How Your eCommerce Payment Gateway Affects Cash Flow

A practical guide to evaluating payment processors for faster deposits and healthier operations

Learn how deposit timing from your payment gateway creates cash flow strain and what features to prioritize when switching. This guide covers practical selection criteria for eCommerce managers ready to optimize their payment stack.

TL;DR

- Deposit timing directly impacts operations – The gap between customer payment and fund availability creates real costs through missed supplier discounts, credit line usage, and delayed inventory purchases.

- Audit before you switch – Calculate your actual funding timeline and effective processing rate using bank statements, not provider dashboards. This baseline reveals whether switching is worth the effort.

- Prioritize funding speed over marginal rate savings – A provider charging slightly more but funding next-day often delivers better total value than the cheapest option with three-day funding.

- Plan migration carefully – Run parallel processing during transition, avoid peak sales periods, and systematically handle stored payment methods to prevent disruption.

- Monitor continuously after switching – Track funding timing, approval rates, and effective costs monthly. Providers sometimes deliver excellent onboarding service that degrades over time.

What This Guide Covers and Who It’s For

This guide helps eCommerce managers at established online businesses solve one specific problem: delayed deposits that strangle cash flow. If you manage payments for a company with 10 to 50 employees and find yourself waiting days (or longer) to access your revenue, this is for you.

By the end, you’ll understand exactly how your current eCommerce payment gateway affects deposit timing, what features to prioritize when evaluating alternatives, and how to build a payment processing stack that delivers funds faster. We’ll focus on practical selection criteria, not theoretical comparisons.

This guide does not cover setting up your first payment system from scratch or international expansion strategies. It assumes you already process online transactions and want to optimize your existing operations.

Why Deposit Timing Matters More Than Ever

The gap between when customers pay and when you access those funds creates real operational strain. You’ve made the sale, delivered the product, but your bank account doesn’t reflect it for three, five, sometimes seven business days. Meanwhile, supplier invoices arrive, payroll deadlines approach, and inventory needs restocking.

Modern payment infrastructure is evolving rapidly. According to Visa, optimized payment systems are designed to process transactions securely while maintaining speed and efficiency.

The companies winning in eCommerce aren’t just selling better products. They’re operating with better cash flow mechanics.

Consider what delayed deposits actually cost you. Emergency credit lines carry interest. Supplier early payment discounts go unclaimed. Growth opportunities pass because capital sits in processing limbo. For mid-sized eCommerce operations, these friction costs compound into significant annual losses that rarely appear on any single line item.

The shift toward faster payment processing solutions isn’t optional anymore.

