Payment Analytics: What Your Statement Isn’t Showing You

Why the gap between what you paid and what you should have paid is where margin quietly disappears

Learn why processing statements fail as diagnostic tools and how transaction-level payment analytics reveals the hidden margin loss that summary reporting was never designed to catch.

TL;DR

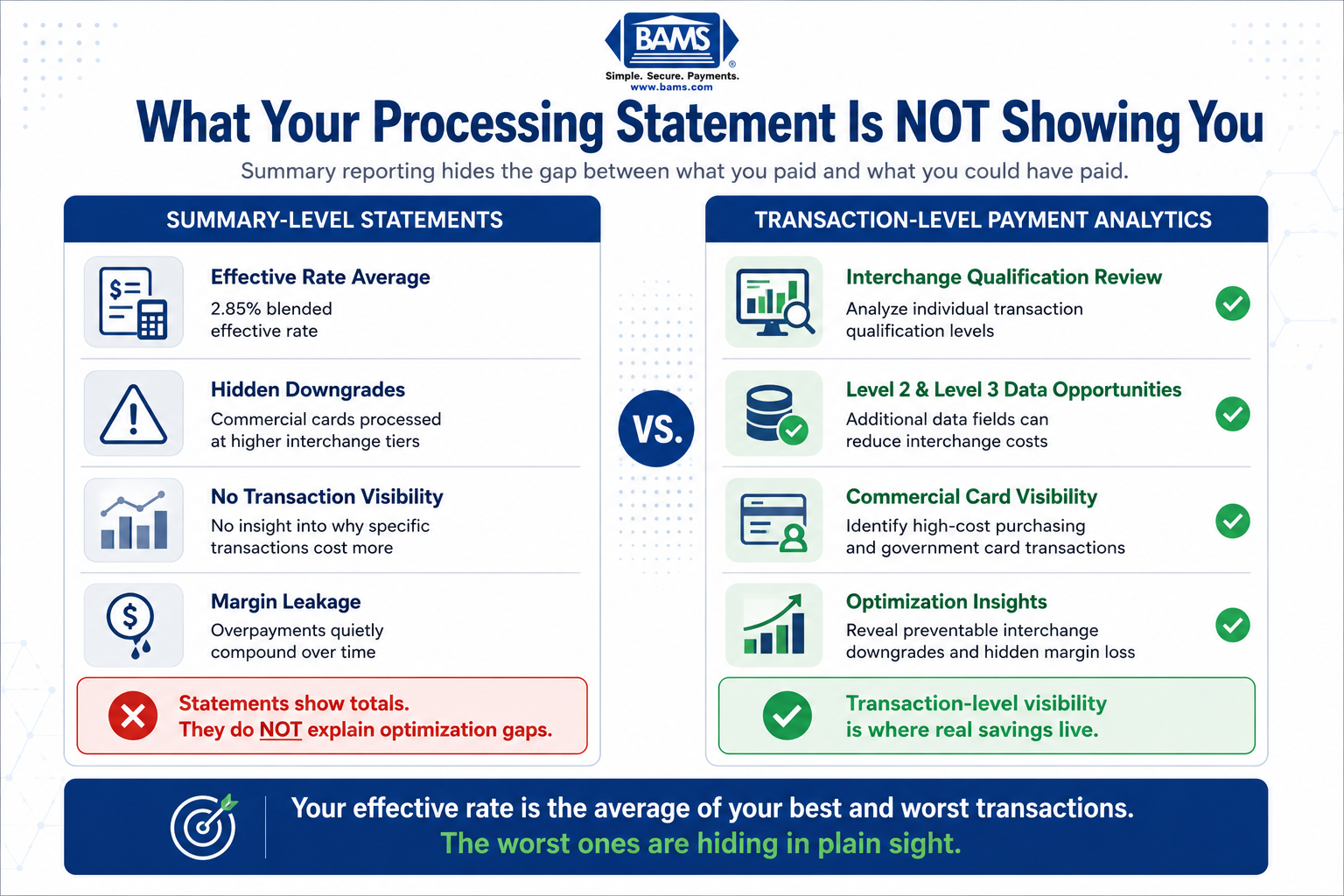

- Your statement shows what you paid, not what you should have paid – Effective rate averages hide costly interchange downgrades on individual transactions, especially commercial card orders.

- Statement opacity benefits processors, not merchants – Summary-level reporting was never designed to help you optimize. Transaction-level evaluation is where real savings live.

- Level 3 data isn’t just for enterprise B2B – If any of your eCommerce customers pay with corporate or purchasing cards, you’re likely overpaying on those transactions without knowing it.

- Your effective rate is not your actual rate – It’s the average of your best and worst qualifying transactions, and the worst ones are hiding in plain sight.

The Document Everyone Trusts but Nobody Reads Closely

Every month, your processing statement lands. You glance at the total, compare it to last month, maybe wince, and move on. That number feels like the truth. It isn’t.

Your processing statement shows you what you paid. It doesn’t show you what you should have paid. And that gap, the space between the actual charge and the optimal charge, is where your margin quietly disappears. Real payment analytics starts with understanding that distinction.

