6 Places Slow Deposits Drain eCommerce Margins

A diagnostic framework for the hidden liquidity losses most operators never trace back to settlement timing

Discover six specific cost categories where payment deposit delays silently erode eCommerce profitability. Learn how to diagnose compounding cash flow management problems across inventory, financing, and competitive response before they drain your margins.

TL;DR

- Slow deposits create six hidden costs – Missed restock windows, invisible financing charges, forfeited supplier discounts, capped ad campaigns, inflated payroll reserves, and delayed competitive responses all trace back to settlement timing.

- The root cause hides behind symptoms – These costs never appear as “processing expenses” in your books. They show up as stockouts, interest payments, and missed revenue, which is why most operators only catch one or two.

- Next-day funding changes the math across all six categories – Faster deposits don’t just improve cash flow. They reduce borrowing, unlock supplier discounts, and let you scale winning campaigns without external capital.

- Start with inventory and financing costs – These two categories compound daily and hit gross margin directly. Audit your actual deposit arrival times over 30 days and compare the real cost against next-day alternatives.

- Treat deposit speed as a controllable variable – Build a rolling 13-week cash flow forecast that accounts for settlement timing. When you can predict when cash arrives, you shift from building defensive buffers to deploying capital proactively.

The Hidden Cost of Getting Paid Tomorrow Instead of Today

Ecommerce operators have a paradox most traditional retailers never face. Revenue flows in daily, sometimes hourly, yet the cash from those sales can sit in limbo for two to five business days before it hits your bank account. The ACH Network remains one of the primary mechanisms used to move funds between financial institutions, making settlement timing an important factor in how quickly businesses gain access to processed revenue.

That gap between earning and accessing creates a quiet, compounding drag on cash flow management that most operators underestimate.

The standard advice (tighten receivables, invoice faster, cut expenses) assumes a B2B billing cycle. It doesn’t account for the specific mechanics of payment processing settlement windows, where your money exists but isn’t yours yet. According to the Federal Reserve’s 2025 Small Business Credit Survey, cash flow management and operating expenses remain among the most significant financial challenges facing many small businesses.

This isn’t a general cash flow primer. It’s a diagnostic framework for the six specific places where slow deposit timing silently erodes eCommerce margins, and how to forecast around them once you understand the pattern.

Who This Is For and What It Covers

This guide is built for eCommerce managers at established online businesses (roughly 10 to 50 employees) who process consistent daily transaction volume and feel the friction of delayed deposits even when sales are strong.

The U.S. Small Business Administration identifies cash flow planning as a critical component of business stability and long-term growth, particularly for businesses managing inventory, payroll, and supplier obligations. If you’ve ever had the cash to restock but couldn’t access it in time, this is your playbook.

We’re not covering basic budgeting, invoice optimization for service businesses, or how to set up your first accounting system. We’re focused on the intersection of deposit timing, operational agility, and the six cost categories that surface when settlement windows stretch even one day longer than they should.

How We Selected These Six Margin Drains

Each item on this list meets three criteria. First, it represents a cost that is directly caused or amplified by delayed access to processed revenue. Second, it is commonly missed in standard cash flow advice because it requires understanding payment settlement mechanics. Third, it compounds over time rather than appearing as a single event, making it easy to normalize until the cumulative damage is significant.

6 Places Slow Deposits Silently Drain Ecommerce Margins

The cost of slow deposits rarely appears as a processing fee.

1. Missed Inventory Restock Windows

Why it matters: Suppliers often offer the narrowest restock windows on your highest-velocity SKUs. When your deposit lands on Thursday instead of Tuesday, you miss the cutoff. The stockout doesn’t show up as a “deposit timing problem” in your P&L. It shows up as lost sales, and you attribute it to demand forecasting.

What it looks like today: eCommerce operators running lean inventory models (which most should) depend on frequent, small reorders timed to cash availability. A two-to-three day settlement delay means you’re financing restock gaps with credit lines or simply going out of stock. Faster access to working capital often allows businesses to place replenishment orders sooner and reduce the likelihood of inventory shortages.

