Faster Payment Settlement + Lower Fees: A Guide

How connecting interchange optimization with settlement speed creates a compounding cash flow advantage for eCommerce

Learn how to audit your processing setup, qualify for lower interchange tiers, and link those transaction cost savings to faster payment settlement. This guide shows mid-market eCommerce operators how the combined effect drives reinvestable cash flow.

TL;DR

- Your effective processing rate is the only number that matters — Divide total fees by total volume on your last three statements. If the gap between your quoted rate and effective rate exceeds 0.3%, you have recoverable savings.

- Level 2/3 data qualification is the biggest hidden opportunity for B2B eCommerce — Most processors claim to support it, but many don’t actually pass the required data fields. Request a transaction-level qualification report to verify, and expect savings of 0.3% to over 1.0% per transaction.

- Interchange-plus pricing gives you the transparency to control costs — Bundled or tiered pricing obscures where your money goes and almost always costs more on B2B and corporate card transactions.

- Faster settlement compounds your fee savings — Reducing your effective rate saves money, but getting those savings into your bank account one to two days sooner frees working capital you can reinvest immediately, reducing reliance on credit lines.

- Quarterly audits prevent fee creep — Interchange tables change twice a year, processors adjust markups, and your business evolves. Treat payment optimization as an ongoing discipline, not a one-time project.

Guide Orientation: What This Covers and Who It’s For

This guide is for eCommerce managers at established online businesses (roughly 10 to 50 employees) who suspect their B2B processing costs are higher than they should be. If you’ve reviewed your merchant statement and felt confused by line items you didn’t agree to, or if your effective processing rate seems to creep upward every quarter, this is written for you.

We focus specifically on the hidden fees that inflate B2B card processing costs and, more importantly, on how eliminating those fees works in tandem with faster payment settlement to create a compounding cash flow advantage. By the end, you’ll understand how to audit your current processing setup, qualify more transactions at lower interchange tiers, and connect those savings to settlement speed so every dollar you recover gets reinvested sooner.

This guide does not cover enterprise-scale treasury management, near-zero fee solutions that aren’t realistic for mid-market operators, or a full platform migration. It’s about working smarter within the infrastructure you already have.

