Faster Deposit Strategies eCommerce: Compare What Works

Faster Deposit Strategies Compared: Which Accelerates Cash Flow?

A practical breakdown of next-day funding, payment optimization, and processor switching for eCommerce businesses

Compare three proven strategies for getting your money faster: next-day funding, payment optimization, and processor switching. Learn which approach fits your transaction volume and cash flow needs.

TL;DR

- Next-day funding is the fastest path to improved cash flow – Low implementation effort with immediate impact, ideal for businesses currently waiting 2-3+ days for deposits

- Payment optimization captures more revenue first – If your authorization rate is below 95%, fix that before focusing on deposit speed since you can’t deposit failed transactions

- Processor switching pays off when current terms are outdated – Migration takes 2-4 weeks but often recovers costs within 90 days through better rates and faster settlement

- Combine strategies for maximum impact – The best approach layers next-day funding, authorization optimization, and chargeback prevention together

- Weekend banking remains a universal limitation – Even the fastest processors can’t deposit Saturday sales until Monday when banks reopen

The Cash Flow Problem Every eCommerce Manager Knows Too Well

You made sales yesterday. Your customers paid. But that money? It’s sitting somewhere in the payment processing pipeline, unavailable for restocking inventory, paying suppliers, or funding your next marketing push.

For eCommerce managers at established online businesses, faster deposit strategies aren’t a luxury. They’re the difference between seizing growth opportunities and watching them slip away while waiting for funds to clear. Card payment costs include interchange fees, network assessments, and processor charges, which together define how revenue flows through the payment system and impacts merchant cash flow as outlined by the Federal Reserve.

This comparison breaks down the major approaches to accelerating your deposits, analyzing what actually moves the needle on cost-effective payment processing and which strategies deliver real results for businesses processing significant transaction volumes.

