This guide shows you how to rebuild your cash flow forecast around daily settlement and turn faster deposits into a reinvestment lever.

TL;DR

- Cash gaps are a timing problem, not a funding problem – Most eCommerce liquidity crunches happen because deposits land days after obligations are due, not because the business is unprofitable or overspending.

- Forecast from bank deposits, not from sales – Shift your projected revenue forward by your actual deposit lag to see your true daily cash position. Monthly forecasts hide the daily gaps that cause real pain.

- Align outflows to your deposit cadence – Move supplier payments, ad billing thresholds, and recurring charges to land after your highest-volume deposit days. This eliminates friction without changing your spending.

- Reduce deposit lag to next-day funding – Compressing settlement from three days to one frees two days’ worth of revenue for reinvestment and eliminates most recurring shortfalls. This is the single highest-leverage change.

- Right-size your cash buffer with real data – Use your largest actual single-day variance (times 1.5) as your reserve target. Fix the timing first, then keep only the buffer you genuinely need.

Guide Orientation: What This Covers and Who It’s For

This guide shows eCommerce operators how to forecast cash flow when deposits land daily instead of on a weekly or multi-day delay. It’s built for eCommerce managers at established online businesses (roughly 10 to 50 employees) who already have revenue flowing but keep running into the same liquidity crunch every week.

By the end, you’ll understand exactly how deposit timing distorts a cash flow forecast, how to rebuild your model around daily settlement, and how to turn faster funding into a reinvestment lever for inventory, ad spend, and vendor payments. This guide does not cover fundraising, credit lines, or expense-cutting tactics. The focus is structural: fix the timing, fix the forecast, fix the cycle.