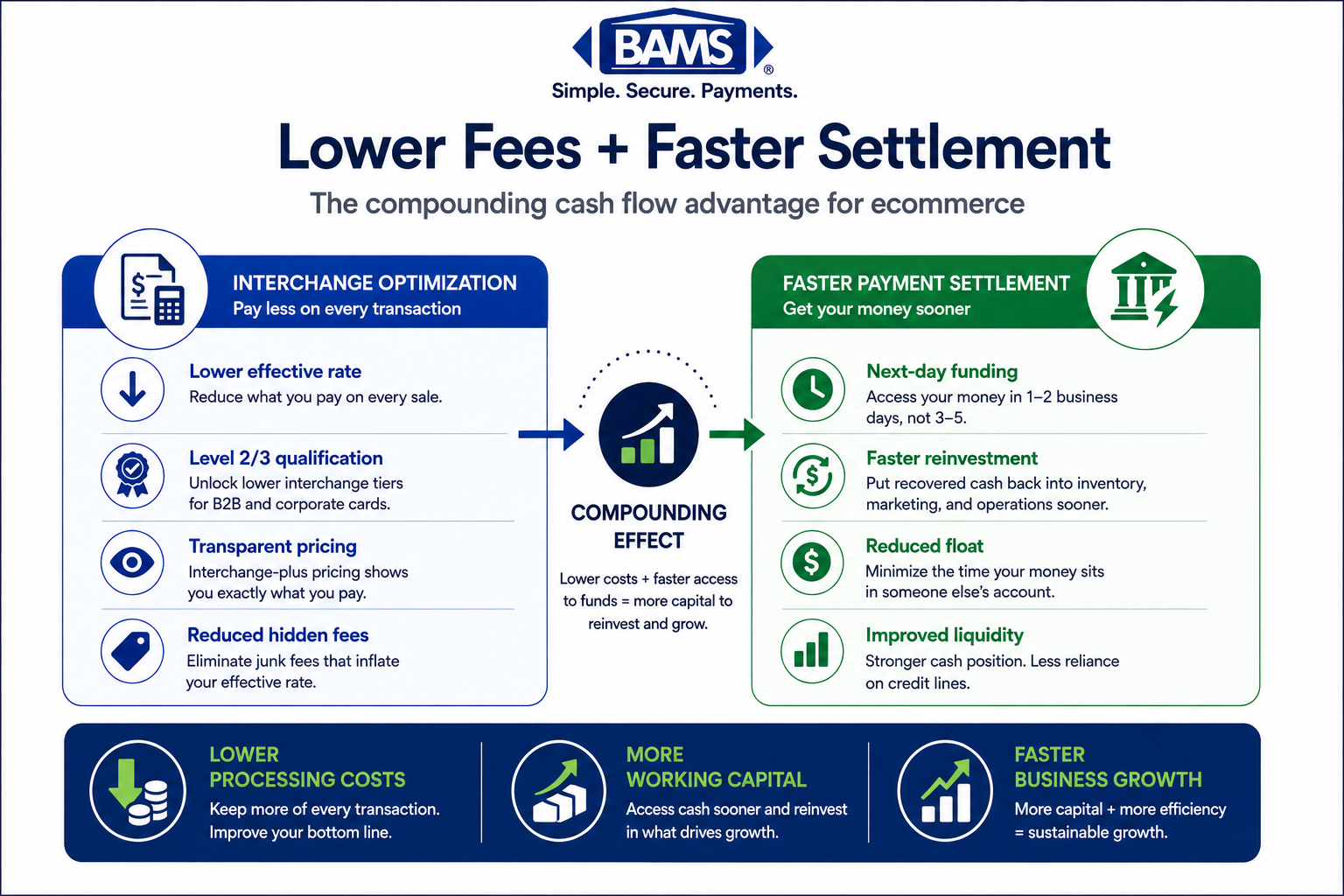

Why Transaction Cost Savings and Settlement Speed Matter Together

Lower interchange costs and faster settlement cycles work together to create stronger cash flow and more reinvestable capital for eCommerce businesses.

Most content about reducing processing costs treats interchange optimization and funding speed as separate topics. One article tells you to negotiate your markup. Another tells you to find a processor with next-day funding. Neither explains what happens when you combine both, and that’s where mid-market eCommerce businesses leave the most money on the table.

Here’s the math that makes this concrete. If you process $500,000 per month in B2B card transactions and your effective rate drops from 3.1% to 2.4%, you save $3,500 monthly. That’s meaningful. But if those savings also land in your bank account one to two days sooner than before, you unlock working capital that can cover inventory purchases, fund ad spend, or reduce reliance on credit lines. Over twelve months, the compounding effect of reinvesting recovered funds earlier can exceed the fee savings themselves.

The industry is moving in this direction. Businesses that treat cost reduction and settlement speed as a single system are building a structural advantage. Those that don’t are subsidizing competitors who do.

Core Concepts: The Language of Hidden B2B Processing Costs

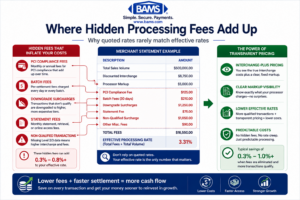

Effective Processing Rate

Your effective processing rate is the total amount you pay in processing fees divided by your total processing volume. It’s the single most honest number on your merchant statement, and most processors don’t highlight it. If you’re paying $7,500 in total fees on $250,000 in volume, your effective rate is 3.0%. This number matters more than any quoted rate because it includes every hidden fee, not just the interchange and markup your processor advertises. Card payment costs include interchange fees, network assessments, and processor markups, which together determine the true effective rate merchants ultimately pay as outlined by the Federal Reserve.