Core Concepts: Understanding Payment Flow and Deposit Timing

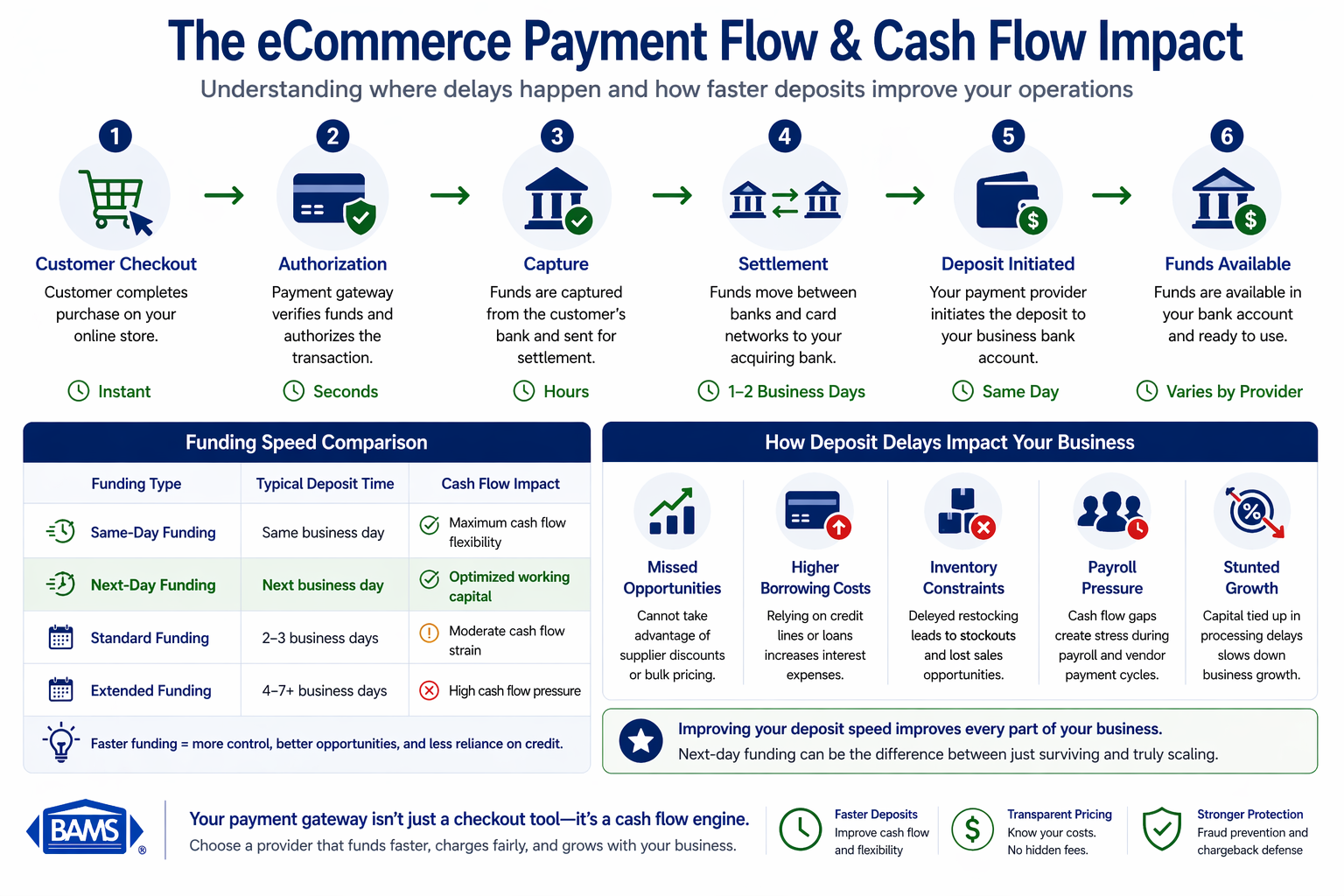

Understanding the full payment flow reveals where delays happen and how faster funding improves cash flow and business operations.

The Transaction Timeline

When a customer completes checkout, their payment doesn’t teleport into your account. It moves through authorization (verifying funds exist), capture (initiating the transfer), settlement (actual movement between banks), and finally deposit (funds available to you). Each stage introduces potential delays.

Most deposit delays occur during settlement and funding. Your gateway authorizes instantly, but the actual money movement depends on your processor’s banking relationships and funding schedule. This is where providers differ dramatically.

Funding Windows: What Actually Varies

Standard funding takes two to three business days. Next-day funding delivers deposits within 24 hours of batch close. Same-day funding (rare and often expensive) provides access within hours. The difference between standard and next-day funding means your Tuesday sales hit your account Wednesday instead of Friday.

The Hidden Cost of “Free” Processing

Some payment facilitators advertise low upfront fees but build delays into their funding model. They earn interest on your money while it sits in their settlement accounts. A dedicated merchant services account typically offers faster funding because the provider’s business model doesn’t depend on holding your funds.

According to the Federal Reserve, interchange fee structures significantly impact overall processing costs, reinforcing the importance of evaluating both cost and funding speed together.