How to apply it: Map your top 10 SKUs by velocity. For each, document the supplier’s order cutoff and your average deposit arrival day. Identify every instance where a one-day faster deposit would have let you place an order a cycle earlier. This gives you a concrete dollar figure for the cost of your current settlement window.

2. Invisible Financing Costs on Working Capital

Why it matters: When deposits arrive slowly, you bridge the gap with credit cards, lines of credit, or short-term loans. These costs get categorized as “financing expenses” rather than what they actually are: a surcharge on slow payment processing. Most operators never connect the two line items.

What it looks like today: Instant payout services charge roughly 1% per transaction for urgent fund access. Credit card float costs 1.5% to 2.5% monthly. Lines of credit carry their own interest. All of these are workarounds for a settlement timing problem, not genuine capital needs.

How to apply it: Audit the last 90 days. Total every dollar borrowed or floated specifically because processed revenue hadn’t arrived yet. Compare that cost against what you’d pay with a processor that offers next-day funding. The delta is your true cost of slow deposits, and it’s usually larger than the processing fee difference you negotiated last quarter.

3. Supplier Discount Forfeitures

Why it matters: Many suppliers offer early payment discounts (commonly 2% for paying within 10 days). When your cash is trapped in a three-to-five day settlement cycle, you burn through half that window before you even have the funds. The discount expires, and you pay full price on goods you’ve already sold.

What it looks like today: Industry guidance recommends leveraging 2/10 net 30 terms as a practical cash flow lever. But the math only works if you actually have the cash within those 10 days. For eCommerce operators with multi-day settlement holds, this discount is theoretical, not operational.

How to apply it: List every supplier that offers early payment terms. Calculate the annualized value of those discounts across your total purchasing volume. Then check how many you’ve actually captured in the last six months. The gap between available and captured discounts is a direct margin leak tied to deposit speed.

4. Ad Spend Timing Gaps During Peak Demand

Why it matters: Paid acquisition doesn’t wait for your deposits. When a product goes viral or a campaign outperforms, you need to scale ad spend immediately. A two-day delay in accessing yesterday’s revenue means you’re either capping winning campaigns or funding them with debt at the exact moment your return on ad spend is highest.

What it looks like today: eCommerce ad accounts on Meta and Google require daily budget availability. Campaign algorithms optimize around consistent spend. When you throttle budget because cash hasn’t landed, the algorithm resets its learning phase, costing you both the immediate sales and the data advantage you’d built.

How to apply it: Track your top five campaign days over the past quarter. For each, note whether you had unrestricted budget access or had to cap spend due to cash availability. Estimate the revenue you left on the table. Even conservative estimates usually reveal that faster deposits would have funded the scale-up without external capital.

5. Payroll and Contractor Timing Stress

Why it matters: Payroll is non-negotiable and fixed-date. When deposit timing is unpredictable, you maintain larger cash reserves than necessary just to cover the gap between when you earn and when you must pay your team. That idle cash buffer is capital that could be deployed elsewhere.

What it looks like today: Industry guidance suggests keeping six months of expenses as a safety net. But a significant portion of that buffer exists only because deposit timing is unreliable. Operators with predictable next-day funding can run leaner reserves and redeploy the difference into growth.

How to apply it: Calculate your current cash buffer specifically allocated to cover payroll timing uncertainty. If you could predict deposits arriving within one business day consistently, how much of that buffer could you reduce? That freed capital has a direct opportunity cost you can quantify against your average return on invested capital.

6. Competitive Response Lag

Why it matters: eCommerce moves fast. A competitor drops prices, a trending product emerges, or a marketplace algorithm shifts. Your ability to respond (new inventory, adjusted pricing, rapid campaign launch) depends on having cash available now, not cash that’s arriving in three days.

What it looks like today: Operators with slow settlement cycles make strategic decisions based on projected cash rather than actual cash. This introduces conservatism into every competitive response. You order less, bid lower, and react slower. The cost doesn’t appear on any report because it’s the revenue you never captured.