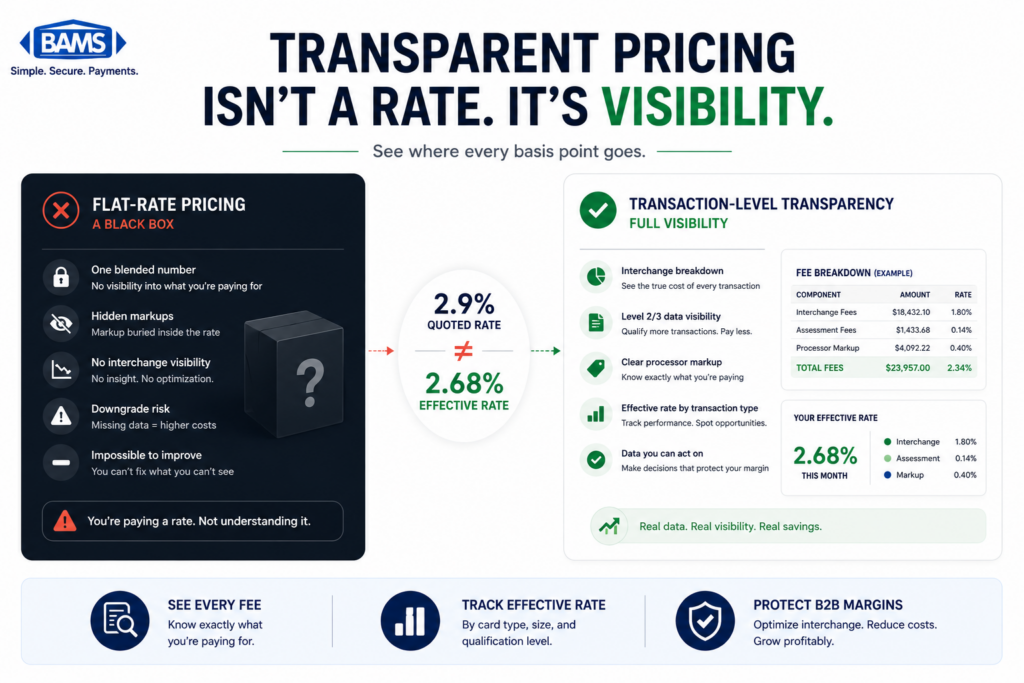

Interchange-Plus Pricing vs. Bundled Pricing

Interchange-plus pricing separates the interchange fee (set by card networks) from your processor’s markup. You see exactly what Visa or Mastercard charges and exactly what your processor adds. Bundled (or tiered) pricing lumps everything together into “qualified,” “mid-qualified,” and “non-qualified” buckets, making it nearly impossible to identify where your money goes. For B2B transactions, bundled pricing almost always costs more because high-ticket and corporate card transactions get routed to the most expensive tier. A detailed breakdown of this structure is available in this guide to credit card processing fees for eCommerce.