Why Deposit Timing Is the Cash Flow Challenge That Keeps Repeating

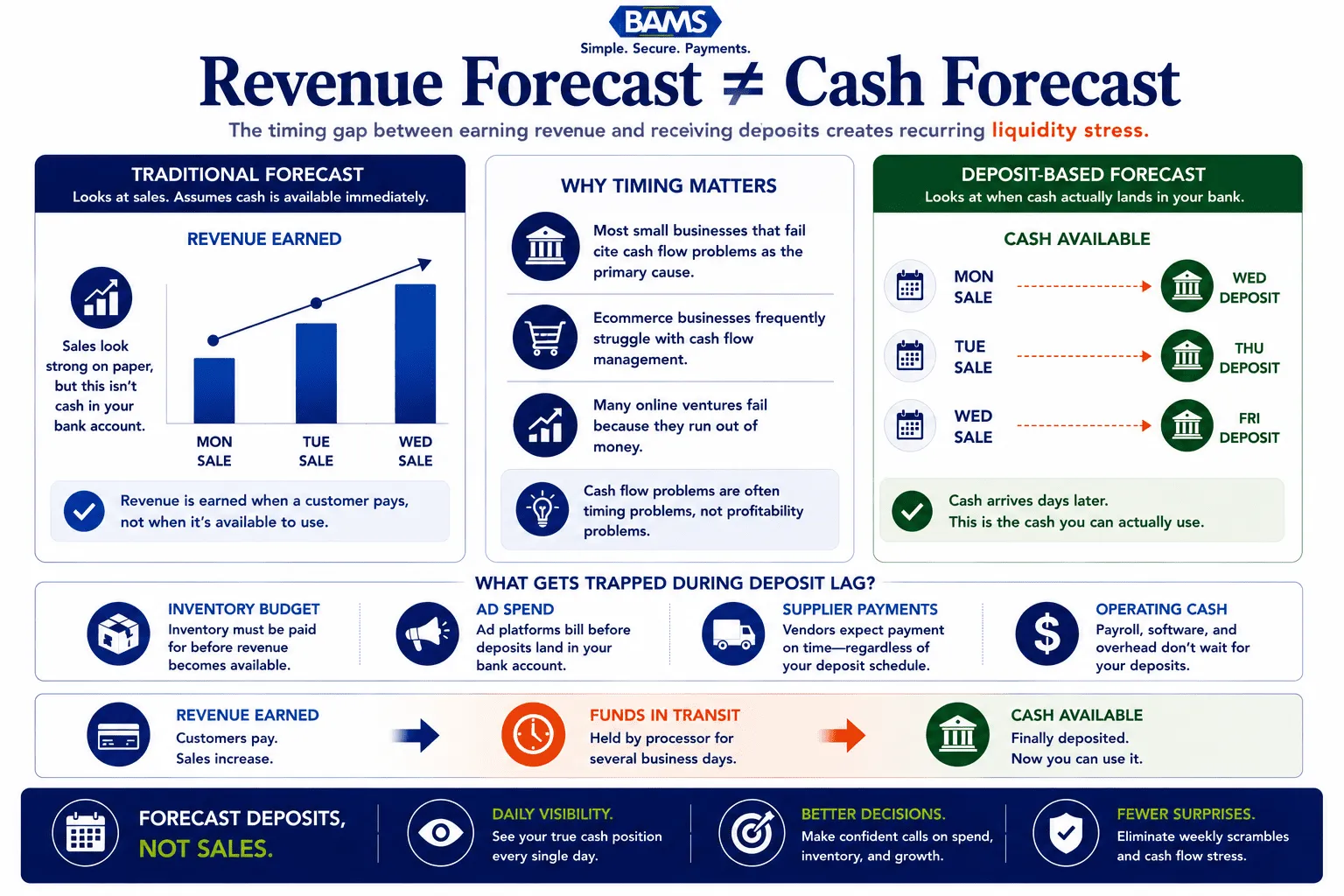

Most eCommerce forecasts track sales. The businesses with the strongest liquidity track deposits.

Most eCommerce teams treat a cash gap like a funding problem. Revenue looks healthy on paper. Margins check out. But every week, the same squeeze shows up: ad invoices hit before deposits clear, supplier payments stack up against an empty operating account, and someone scrambles to cover the gap with a credit card or a short-term draw.

The pattern repeats because the root cause is structural, not operational. Federal Reserve Small Business Survey data continues to show that cash flow management, liquidity access, and working capital constraints remain major concerns for growing businesses. The issue is that standard payment processors hold funds for multiple business days, creating a disconnect between revenue earned and cash available.

For eCommerce specifically, this timing gap is acute. You pay for inventory, shipping, and advertising before customers ever check out. When deposits lag by three to five days, you’re financing a rolling gap with money you’ve already earned but can’t touch. Around 75% of eCommerce businesses report cash flow management difficulties, and the majority of those difficulties trace back to the mismatch between when obligations come due and when funds actually arrive.

The cost of ignoring this is not abstract. Around 32% of online ventures fail because they simply run out of money. Not because demand dried up. Not because the product was wrong. Because cash wasn’t where it needed to be, when it needed to be there.

Core Concepts: The Mechanics Behind the Mismatch

Deposit Lag vs. Cash Gap

A deposit lag is the time between a customer’s payment and when that money reaches your bank account. A cash gap is the period during which your obligations exceed your available cash. The two are related but distinct. Deposit lag is the cause; the cash gap is the symptom. Shorten the lag, and the gap shrinks or disappears.

Batch Settlement and Cutoff Times

Payment processors collect transactions into batches, usually once per day. Each batch is submitted for settlement at a specific cutoff time. If your batch closes at 5 PM but your processor doesn’t initiate the transfer until the next business day, you’ve already added 24 hours of lag before banking transit time even begins. Understanding how batching and payout timing work is the first step toward controlling your cash position.

Available Cash vs. Earned Revenue

Your accounting system may show $50,000 in daily sales. Your bank account may show $12,000. The difference is in transit. Traditional cash flow forecasts often treat earned revenue as available cash, which creates a false picture of liquidity. When you forecast around daily deposits, you align the model with reality: what’s actually in your account, today, ready to deploy.