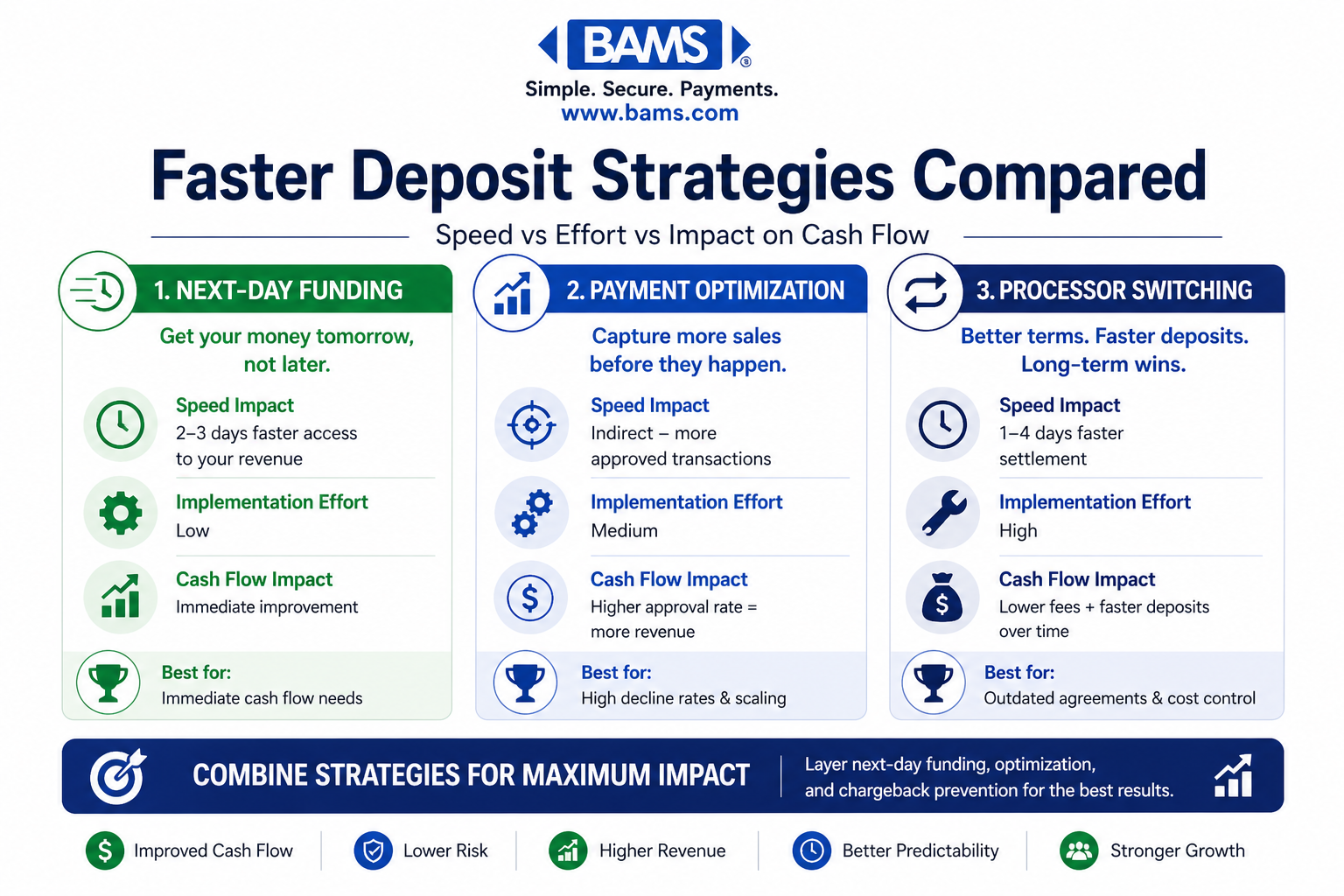

Quick Verdict: Which Faster Deposit Strategy Fits Your Business?

A side-by-side comparison of faster deposit strategies, showing how each approach impacts speed, effort, and overall cash flow performance.

Choose next-day funding if you need predictable, daily access to revenue without taking on debt or restructuring your payment stack. It’s the most direct path to improved cash flow.

Choose payment optimization if your authorization rates are below 95% and you’re losing revenue to failed transactions before deposits even become relevant.

Choose processor switching if you’re locked into 3-5 day settlement windows and your current provider won’t negotiate. The switching costs often pay for themselves within 90 days.

|

Strategy |

Speed Impact |

Implementation Effort |

Cost |

Best For |

|---|---|---|---|---|

|

Next-Day Funding |

2-3 days faster |

Low |

$0-0.5% per transaction |

Immediate cash flow needs |

|

Payment Optimization |

Indirect (more successful transactions) |

Medium |

Technology investment |

High decline rates |

|

Processor Switching |

1-4 days faster |

High |

Migration costs |

Outdated agreements |

|

Hybrid Approach |

Maximum impact |

High |

Varies |

Growth-focused businesses |

What Makes Deposits Faster: The Evaluation Criteria

Before comparing strategies, you need to understand what actually determines deposit speed. Not all “fast” claims are equal. Payment timelines depend on how transactions move between banks, networks, and processors, with settlement speed influenced by batching, risk controls, and processing infrastructure as outlined by Visa.

Settlement Window

The time between transaction authorization and funds hitting your bank account. Standard processing runs 2-3 business days. Guaranteed next-day funding cuts this to 24 hours or less.

Batch Processing Timing

When your processor batches transactions affects deposit timing. A 10 PM cutoff means today’s sales deposit tomorrow. A 6 PM cutoff might push afternoon sales to the following day.

Authorization Success Rate

Money you don’t capture can’t be deposited. Streamlined processes that reduce friction increase successful transactions, which means more revenue reaching your account.

Reserve Requirements

Some processors hold a percentage of your deposits as reserves, especially for eCommerce. Lower reserves mean faster access to more of your money.

Weekend and Holiday Handling

Does your processor work weekends? Friday sales depositing Monday versus Tuesday makes a real difference for weekly cash flow.

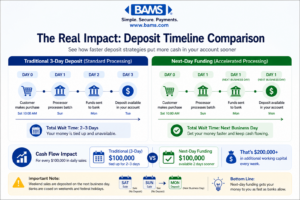

Strategy 1: Next-Day Funding Programs

A timeline comparison showing how next-day funding accelerates access to revenue compared to standard 2–3 day settlement cycles.

How It Works

Next-day funding accelerates the standard settlement timeline. Instead of waiting 2-3 business days for batched transactions to clear, you receive funds the following business day. Some providers even offer same-day funding for transactions processed before specific cutoff times.

Strengths

Implementation is straightforward. You’re not changing your checkout flow, payment gateway, or customer experience. The speed improvement is immediate and consistent.

For businesses with tight margins or seasonal inventory needs, predictable daily deposits transform cash flow management. You can reorder stock, pay suppliers on time, and avoid short-term financing.