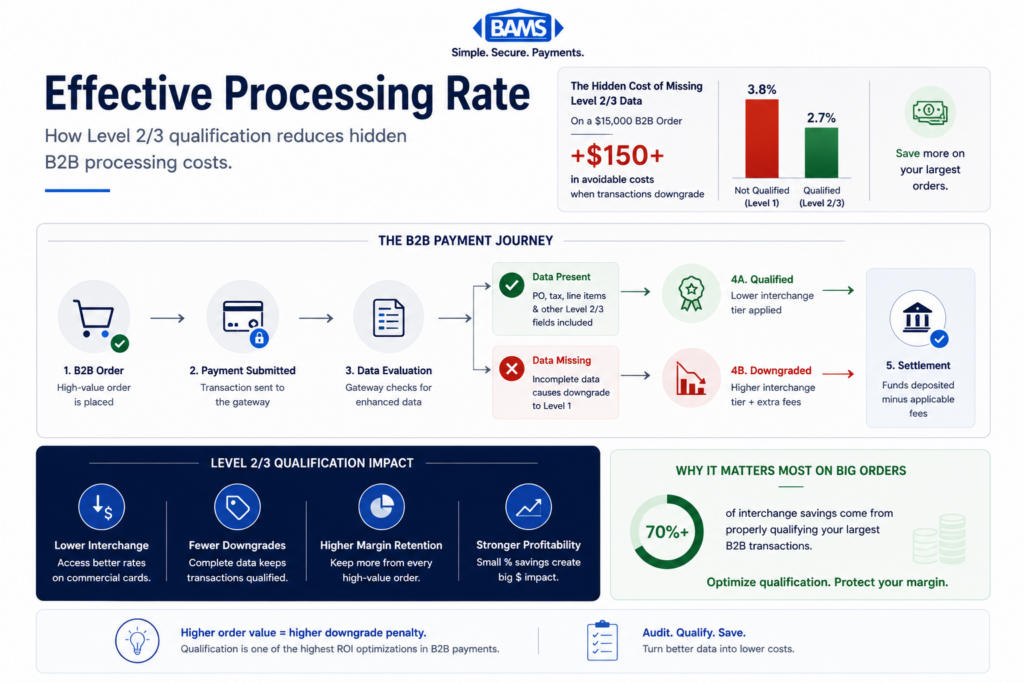

Level 2 and Level 3 Data Qualification

Card networks offer lower interchange rates on B2B transactions when you submit additional data fields with each transaction. Level 2 data includes tax amount, customer code, and merchant postal code. Level 3 adds line-item detail: product descriptions, quantities, unit costs, and commodity codes. When your gateway or processor submits this data correctly, your transactions qualify for significantly lower interchange categories. When they don’t, you pay the standard (higher) rate, and most processors never tell you.

Settlement Speed as a Financial Lever

Settlement speed is how quickly processed funds reach your bank account. Traditional processors batch-settle in two to three business days. Next-day funding closes that gap. The difference isn’t just convenience; it’s a reduction in your cash conversion cycle that directly affects how much working capital you need to maintain operations. Settlement timing depends on how transactions move between gateways, processors, card networks, and issuing banks, with batch schedules and processing infrastructure directly affecting funding speed as outlined by Visa.

The Framework: Treating Cost Reduction and Cash Flow as One System

Most eCommerce operators approach processing costs through a single lens: find a cheaper rate. This guide uses a different framework built on three interconnected phases.

Phase 1: Expose — Identify every fee you’re currently paying, including the ones your processor buries in statement footnotes. Calculate your true effective processing rate.

Phase 2: Optimize — Reduce your interchange costs through data qualification, pricing model corrections, and fee elimination. This is where Level 2/3 optimization and hidden fee removal happen.

Phase 3: Accelerate — Connect your cost savings to faster settlement so recovered dollars re-enter your business sooner. Measure the combined impact, not each piece in isolation.

These phases are sequential but also cyclical. As your volume grows or your product mix changes, you return to Phase 1 and re-audit. The businesses that treat this as an ongoing system, rather than a one-time negotiation, consistently maintain lower costs.

Step-by-Step: Eliminating Hidden Fees and Connecting Savings to Cash Flow

Step 1: Calculate Your True Effective Processing Rate

Objective: Establish an honest baseline of what you’re actually paying, not what your processor says you’re paying.

Pull your last three monthly merchant statements. For each month, divide total fees (every line item, including PCI compliance fees, batch fees, statement fees, and any charges labeled as “miscellaneous” or “regulatory”) by total processing volume. The result is your effective rate. If your processor quotes you 2.3% but your effective rate is 2.9% or higher, the gap represents hidden costs.

For a deeper walkthrough on what to look for, this breakdown of why your rate is higher than you think covers the most commonly overlooked fee layers, including card-not-present premiums and assessment fees that processors rarely explain.

Anti-patterns: Don’t rely on your processor’s summary dashboard. These often exclude ancillary fees. Don’t average a single month; seasonal volume shifts can distort your baseline. Don’t confuse your quoted interchange-plus rate with your effective rate.

Success indicators: You have a three-month average effective rate calculated to two decimal places. You can identify at least three fee categories beyond interchange and markup. You know the dollar gap between your quoted rate and your actual rate. Merchants using transparent interchange plus pricing gain visibility into interchange costs and processor markup separately, making it easier to identify unnecessary fee inflation.

Step 2: Audit for Hidden and Junk Fees

Objective: Identify every fee that doesn’t directly correspond to interchange, assessments, or a clearly defined processor markup.

A breakdown of hidden processing fees that increase your effective rate and reduce available working capital.