PCI Compliance and Speed

The PCI Security Standards Council highlights that strong compliance and security frameworks are essential to protect transactions without introducing operational delays.

When compliance is built into your gateway infrastructure, you avoid the manual processes and delayed batching that often accompany less sophisticated setups.

The Cash Flow Optimization Framework

Transforming your payment operations requires addressing four interconnected areas: funding speed, fee transparency, security infrastructure, and support responsiveness. These aren’t independent features to check off. They form a system where weakness in one area undermines the others.

Funding speed determines when you can deploy revenue. Fee transparency ensures you’re not paying hidden costs that offset speed benefits. Security infrastructure (including chargeback defense) protects the revenue you’ve earned. Support responsiveness means problems get solved before they cascade into cash flow disruptions.

The framework moves from assessment (understanding your current state) through evaluation (comparing alternatives) to implementation (switching without disruption) and optimization (ongoing improvement). Each phase builds on the previous one.

Step 1: Audit Your Current Payment Performance

Objective: Establish baseline metrics for deposit timing, effective fee rates, and dispute resolution so you can measure improvement.

Pull three months of transaction data and calculate your actual funding timeline. Don’t rely on what your provider promises. Measure when batches close versus when funds appear in your bank account. Note variations by day of week and transaction type.

Calculate your effective processing rate by dividing total fees paid by total volume processed. This single number often reveals costs hidden across multiple line items. Include gateway fees, transaction fees, batch fees, and any monthly charges.

Document your chargeback rate and resolution outcomes. Each payment type carries different dispute patterns. Understanding your current exposure helps you evaluate whether a new provider’s chargeback defense program offers real value.

Avoid: Accepting provider dashboards at face value. Cross-reference with your actual bank statements. Providers sometimes report “deposit date” as the date they initiate transfer, not when funds clear.

Success indicator: You can state your average funding time to the hour, your effective rate to two decimal places, and your chargeback win rate as a percentage.

Step 2: Define Your Non-Negotiable Requirements

Objective: Create a prioritized list of must-have features that eliminates unsuitable providers immediately.

Start with funding speed. If next-day funding is essential for your operations, any provider without it is automatically disqualified. Don’t let sales conversations convince you to compromise on requirements you’ve identified as critical.

Map your integration requirements precisely. If you run Shopify, you need a payment gateway for Shopify that connects without custom development. If you use WooCommerce, verify the payment gateway for WooCommerce integration is maintained and current. Platform compatibility issues cause implementation delays that extend your time with suboptimal funding.

Consider your transaction profile. High average order values, recurring billing solutions, or B2B payment gateways each require specific capabilities. Multi-currency payment processing matters if you sell internationally. List what you actually need, not what sounds impressive.

Avoid: Creating a requirements list so long that no provider qualifies. Focus on five to seven genuinely critical features. Everything else is negotiable.

Success indicator: You can explain why each requirement matters to your specific business, with a dollar figure or operational impact attached.

Step 3: Evaluate Providers Against Real-World Criteria

Choosing the right payment gateway requires evaluating funding speed, pricing transparency, reliability, and long-term scalability.

Objective: Compare viable providers using criteria that predict actual performance, not marketing claims.

Request sample merchant statements from each provider. A legitimate secure payment gateway provider will show you exactly how fees appear and how funding timing works for businesses similar to yours. Vague responses here predict vague billing later.

Ask specifically about their banking relationships and funding infrastructure. Direct banking relationships typically enable faster funding than providers who rely on intermediaries.

Evaluate support structure before you need it. Will you have a dedicated account manager or submit tickets into a queue? For eCommerce operations where payment issues directly equal lost revenue, the difference matters. Test response times during your evaluation by asking technical questions.

Examine their transaction fee structure in detail. Look for interchange-plus pricing (transparent) versus tiered or flat-rate pricing (often more expensive at scale). Understand how they handle different card types, as rewards cards and corporate cards typically carry higher interchange.