The Reinvestment Lever

Faster deposits don’t just prevent shortfalls. They create optionality. When Tuesday’s revenue is available Wednesday morning instead of Friday, you can reorder inventory sooner, capture early-payment discounts from suppliers, and fund ad spend without floating the cost on credit. This is the concept most eCommerce finance guidance misses entirely: deposit speed isn’t just a cash flow fix, it’s a reinvestment accelerator.

The Framework: Forecast, Align, Accelerate

This guide follows a three-phase framework for rebuilding your cash flow forecast around daily deposits. Each phase builds on the previous one.

- Phase 1: Forecast — Map your actual cash inflows and outflows by day, not by week or month. Identify where timing mismatches create gaps.

- Phase 2: Align — Restructure payment obligations and deposit schedules so inflows and outflows land in the right sequence.

- Phase 3: Accelerate — Reduce deposit lag to its minimum (ideally next-day or same-day funding) and use the freed-up cash to improve liquidity and reinvest faster.

The steps below walk through each phase with specific execution guidance. They’re sequential: start with Step 1 even if you think your forecast is solid. Most aren’t.

The solution isn’t more funding. The solution is fixing the timing of the money you already earned.

Step-by-Step: How to Forecast Cash Flow With Daily Deposits

Step 1: Map Your True Daily Cash Position

Objective: Know exactly how much cash is available in your operating account on any given day, separate from what you’ve earned but haven’t received.

Start by pulling 60 to 90 days of bank statements and processor settlement reports. For each day, record three numbers: opening bank balance, deposits received, and total outflows (vendor payments, payroll debits, ad platform charges, subscription fees). Don’t use your accounting software’s revenue figures here. Use actual bank credits.

Most ecommerce managers discover that their “cash flow forecast” has been a revenue forecast in disguise. Revenue accrues when a sale happens. Cash arrives when the processor settles. Those are different events on different days. If your current model doesn’t distinguish between the two, your cash flow forecast may be overstating your available cash.

Anti-patterns: Don’t average deposits across the week. Daily variance matters. A $10,000 Monday and a $2,000 Tuesday are not the same as two $6,000 days when your supplier payment hits Tuesday morning. Don’t ignore weekends and holidays, when deposits pause but obligations don’t.

Success indicators: You can state your actual available cash for any day in the past 90 days within 5% accuracy, using bank data alone.

Step 2: Identify Your Recurring Timing Gaps

Objective: Pinpoint the specific days and patterns where outflows exceed available cash, and trace those gaps to deposit lag.

With your daily cash map in hand, highlight every day where your ending balance dropped below your minimum operating threshold (the amount you need to cover the next day’s obligations). Look for patterns. Common ones include: Monday gaps caused by weekend sales that haven’t settled yet, mid-week gaps when ad platform charges hit before that week’s deposits clear, and end-of-month gaps when payroll and rent overlap with slower settlement periods.

For each gap, calculate two numbers: the size of the shortfall and the number of days between when the revenue was earned and when it arrived. This second number is your effective deposit lag. If your processor settles in three business days, a Friday sale doesn’t land until Wednesday. That’s five calendar days of lag, during which you’re financing operations with yesterday’s cash.

Anti-patterns: Don’t assume the gap is caused by overspending. If your margins are healthy and your expenses are proportional to revenue, the gap is almost certainly a timing issue. Cutting ad spend to “fix” a cash gap caused by deposit lag just shrinks your revenue without solving the structural problem.

Success indicators: You have a list of recurring gap days, each annotated with the deposit lag that caused it and the dollar amount of the shortfall.

Step 3: Rebuild the Forecast Around Settlement Dates

Objective: Create a forward-looking daily cash flow model that uses deposit dates (not sale dates) as the revenue input.

Take your revenue projections and shift them forward by your actual deposit lag. If your processor settles in two business days, Tuesday’s projected sales appear as Thursday’s projected cash. If you’re on a three-day cycle, they appear Friday. Build a simple spreadsheet or update your existing model with two columns: “Revenue Earned” and “Cash Available.” The forecast runs on the second column.