Common hidden fees in merchant services include PCI non-compliance fees (charged when you haven’t completed a self-assessment questionnaire, sometimes even when you have), monthly minimum fees, batch processing fees, annual fees, early termination fees embedded in auto-renewal clauses, and “rate adjustment” surcharges that appear after your initial contract period.

Create a spreadsheet with three columns: fee name, monthly amount, and whether you agreed to it in your original contract. Highlight anything you can’t trace to a specific contractual term. For B2B eCommerce, pay special attention to “downgrade surcharges,” which are fees charged when a transaction doesn’t qualify at the lowest interchange tier. These are often the largest hidden cost and the most fixable.

Anti-patterns: Don’t assume a fee is legitimate just because it appears on every statement. Some processors add fees incrementally, counting on the fact that you won’t notice a $15 charge that wasn’t there six months ago. Don’t skip the contract review; some fees are technically disclosed but buried in addenda.

Success indicators: You have a complete inventory of every non-interchange fee. You can categorize each as “agreed,” “unclear,” or “not in contract.” You’ve quantified the total monthly cost of fees outside interchange and processor markup.

Step 3: Verify Your Level 2/3 Data Qualification

Objective: Determine whether your B2B and high-ticket transactions are actually qualifying at the lowest available interchange tiers.

This is the step most mid-market eCommerce businesses skip entirely, and it’s often the most valuable. Card networks like Visa and Mastercard offer reduced interchange rates on B2B transactions when Level 2 or Level 3 data is submitted. The savings can range from 0.3% to over 1.0% per transaction, which on a $500,000 monthly B2B volume translates to $1,500 to $5,000 in monthly savings.

The problem: many processors claim to support Level 2/3 processing but don’t actually pass the required data fields. To verify, request a transaction-level interchange qualification report from your processor. Look for transactions categorized as “EIRF” (Electronic Interchange Reimbursement Fee) or “Standard,” which are Visa’s designations for transactions that failed to qualify at lower tiers. If more than 10-15% of your B2B transactions fall into these categories, your data isn’t being submitted correctly.

Anti-patterns: Don’t take your processor’s word that “Level 3 is enabled.” Ask for proof in the form of qualification reports. Don’t assume your eCommerce platform handles this automatically; most platforms (including Shopify) don’t pass Level 3 data without additional configuration or middleware.

Success indicators: You have a transaction-level qualification report. You know the percentage of transactions qualifying at Level 2 or Level 3. You can estimate the dollar impact of upgrading unqualified transactions.

Step 4: Switch to Interchange-Plus Pricing (If You Haven’t)

Objective: Ensure your pricing model gives you full visibility into interchange costs and processor markup, separately.

If you’re still on tiered or bundled pricing, this single change can reduce your effective processing rate by 0.3% to 0.8% without any other modifications. Tiered pricing is designed to obscure costs. It routes transactions into qualification buckets that benefit the processor, not you. Interchange-plus pricing removes this opacity.

When negotiating the switch, focus on the processor’s markup (the “plus” in interchange-plus), not the interchange rate itself. Interchange is set by card networks and is non-negotiable. Your processor’s margin on top of interchange is entirely negotiable. For mid-market eCommerce businesses processing $200,000 to $1 million monthly, a competitive markup ranges from 0.10% to 0.25% plus $0.05 to $0.10 per transaction.

Anti-patterns: Don’t accept a “blended” rate that your processor calls interchange-plus but actually bundles assessments into the quoted rate. Don’t negotiate based on volume you hope to reach; negotiate based on your current three-month average. Don’t sign contracts longer than one year without a rate review clause.

Success indicators: Your statement clearly separates interchange, assessments, and processor markup on every transaction. Your effective rate has decreased measurably within the first full billing cycle. You can verify any markup increase against your contract terms.

Step 5: Connect Cost Savings to Faster Payment Settlement

Objective: Ensure the money you save on processing fees reaches your operating account as quickly as possible, creating a compounding cash flow advantage.

This is the step that transforms transaction cost savings from a line-item improvement into a growth lever. Around 48% of businesses now use faster payment methods specifically to reduce costs, but the real advantage is what happens when lower fees and faster settlement work together.