For eCommerce managers juggling deposit timing, chargeback rates, and platform fees, the statement becomes a summary of damage already done. Not a diagnostic tool. Not a roadmap. Just a receipt.

Why We Treat Statements Like Financial Truth

Processing statements became the default accountability mechanism because they were the only thing processors gave us. They list transactions, fees, and totals. They look thorough. And for a long time, that was enough.

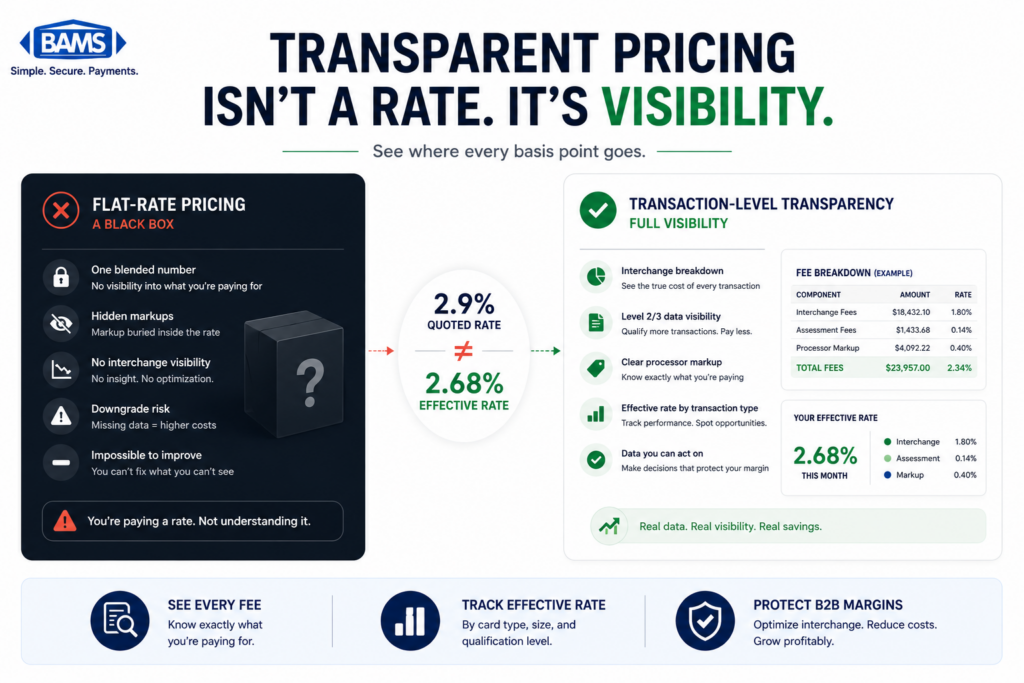

The logic made sense: if you can see what you’re paying, you can manage it. Processors reinforced this by offering “transparent” pricing models (interchange-plus, flat rate, tiered) and pointing to the statement as proof of their honesty. The industry trained merchants to audit at the summary level, comparing effective rates month over month.

But summary-level reporting was designed for a simpler era. As transaction complexity increases across eCommerce operations, Visa’s small business payment resources continue to emphasize the importance of visibility, payment data accuracy, and modern payment infrastructure for growing merchants.

The Real Problem Isn’t Complexity. It’s Convenient Opacity.

Here’s what we actually believe: statement opacity isn’t a complexity problem merchants need to solve. It’s a transparency failure processors have no incentive to fix.

Processing statements only show what you paid. Transaction-level payment analytics reveals what you should have paid.

Your processor benefits when you can’t see the difference between what you paid and what was possible. That’s not a conspiracy. It’s just business model mechanics. And it’s the reason transaction-level evaluation matters more than any statement summary ever will.