Layer in your outflows by their actual debit dates. Ad platforms typically charge on fixed cycles (weekly or when a threshold is hit). Supplier payments have specific due dates. Payroll is biweekly or semi-monthly. Map each one to the exact day it hits your account. Now you have a daily cash flow forecast that reflects reality: when money arrives and when money leaves.

This is where you start to see the structural advantage of daily deposits. If you can reduce your deposit lag from three days to one, every projected revenue line shifts two days earlier. Run the model both ways (current lag vs. next-day funding) and compare the gap days. In most cases, the majority of recurring shortfalls disappear.

Anti-patterns: Don’t build a monthly forecast and call it done. Monthly models hide the daily gaps that cause real operational pain. A month can look cash-positive while containing five days of negative balance. Don’t forget to account for processor holds, chargebacks, and reserve withholdings, which can delay portions of your deposits beyond the standard settlement window.

Success indicators: Your forecast accurately predicts your bank balance for each of the next 14 days within 10% variance, validated against actual results over two to three weeks.

Step 4: Align Outflow Timing to Inflow Cadence

Objective: Restructure when you pay obligations so they land after (not before) your deposits clear.

With a daily forecast in place, you now have the data to negotiate smarter payment schedules. Contact suppliers and ask to shift payment due dates by two to three days to align with your deposit cadence. Many suppliers will accommodate this, especially for reliable accounts. If your ad platform charges on Mondays but your heaviest deposit days are Tuesday through Thursday, adjust campaign budgets or billing thresholds so charges align with cash availability.

For recurring fixed costs (rent, SaaS subscriptions, insurance), check whether you can choose your debit date. Many vendors allow you to select a specific day of the month. Pick one that falls after your highest-volume deposit days. This sounds simple, but the cumulative effect is significant: you’re eliminating friction between inflows and outflows without spending less or earning more.

Scheduling payments exactly when due (rather than early) and using payment tools that create extra float directly addresses the timing problem behind weekly cash gaps.

Anti-patterns: Don’t pay early to “get it off the list.” Every day of float you voluntarily surrender is a day your cash isn’t working for you. Don’t ignore payment terms you’ve already negotiated. Net-30 means you have 30 days. Use them.

Success indicators: Your revised forecast shows fewer gap days, and your average daily ending balance increases without any change in revenue or expenses.

Step 5: Accelerate Cash Inflows by Reducing Deposit Lag

Objective: Compress the time between a customer’s payment and your access to those funds to one business day or less.

This is the highest-leverage step in the entire framework. Every other step optimizes around a constraint. This step removes the constraint. If your current processor settles in two to five business days, switching to next-day funding collapses your effective deposit lag to roughly 24 hours. That single change shifts every revenue line in your forecast forward and can eliminate most recurring cash gaps.

BAMS offers next-day funding with a 9 PM EST batch cutoff, which means sales processed up to 9 PM land in your account the following business day. For eCommerce operators running campaigns across time zones, that late cutoff captures a larger share of daily transactions in each batch, further reducing effective lag. FedNow Service resources continue to demonstrate how faster payment infrastructure can reduce settlement delays and improve access to working capital.

When evaluating any processor for funding speed, ask three specific questions: What is the batch cutoff time? What is the settlement timeline for each card network (Visa, Mastercard, Amex, Discover)? Are there rolling reserves or holdbacks that delay a portion of funds beyond the stated timeline? The answers determine your real deposit lag, not the marketing claim.

Anti-patterns: Don’t assume all “next-day funding” offers are equivalent. Some processors advertise next-day but impose early cutoff times (3 PM or 4 PM), which pushes evening transactions to a two-day settlement. Don’t overlook processing fees in the comparison. Faster funding at a significantly higher per-transaction cost may not improve your net cash position.

Success indicators: Your daily cash flow forecast, updated for next-day settlement, shows zero or near-zero recurring gap days. Your short-term cash buffer requirements decrease because less cash is trapped in transit.

Step 6: Build a Short-Term Cash Buffer Based on Actual Variance

Objective: Set a data-driven reserve amount that absorbs daily fluctuations without tying up excess capital.