Consider a concrete scenario. You reduce your effective rate from 3.0% to 2.4% on $400,000 in monthly volume, saving $2,400 per month. If your previous processor settled in three business days and your new arrangement settles next-day, you gain access to roughly two days of float on your entire processing volume. On $400,000 monthly (approximately $13,300 daily), that’s $26,600 in working capital available sooner each month. Combined with the $2,400 in fee savings, your total monthly cash flow improvement approaches $29,000.

Providers like BAMS offer next-day funding alongside interchange-plus pricing, which means your savings aren’t sitting in a processor’s holding account for two to three extra days. That combination is what turns a cost-reduction exercise into a reinvestment engine.

Anti-patterns: Don’t evaluate settlement speed in isolation from cost. A processor offering next-day funding with a higher effective rate may cost you more overall. Don’t overlook weekend and holiday settlement gaps; ask your processor exactly how many calendar days your funds are typically held.

Success indicators: You know your average settlement time in both business days and calendar days. You can calculate the working capital freed by faster settlement. You’ve modeled the combined impact of lower fees plus faster funding on a 12-month basis.

Step 6: Automate Monitoring and Schedule Recurring Audits

Objective: Prevent fee creep and qualification drift from eroding your gains over time.

Processing costs are not a set-it-and-forget-it problem. Card networks update interchange tables twice a year (April and October). Processors can adjust markups with notice periods as short as 30 days. Your own product mix and average ticket size shift seasonally, which changes your interchange qualification profile. Modern payment infrastructure improves transaction visibility and operational control, helping eCommerce businesses identify qualification failures, settlement delays, and processing inefficiencies earlier according to Modern Treasury.

Set a calendar reminder to recalculate your effective rate quarterly. Compare it against your baseline from Step 1. If it rises by more than 0.1% without a corresponding change in your business, investigate. Request updated qualification reports every six months to ensure your Level 2/3 data is still passing correctly. If you’ve added new product lines, new payment methods, or changed eCommerce platforms, re-verify data field mapping immediately.

Anti-patterns: Don’t assume your initial optimization is permanent. Don’t rely solely on your processor to notify you of rate changes; read every statement. Don’t treat reconciliation as a finance-only task; your eCommerce operations team needs visibility into qualification rates and settlement timing.

Success indicators: You have a quarterly review process documented and assigned. Your effective rate has remained stable or decreased over two consecutive quarters. You can identify the cause of any rate increase within one billing cycle.

Practical Examples: Before and After

Scenario A: The Bundled Pricing Trap

A mid-market eCommerce business processing $600,000 monthly in mixed B2C and B2B orders operates on tiered pricing. Their processor quotes a “qualified rate” of 1.69%, but their effective rate is 3.15%. The gap comes from non-qualified surcharges on corporate cards (which make up 40% of their volume), a $99 monthly PCI fee, a $25 statement fee, and batch fees totaling $45 per month.

After switching to interchange-plus pricing and enabling Level 2 data submission, their effective rate drops to 2.45%. The monthly savings: $4,200. After also moving to a processor with next-day funding, they gain access to approximately $40,000 in working capital sooner each month, which they redirect toward inventory purchases that previously required a revolving credit line at 8.5% APR. The annual impact: over $50,000 in direct savings plus $3,400 in avoided interest.

Scenario B: Level 3 Data That Wasn’t Actually Passing

An eCommerce wholesaler processes $350,000 monthly, almost entirely B2B. Their processor confirmed “Level 3 support” during onboarding. After requesting a qualification report (Step 3), the wholesaler discovers that 68% of transactions are qualifying at Standard interchange, the highest tier, because their gateway wasn’t passing line-item data correctly. The configuration fix takes two weeks. The result: a 0.7% reduction in effective rate, saving $2,450 per month with zero change in pricing model or processor.

Common Mistakes and Pitfalls

Focusing only on the quoted rate. Your processor’s quoted rate is a marketing number. Your effective rate is the real number. Every decision should be benchmarked against effective rate, not the rate on your contract’s first page. Processors offering guaranteed next day funding allow recovered processing savings to re-enter the business faster, reducing cash flow friction across operations.