How to apply it: Review the last quarter for moments when you wanted to act quickly but couldn’t because funds were in transit. Price drops you delayed, inventory you didn’t order, campaigns you didn’t launch. Assign a conservative revenue estimate to each. This is your competitive response tax, paid entirely because of deposit timing. Processors like BAMS, which offer next-day funding with a 9 PM EST cutoff, exist specifically to eliminate this lag for small-to-midsize eCommerce operations.

The Pattern Behind All Six: Improve Liquidity to Improve Everything Else

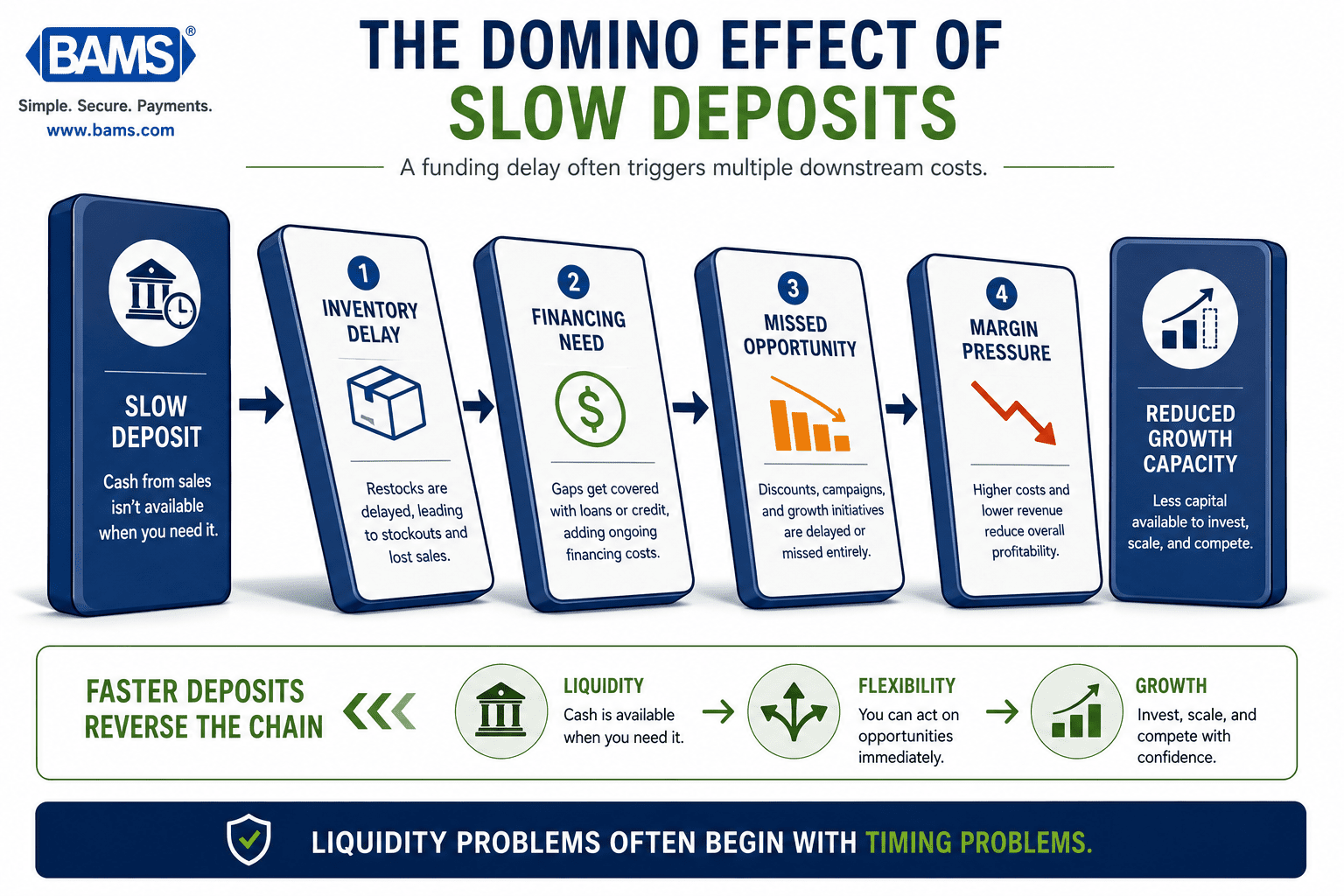

A funding delay often triggers multiple downstream costs.