Core deposit growth at U.S. commercial banks accelerated to 4% during the first three quarters of 2025, reflecting broader recognition that deposit velocity matters for business health.

Limitations

Next-day funding sometimes carries a small per-transaction fee (typically 0.1-0.5%). For high-volume, low-margin businesses, this adds up.

It also doesn’t fix underlying issues. If your authorization rates are poor or you’re losing sales to cart abandonment, faster deposits on fewer successful transactions only partially solves your problem.

Verdict

Next-day funding wins for businesses that need immediate, low-effort improvement to cash flow. It’s the right starting point for most eCommerce operations, especially those processing $50,000+ monthly who can negotiate favorable terms.

Strategy 2: Payment Optimization for Higher Authorization Rates

How It Works

Payment optimization focuses on capturing more revenue from existing traffic. This includes authorization rate improvement through retry logic, network token optimization, and intelligent routing that sends transactions through the most likely-to-succeed pathways.

Strengths

The math is compelling. If you’re processing $500,000 monthly with a 92% authorization rate, improving to 96% captures an additional $20,000 in revenue. That’s money that deposits into your account instead of disappearing into failed transaction limbo.

Digital platforms now enable account processes in under four minutes, reducing abandonment and accelerating customer acquisition. The same principle applies to payment flows: friction kills conversions.

Payment optimization also improves customer payment recovery. Smart retry logic, updated card-on-file systems, and dunning management recover revenue from failed recurring payments that would otherwise churn.

Limitations

Implementation requires technical resources. You’ll need to evaluate your current gateway capabilities, potentially integrate new tools, and monitor performance over time.

Results vary by business type. If your authorization rates are already above 97%, optimization offers diminishing returns compared to faster settlement.

Verdict

Payment optimization wins for businesses with authorization rates below 95% or significant recurring revenue. The upfront investment pays compound returns as you capture more transactions that then deposit faster.

Strategy 3: Switching Payment Processors

How It Works

Sometimes the fastest path to faster deposits is finding a processor that prioritizes speed. Many eCommerce businesses operate on legacy agreements with 3-5 day settlement windows, unclear fee structures, and limited support.

Switching to a processor offering next-day funding, transparent pricing, and dedicated account management can transform your cash flow without ongoing per-transaction fees.

Strengths

A full processor switch addresses multiple issues simultaneously. You can negotiate better rates, faster settlement, lower reserves, and improved support in a single transition.

Industry-wide trends show banks reducing reliance on expensive wholesale funding in favor of relationship-based strategies. Payment processors are following suit, competing on service quality rather than just rates.

For established businesses processing significant volume, switching leverage is real. Processors want your business and will compete for it.

Limitations

Migration isn’t trivial. You’ll need to update payment gateway integrations, transfer recurring billing relationships, and manage a transition period where both systems may run simultaneously.

There’s also risk. A new processor relationship is unproven. Customer service quality and actual support responsiveness only become clear after you’ve committed.

Verdict

Processor switching wins for businesses stuck with outdated agreements or processors unwilling to negotiate. If your current provider won’t offer next-day funding or competitive rates, the market has better options.

Faster Deposit Strategies: Use Case Mapping

If You’re Managing Seasonal Inventory

Choose next-day funding. When you need to reorder fast-moving products before they sell out, waiting 3 days for deposits means missed sales. Predictable daily cash flow lets you restock in rhythm with demand.

If You’re Scaling Rapidly

Choose a hybrid approach combining next-day funding with payment optimization. Growth amplifies both opportunities and problems. Capturing more transactions and accessing that revenue faster compounds your scaling capacity.

If You Have High Recurring Revenue

Prioritize payment optimization and customer payment recovery. Failed subscription renewals represent ongoing revenue loss. Smart retry logic and card updater services recover 10-30% of otherwise-churned customers.

If You’re Processing High-Ticket Items

Consider processor switching for better reserve terms. High average order values often trigger higher reserve requirements. A processor experienced with your business model may offer more favorable terms.

If Your Authorization Rates Are Already Strong

Focus purely on settlement speed. If you’re capturing 97%+ of transactions, optimization offers limited upside. Next-day funding delivers immediate, measurable improvement.

What None of These Strategies Fully Solve

Every faster deposit strategy has blind spots worth acknowledging.

Weekend banking limitations persist. Even next-day funding can’t deposit Saturday sales until Monday when banks are closed. True 7-day-a-week settlement remains rare.