Ignoring Level 2/3 qualification. This is the single largest source of unnecessary interchange cost for B2B eCommerce. If you process corporate cards or purchasing cards and haven’t verified your qualification reports, you’re almost certainly overpaying.

Treating settlement speed as a convenience feature. Faster settlement isn’t about getting paid sooner for its own sake. It’s about reducing your cash conversion cycle, which directly affects how much external capital you need. The businesses adapting now are building a durable advantage.

Auditing once and assuming the problem is solved. Fee creep is real. Interchange tables change. Processor markups adjust. Your business evolves. Quarterly reviews are the minimum cadence for maintaining your gains.

What to Do Next

Start with Step 1. Pull your last three merchant statements and calculate your effective processing rate. That single number will tell you whether your current setup is working or quietly draining margin. If the gap between your quoted rate and your effective rate is more than 0.3%, you have recoverable savings waiting.

From there, work through the steps in order. Each one builds on the previous. You don’t need to overhaul your entire payment stack in a week. Even completing Steps 1 through 3 will give you the information you need to have a more informed conversation with your current processor or evaluate alternatives.

Revisit this guide quarterly as a reference, not a one-time checklist. The businesses that consistently maintain low processing costs are the ones that treat payment optimization as an ongoing operational discipline rather than a one-time project.

Frequently Asked Questions

What is interchange-plus pricing and how does it work?

Interchange-plus pricing separates the two main components of your processing cost: the interchange fee (set by card networks like Visa and Mastercard) and your processor’s markup. You see both numbers on your statement, which makes it easy to verify what you’re paying and why. This transparency is especially valuable for B2B transactions, where interchange rates vary significantly based on card type and data qualification. It’s generally the most cost-effective model for mid-market eCommerce businesses.

Why should businesses consider Level 2/3 optimization for B2B transactions?

Card networks offer lower interchange rates when you submit additional transaction data, such as tax amounts, customer codes, and line-item details. Level 2 data can reduce interchange by 0.3% to 0.5% per transaction, and Level 3 can push savings beyond 1.0% on qualifying transactions. For businesses processing significant B2B volume on corporate or purchasing cards, this optimization often represents the largest single opportunity to reduce costs without changing processors or pricing models.

How can companies effectively reduce their merchant service charges?

Start by calculating your true effective processing rate (total fees divided by total volume). Then audit for hidden fees like PCI non-compliance charges, batch fees, and downgrade surcharges. Ensure you’re on interchange-plus pricing rather than tiered or bundled models. Verify that your B2B transactions are qualifying at the lowest interchange tiers through Level 2/3 data submission. Finally, connect those savings to faster settlement so recovered funds re-enter your business sooner. For more detail on hidden fee layers, see this guide to true processing costs.

When is the best time to negotiate processing fees with your merchant services provider?

The strongest negotiating position comes after you’ve completed your own audit. When you can show your processor your effective rate, your qualification report, and the specific fees you’re questioning, the conversation shifts from vague complaints to data-backed requests. Contract renewal periods are also natural negotiation points. Avoid negotiating based on projected future volume; use your actual three-month average as leverage.

What are the common hidden fees in merchant services that businesses should watch out for?

The most common include PCI non-compliance fees (often $19.95 to $99 monthly), statement fees, batch processing fees, annual or account maintenance fees, early termination fees, and “rate adjustment” surcharges that appear after introductory periods expire. For B2B eCommerce, downgrade surcharges on transactions that fail to qualify at lower interchange tiers are frequently the most expensive hidden cost. These can add 0.5% to 1.5% to individual transactions without appearing as a separate, clearly labeled line item.

Which payment processing model is more cost-effective for high-volume transactions?

For most mid-market eCommerce businesses processing $200,000 or more monthly, interchange-plus pricing is the most cost-effective and transparent model. It allows you to benefit directly from lower interchange tiers (especially with Level 2/3 data qualification) and makes it easy to verify your processor’s markup. Flat-rate pricing (like Stripe’s or PayPal’s standard rates) becomes increasingly expensive as volume grows because you pay the same percentage regardless of actual interchange costs. For American Express specifically, programs like OptBlue can significantly reduce costs compared to standard Amex processing.