Even with daily deposits and aligned outflows, variance happens. A supplier charges early. A chargeback pulls funds from tomorrow’s settlement. A holiday weekend creates a three-day deposit gap. You need a buffer, but the right buffer is calculated, not guessed.

Using your 90-day cash map from Step 1, find your largest single-day negative variance (the biggest gap between expected and actual ending balance). Multiply that by 1.5. That’s your minimum short-term cash buffer. It’s enough to absorb the worst day you’ve actually experienced, with a margin for the unexpected. Industry guidance often recommends six months of expenses as a safety net, but that figure is designed for businesses with multi-day deposit lag and unpredictable inflows. With daily funding and a solid forecast, your buffer can be leaner and your capital can work harder.

Park this buffer in a separate account. Don’t commingle it with operating cash. The buffer exists to absorb timing shocks, not to fund inventory or ad spend. Replenish it immediately after any draw.

Anti-patterns: Don’t skip the buffer because your forecast looks clean. Forecasts model the expected; buffers protect against the unexpected. Don’t set the buffer once and forget it. Revisit quarterly as your revenue scale and expense structure change.

Success indicators: You have a dedicated reserve account funded at your calculated minimum. You haven’t needed to use credit or delay payments to cover a timing gap in the past 30 days.

Step 7: Use Freed Capital to Accelerate Reinvestment Cycles

Objective: Redeploy the cash that was previously trapped in deposit lag into inventory, advertising, and supplier relationships that compound growth.

This is where the framework shifts from defensive (preventing gaps) to offensive (creating advantage). When your deposit lag drops from three days to one, you free up roughly two days’ worth of revenue that was previously in transit. For a business doing $30,000 per day in sales, that’s $60,000 of working capital that’s now available 48 hours sooner.

Direct that capital toward three high-return uses. U.S. Small Business Administration resources continue to emphasize the importance of maintaining healthy cash flow and reinvesting available capital into growth initiatives that strengthen business resilience.

First, reorder inventory faster. If you can place restock orders two days earlier, you reduce stockout risk and capture sales you would have otherwise missed. Second, fund ad spend from revenue rather than credit. This eliminates interest costs and lets you scale campaigns based on actual performance data from the previous day’s sales. Third, negotiate early-payment discounts with suppliers. A 2% discount for paying 20 days early (2/10 net 30) annualizes to roughly 36% return on capital. That’s a better return than almost any other use of cash in your business.

For businesses with invoice-based B2B components alongside their eCommerce operations, streamlining invoice delivery and follow-up can further accelerate cash inflows and reduce the receivables portion of your cash cycle.

Anti-patterns: Don’t reinvest all freed capital immediately. Maintain your buffer from Step 6 first. Don’t chase volume for volume’s sake. Reinvest in areas with proven return, not speculative expansion.

Success indicators: Your inventory reorder cycle has shortened. Your ad spend is funded from operating cash rather than credit. You’ve captured at least one early-payment discount from a supplier.

Practical Example: The Weekly Crunch, Before and After

Before: Three-Day Settlement

An eCommerce brand doing $25,000 per day in sales uses a processor with a three-business-day settlement cycle. Friday and Saturday sales ($50,000 combined) don’t arrive until Wednesday. Meanwhile, a $15,000 ad platform charge hits Monday, a $20,000 supplier payment is due Tuesday, and payroll of $18,000 debits Wednesday morning. By Tuesday, the operating account is $12,000 short. The manager transfers from a reserve, pays a credit card float fee, or delays the supplier payment. This happens nearly every week.

After: Next-Day Settlement

The same brand switches to a processor with next-day funding. Friday’s $25,000 arrives Saturday (or Monday for banks that don’t process weekend deposits). Saturday’s $25,000 arrives Monday. The Monday ad charge is covered by Friday/Saturday revenue. The Tuesday supplier payment is covered by Monday’s deposit. Payroll on Wednesday is covered by Tuesday’s deposit. The weekly crunch disappears. No reserve draw. No float fees. No delayed supplier payments.