Avoid: Choosing based on the lowest quoted rate without understanding what’s included. A provider offering 2.5% flat rate often costs more than one offering interchange-plus with a 0.3% margin.

Success indicator: You can project your monthly costs with each provider using your actual transaction data, not their calculator with default assumptions.

Step 4: Verify Security and Compliance Infrastructure

Objective: Confirm that faster funding doesn’t come at the cost of security vulnerabilities or compliance gaps.

A secure payment gateway should provide PCI DSS compliance documentation without hesitation. Ask for their Attestation of Compliance and verify its current status. Compliance lapses expose you to liability and can result in processing suspension.

Understand their tokenization approach. When customer payment data is tokenized, you reduce your PCI scope and simplify your own compliance requirements. This matters for recurring billing and stored payment methods.

Evaluate their fraud prevention tools. Machine learning fraud detection, velocity checks, and address verification services should be standard. Ask how they balance fraud prevention with approval rates, as overly aggressive fraud rules reject legitimate customers.

Review their chargeback defense program specifically. The global payment gateway market is projected to grow, driven partly by demand for integrated payment solutions that handle disputes proactively rather than reactively.

Avoid: Assuming all providers handle security equally. Ask about breach history, incident response procedures, and how they communicate security issues to merchants.

Success indicator: You have documentation confirming PCI compliance, understand exactly what security features are included versus add-on, and know their chargeback response process.

Step 5: Plan Your Migration to Minimize Disruption

Objective: Switch providers without creating gaps in payment acceptance or funding delays during transition.

Never cut over completely on day one. Run parallel processing for at least two weeks, routing a percentage of transactions through your new provider while maintaining your existing setup. This reveals integration issues before they affect all your revenue.

Coordinate timing with your business cycle. Avoid switching during peak sales periods or when you have unusual cash flow needs. The best migration windows are during predictably slower periods when you can absorb any temporary disruption.

Update stored payment methods systematically. If you offer recurring billing, you’ll need to migrate tokenized card data or re-collect payment information from subscribers. Plan this communication carefully to minimize customer friction.

Document everything during migration. Track which transactions process through which provider, monitor funding timing from both, and keep detailed notes on any issues. This documentation proves invaluable if disputes arise later.

Avoid: Rushing migration to escape your current provider’s next billing cycle. A botched transition costs more than one additional month of suboptimal processing.

Success indicator: You complete migration with zero missed transactions, funding arrives on the new provider’s promised schedule from day one, and customer-facing checkout experience remains unchanged.

Step 6: Optimize Ongoing Operations

Objective: Extract maximum value from your new payment infrastructure through continuous monitoring and adjustment.

Set up automated reporting that tracks the metrics you established in Step 1. Compare actual performance against promised performance weekly for the first quarter, then monthly thereafter. Providers sometimes deliver excellent service during onboarding that degrades over time.

Review your batch timing and adjust if needed. Batching earlier in the day often means faster next-day funding. Understand your provider’s cutoff times and align your operations accordingly.

Monitor approval rates alongside fraud rates. The goal isn’t zero fraud. It’s optimal balance between protection and conversion. If your approval rate drops after switching providers, investigate whether fraud settings need calibration.

Stay informed about new payment methods. Ensure your gateway supports emerging payment preferences.

Avoid: Setting and forgetting your payment configuration. The payments landscape evolves continuously, and providers update their offerings. Annual reviews ensure you’re not missing improvements.

Success indicator: Your funding timeline meets or exceeds promised performance, effective rates remain stable, and you proactively identify optimization opportunities before they become problems.

Practical Example: How Faster Funding Changes Operations

Consider a mid-sized eCommerce operation processing $500,000 monthly. With standard three-day funding, approximately $50,000 sits in processing limbo at any given time. Switching to guaranteed next-day funding reduces that float to roughly $16,000, freeing $34,000 for immediate operational use.