Chargebacks still disrupt cash flow. A disputed transaction reverses your deposit regardless of how fast it arrived. Proactive chargeback prevention strategies complement but don’t replace deposit speed improvements.

International transactions add complexity. Cross-border payments involve additional settlement layers that even the fastest domestic processors can’t fully accelerate.

Migration and Switching: What It Actually Takes

Switching Costs

Expect 2-4 weeks of implementation time for a full processor switch. Development resources for gateway integration typically run 20-40 hours depending on your platform complexity.

Most processors don’t charge explicit switching fees, but watch for early termination fees from your current provider. Review your existing agreement before initiating conversations.

Data Portability

Transaction history generally stays with your old processor. You’ll maintain access for reporting and dispute resolution, but historical data won’t migrate to your new provider.

Recurring billing tokens are the critical consideration. Some processors use proprietary tokenization that doesn’t transfer. You may need to re-collect payment information from subscription customers.

When Switching Makes Sense

Switch when the math works. If faster deposits and better rates save you $2,000 monthly, a $5,000 migration investment pays back in under 90 days. Commercial balances rose 2% between Q3 2023 and Q1 2024 as businesses optimized their banking relationships, and payment processing deserves the same strategic attention.

The Integrated Approach: Combining Strategies for Maximum Impact

The most effective cost-effective payment processing approach combines multiple strategies rather than relying on any single solution. A modern integrated payment gateway helps streamline transaction flow, improve authorization outcomes, and support faster settlement across your entire payment stack.

Layer 1: Foundation

Start with a processor offering next-day funding as a standard feature, not a premium add-on. This establishes your baseline deposit speed.

Layer 2: Optimization

Implement authorization rate improvement through smart routing and retry logic. Every additional percentage point of successful transactions compounds your daily deposits.

Layer 3: Protection

Add chargeback prevention to protect the deposits you’re receiving. Disputes reverse your cash flow gains and often carry additional fees.

Layer 4: Monitoring

Use transaction reporting to identify patterns. Which products have higher decline rates? Which times of day see more failed authorizations? Data drives continuous improvement.

Final Recommendation: Your Path to Faster Deposits

For most eCommerce managers at established businesses, the right sequence is clear.

First, evaluate your current settlement timeline. If you’re waiting more than 2 business days for deposits, faster funding should be your immediate priority. It’s the lowest-effort, highest-impact change available.

Second, assess your authorization rates. Below 95%? Payment optimization will capture revenue you’re currently losing, which then deposits faster.

Third, review your processor relationship holistically. Transparent pricing, dedicated support, and proactive chargeback defense matter as much as raw deposit speed.

The goal isn’t just faster deposits. It’s predictable, optimized cash flow that lets you focus on growing your business instead of managing payment headaches. The right combination of faster deposit strategies gets you there.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposit strategies are approaches that accelerate the time between when a customer pays and when those funds reach your bank account. Common strategies include next-day funding programs, payment optimization to increase successful transactions, and switching to processors with shorter settlement windows. The right strategy depends on your current deposit timeline and transaction volume.

Why is payment optimization important for businesses?

Payment optimization increases the percentage of transactions that successfully complete. If your authorization rate is 92% instead of 96%, you’re losing 4% of potential revenue before it ever becomes a deposit. For a business processing $500,000 monthly, that’s $20,000 in lost sales. Optimization captures that revenue, which then deposits into your account.

How can I improve my payment authorization rates?

Start by analyzing where declines occur. Common improvements include implementing smart retry logic for soft declines, using network tokens instead of raw card numbers, enabling card-on-file updater services for recurring payments, and routing transactions through optimal networks based on card type and issuing bank.

Which payment processing fees can I reduce to optimize costs?

Focus on interchange optimization through accurate transaction data (Level 2 and Level 3 processing for B2B), negotiate processor markup rates based on your volume, eliminate unnecessary add-on fees, and review your statement for services you don’t use. Transparent pricing models like cost-plus make it easier to identify savings opportunities.

What role does fraud protection play in payment optimization?

Effective fraud protection prevents chargebacks that reverse your deposits and carry additional fees. However, overly aggressive fraud rules decline legitimate transactions, hurting your authorization rate. The balance is fraud protection that blocks actual fraud while approving good customers quickly.

When should I consider switching payment processors?

Consider switching when your current processor won’t offer next-day funding, your rates are significantly above market for your volume, you’re experiencing poor support responsiveness, or your settlement window exceeds 3 business days. Calculate the total cost of switching against projected savings to determine if the math works.

Sources