The only variable that changed was deposit timing. Revenue stayed the same. Expenses stayed the same. The cash gap was never a funding problem. It was a timing problem.

Common Mistakes and Pitfalls

- Forecasting from revenue, not from bank deposits. This is the most common error and the hardest to catch because the numbers look right at the monthly level. They’re wrong at the daily level, which is where cash gaps live.

- Treating every cash gap as an emergency. When you don’t have a daily forecast, every shortfall feels unexpected. With the right model, most gaps are predictable weeks in advance, which means they’re preventable.

- Ignoring processor holds and reserves. Some processors withhold a percentage of deposits as a rolling reserve. If your forecast doesn’t account for this, your projected cash is higher than your actual cash. Ask your processor for the exact reserve terms in writing.

- Over-buffering instead of fixing the lag. Holding excessive reserves is expensive. Every dollar in a buffer account is a dollar not working in your business. Fix the timing first, then right-size the buffer.

- Optimizing expenses when the problem is inflow timing. Cutting costs to cover a timing gap is like dieting to fix a broken watch. The problem isn’t how much you’re spending. It’s when the money shows up.

What to Do Next

Start with Step 1. Pull your last 90 days of bank statements and processor settlement reports. Map your actual daily cash position. This single exercise will reveal whether your current forecast reflects reality or a comfortable approximation of it.

If the data confirms recurring timing gaps, work through Steps 2 through 5 in order. The framework is designed to be revisited as your business scales, so treat it as a living model rather than a one-time project. Update your daily forecast weekly for the first month, then biweekly once the model stabilizes.

The goal isn’t a perfect forecast. It’s a forecast accurate enough to make deposit timing a strategic advantage rather than a recurring source of stress. When you know exactly when cash arrives and when it leaves, you stop reacting to gaps and start using your capital with intention.

Frequently Asked Questions

What is a cash flow acceleration strategy?

A cash flow acceleration strategy is any systematic approach to getting cash into your operating account faster. For eCommerce businesses, the most direct lever is reducing deposit lag from your payment processor. Switching from a three-day to a next-day settlement cycle compresses the gap between earning revenue and accessing it, which eliminates most timing-driven shortfalls without requiring you to cut expenses or secure outside funding.

How does deposit timing affect cash flow forecasting?

Deposit timing determines when earned revenue becomes available cash. A forecast built on sale dates overstates your daily cash position by the number of days your processor holds funds. For accurate forecasting, shift projected revenue forward by your actual deposit lag. If your processor settles in two business days, Wednesday’s sales appear as Friday’s available cash in the forecast.

How can eCommerce businesses improve liquidity without taking on debt?

The fastest path is to reduce the time between a customer’s payment and your access to those funds. Next-day funding from your payment processor frees working capital that was previously trapped in transit. Beyond that, aligning outflow due dates with your deposit cadence and negotiating early-payment discounts with suppliers can improve liquidity without borrowing.

How large should a short-term cash buffer be for an eCommerce business?

Rather than using a generic rule like “six months of expenses,” calculate your buffer from actual data. Find your largest single-day negative variance over the past 90 days and multiply by 1.5. This gives you a buffer sized to your real risk profile. Businesses with daily deposits and aligned outflows typically need a smaller buffer than those with multi-day settlement lag.

Why do profitable eCommerce businesses still run into cash flow problems?

Profitability is measured over time (monthly, quarterly, annually), but cash obligations hit on specific days. A business can be profitable on a monthly basis while being cash-negative on a Tuesday because deposits haven’t cleared. This is why around 82% of small business failures are attributed to cash flow problems, not lack of profitability.

How can businesses improve cash flow forecasting with real-time data?

Connect your bank feed and processor settlement reports to your forecasting model so that actual deposit amounts update daily. Compare projected vs. actual cash for each day and refine your assumptions weekly. Over time, your model will reflect your true deposit patterns, seasonal variance, and the impact of processor holds or chargebacks, giving you a forecast you can actually act on.