These six drains share a common structure. None of them appear as “payment processing costs” in your accounting. They show up as inventory shortages, financing expenses, missed discounts, capped campaigns, inflated reserves, and slow competitive responses. This is why most operators only catch one or two. The root cause (deposit timing) is separated from the symptom by at least one layer of abstraction.

The strategic insight is that when you improve liquidity at the deposit level, the benefits cascade across every operational category. Faster deposits don’t just mean “getting your money sooner.” They mean lower financing costs, better supplier terms, more aggressive growth spending, and leaner operations. Weekly review of operating cash flow, receivables aging, and inventory turnover becomes far more actionable when you’re working with actual cash rather than projected settlements.

The compounding effect is what makes this a systems problem, not a single-point fix. Each day of faster access multiplies across every transaction, every restock cycle, and every campaign decision you make.

Where to Start: Prioritizing Your Cash Flow Forecasting Overhaul

You don’t need to address all six simultaneously. Start with the one or two that represent your largest dollar exposure. For most eCommerce operators, that’s inventory restock windows (#1) and invisible financing costs (#2), because they compound daily and affect gross margin directly.

Next, audit your current processor’s settlement terms. Document your actual deposit arrival times (not the stated terms) over 30 days. Compare the real cost of your current timing against a next-day funding arrangement. The math usually makes the decision obvious.

Finally, build a rolling 13-week cash flow forecast that accounts for deposit timing as a variable, not a constant. When you treat settlement speed as a lever you can control, your financial stability solutions shift from reactive (building bigger buffers) to proactive (deploying capital faster). That shift is where margin improvement actually lives.

Frequently Asked Questions

What is a cash flow acceleration strategy for eCommerce?

A cash flow acceleration strategy reduces the time between earning revenue and being able to spend it. For eCommerce, this primarily means shortening payment processor settlement windows (moving from 3-5 day deposits to next-day funding), capturing early payment supplier discounts, and eliminating short-term borrowing used to bridge deposit gaps. The goal is to turn processed sales into deployable cash as fast as possible.

How can businesses improve cash flow forecasting with real-time data?

Start by tracking actual deposit arrival times daily for at least 30 days, not the times your processor promises. Build a rolling 13-week forecast that includes deposit timing as a variable. Update projections weekly with real transaction volumes, supplier payment dates, and payroll obligations. When your forecast reflects when cash actually arrives (not when it’s earned), you can make purchasing and spending decisions with far greater precision.

Why is optimizing merchant services important for cash flow?

Your merchant services provider controls how quickly you access the revenue you’ve already earned. A processor with a two-day hold versus a next-day deposit creates a compounding gap across every transaction. Over a month of $10,000 daily sales, that’s $10,000 to $30,000 perpetually out of reach. Optimizing your processor relationship directly affects inventory purchasing power, financing costs, and operational agility.

How does deposit timing affect eCommerce ad spend?

Paid advertising platforms require daily budget availability, and their algorithms optimize around consistent spend. When you can’t fund a winning campaign because yesterday’s revenue hasn’t settled, you either cap the campaign or finance it with debt. Both options cost you. Faster deposits let you reinvest revenue into scaling campaigns within 24 hours of earning it, which preserves algorithm learning and maximizes return on ad spend.

Which payment solutions can help reduce processing fees and speed up deposits?

Look for processors that offer next-day funding without charging the 1% instant-payout surcharge common on many platforms. Providers like BAMS offer next-day funding with a 9 PM EST batch cutoff, which means transactions processed later in the day still qualify. Compare total cost: processing rate plus the hidden costs of slow deposits (financing, missed discounts, stockouts) rather than rate alone.

How much cash reserve should an eCommerce business maintain?

A common guideline is six months of operating expenses. However, a significant portion of that reserve often exists to cover unpredictable deposit timing. If you switch to a processor with reliable next-day funding, you may be able to reduce your buffer and redeploy that capital into inventory, marketing, or other growth activities. The right reserve size depends on your deposit predictability as much as your expense level.