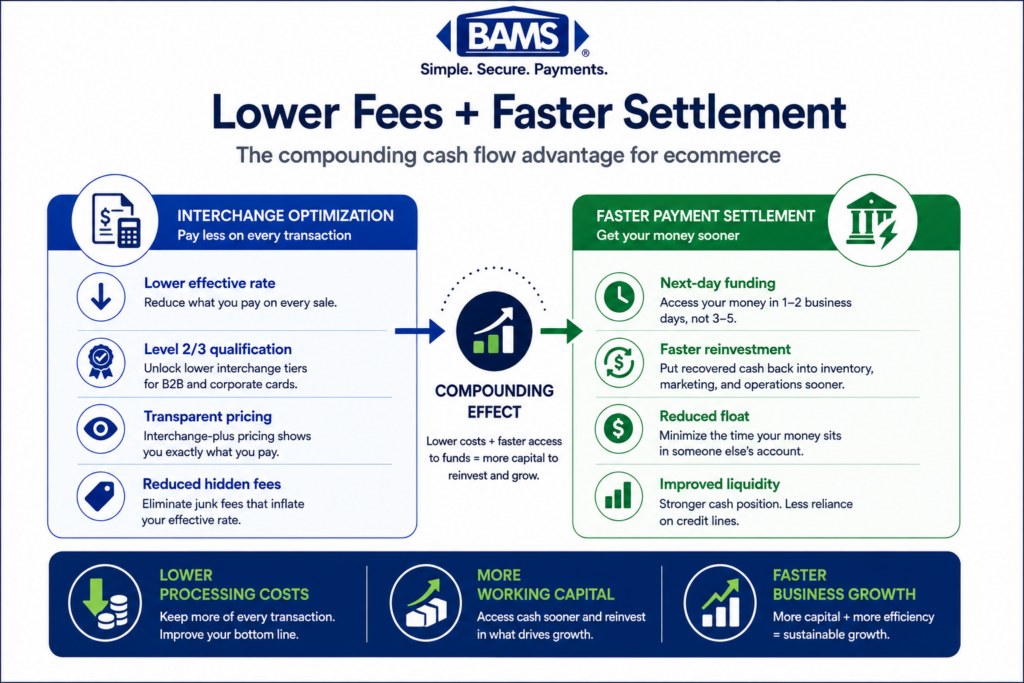

Where Credit Card Optimization Actually Lives

Let’s make this concrete. Say your eCommerce store processes 8,000 transactions a month. A healthy mix of consumer debit, consumer credit, and a slice of commercial and purchasing cards from business buyers. Your statement shows an effective rate of 2.85%. Looks normal. Maybe even competitive.

But buried in that average is a story the statement won’t tell you.

Most merchants focus on statements. Real optimization happens at the transaction level.

Some of those commercial card transactions qualified at the highest interchange tier because your gateway only passed Level 1 data (card number, amount, date). Had your system passed Level 2 data (tax amount, merchant postal code) or Level 3 data (line-item detail, invoice numbers, product codes), those same transactions could have qualified at significantly lower interchange rates. The card networks created interchange categories specifically to reward richer data, but most eCommerce merchants never know they’re eligible.

This isn’t a B2B-only problem. If you sell online and any portion of your customers pay with corporate purchasing cards, government cards, or business credit cards, you’re likely overpaying on those transactions without realizing it. Your statement won’t flag them. It just averages them into the blend.

Modern Treasury payment operations resources continue to emphasize how transaction-level visibility and reconciliation workflows improve operational decision-making. That advice scales down perfectly. You don’t need an enterprise treasury team. You need someone looking at your transactions individually, not in aggregate.

This is where working with a partner like BAMS changes the math. Their approach to merchant services includes transaction-level evaluation that identifies where you’re overpaying on interchange, which card types are costing you the most, and whether your gateway is passing enough data to qualify for lower rates. It’s the kind of analysis your statement was never built to provide.

Businesses are waking up to the fact that payment data, analyzed at the right depth, is a profit lever. Not just a cost center.

What You’re Actually Risking by Trusting the Summary

If this thesis is right, then every month you rely solely on your processing statement, you’re making financial decisions with incomplete information. You’re benchmarking against an effective rate that hides the variance between your best-qualifying and worst-qualifying transactions.

For an eCommerce business processing $500,000 a month, even a 15-basis-point gap between actual and optimal interchange on commercial card volume can mean thousands lost annually. That’s not a rounding error, that’s a marketing budget. That’s inventory and that’s the difference between hiring and waiting.

And the cost compounds. Because if you don’t know which transactions are downgrading, you can’t fix the data fields causing the downgrades. You can’t have the right conversation with your gateway provider. You can’t hold your processor accountable for something neither of you is measuring.

A Better Way to Think About Your Processing Costs

Stop thinking of your processing statement as a report card. Start thinking of it as a table of contents.

It tells you the chapters exist. It doesn’t tell you what’s in them. Real credit card optimization means reading the chapters: examining each transaction’s interchange qualification, understanding why specific charges landed where they did, and identifying the data gaps that cost you money.

The mental model shift is this: your effective rate is not your actual rate. It’s the average of your best rates and your worst rates, and the worst ones are hiding in plain sight. That reframe alone changes how you evaluate processors, negotiate contracts, and prioritize gateway configurations.

The Statement Is the Starting Line, Not the Finish

We’re not saying throw your statement away. We’re saying stop letting it be the final word on what your payments cost. The merchants who are reducing processing costs today aren’t the ones with the best negotiated rates. They’re the ones with the deepest visibility into what’s happening at the transaction level.

Your processor should be showing you that picture. If they’re not, the question isn’t whether you’re overpaying. It’s by how much.

Frequently Asked Questions

What is Level 3 data in merchant services?

Level 3 data refers to detailed, invoice-quality transaction information (line items, product codes, tax amounts) passed during payment processing. When submitted with commercial or purchasing card transactions, it can qualify those transactions for lower interchange rates from the card networks.

How does transaction-level evaluation differ from reading my processing statement?

Your processing statement shows totals and averages across all transactions. Transaction-level evaluation examines each individual charge to determine whether it qualified at the lowest possible interchange rate, revealing specific opportunities your statement’s summary obscures.

Which types of transactions are eligible for Level 3 interchange rates?

Commercial cards, corporate purchasing cards, and government cards are the primary transaction types eligible for Level 3 interchange savings. Many eCommerce merchants process these without realizing it, because their statements don’t distinguish them from consumer card transactions.

Sources