That $34,000 difference enables paying suppliers within discount windows (often 2% savings for payment within 10 days), avoiding short-term credit line draws, and purchasing inventory at optimal times rather than when funds finally arrive. Over a year, these operational improvements often exceed the cost difference between providers.

The Yes Bank partnership with Amazon Pay demonstrates how financial institutions are investing in real-time payment infrastructure to reduce friction. While that example involves UPI in India, the underlying principle applies globally: payment systems that move money faster create competitive advantages for merchants.

Alternatives to traditional payment facilitators often provide these speed advantages because their business model centers on merchant service rather than float income.

Common Mistakes That Undermine Cash Flow Improvements

The most frequent error is focusing exclusively on per-transaction rates while ignoring funding speed. A provider charging 0.1% less but funding two days slower costs you more in operational friction than you save in processing fees.

Many eCommerce managers underestimate migration complexity, particularly around recurring billing and stored payment methods. Rushed transitions result in failed subscription renewals and customer complaints that damage relationships.

Another common mistake is choosing integrated payment solutions based on platform recommendations alone. Your eCommerce platform may have preferred partners, but those partnerships often reflect revenue sharing arrangements rather than optimal merchant outcomes.

Finally, businesses often fail to renegotiate terms as they grow. Competition for merchant business remains intense. Your leverage increases with volume, so use it.

What to Do Next

Start with Step 1. Pull your last three months of transaction data this week and calculate your actual funding timeline and effective rate. This baseline takes two hours and immediately reveals whether your current setup deserves scrutiny.

If your audit reveals significant gaps between what you’re paying (in fees and delayed access) and what’s available in the market, move through the remaining steps at a pace that matches your operational capacity. Rushing creates errors, but unnecessary delay extends the cost of suboptimal processing.

Use this guide as a reference rather than a checklist. Your specific situation will require adapting these steps to your transaction profile, platform requirements, and growth trajectory. The framework remains constant even as details vary.

Frequently Asked Questions

What is a payment gateway and why is it important for eCommerce?

A payment gateway is the technology that securely transmits transaction data between your online store, the customer’s bank, and your merchant account. It handles authorization, encryption, and communication between all parties. For eCommerce, your gateway directly affects checkout conversion rates, deposit timing, and security compliance. A slow or unreliable gateway means lost sales and delayed access to revenue.

How do I choose the best payment gateway for my business?

Start by identifying your non-negotiable requirements: funding speed, platform integration (Shopify, WooCommerce, or custom), transaction volume, and payment types you need to accept. Then evaluate providers against these criteria using actual merchant statements, not marketing materials. Prioritize transparent pricing, dedicated support, and proven reliability over the lowest quoted rate.

When should I consider switching my payment gateway?

Consider switching when your funding timeline exceeds two business days, your effective processing rate seems high compared to alternatives, you experience frequent technical issues affecting checkout, or your support requests go unanswered. Also evaluate switching when your business has grown significantly since you chose your current provider, as your leverage for better terms has likely increased.

Which payment gateways support international transactions?

Most established payment gateways support international transactions, but capabilities vary significantly. Key factors include multi-currency payment processing (settling in local currencies versus converting everything to USD), supported countries, and international card network coverage. Verify specific country support and understand the fee structure for cross-border transactions before committing.

How does a secure payment gateway protect online transactions?

Secure payment gateways use encryption (typically TLS) to protect data in transit, tokenization to replace sensitive card data with non-sensitive equivalents, and fraud detection tools to identify suspicious transactions. They maintain PCI DSS compliance, which establishes security standards for handling cardholder data. This infrastructure protects both your customers and your business from data breaches and fraud losses.

What’s the difference between a payment gateway and a payment processor?

The payment gateway handles the front-end communication, securely capturing and transmitting transaction data. The payment processor handles the back-end movement of funds between banks. Many providers offer both services bundled together, but they’re technically distinct functions. Understanding this distinction helps you evaluate whether you need to switch one or both components of your payment stack.