9 Signals That Reveal Your Ideal Funding Speed

A diagnostic framework matching same-day vs. next-day deposits to your actual eCommerce cash flow patterns

Learn which business conditions justify paying for same-day funding and which make next-day deposits the smarter default. This diagnostic covers volume thresholds, sale event timing, and operational bottlenecks to help eCommerce operators stop overpaying for speed they don’t need.

TL;DR

- Same-day funding pays for itself in 6 specific conditions – Heavy weekend sales, frequent flash sales, dynamic ad budgets, just-in-time inventory, cross-border complexity, and payroll timing crunches all create cash flow gaps that faster settlement directly closes.

- Next-day funding is the smarter default in 3 conditions – If your monthly volume is below $50K, your expenses are predictable, or you operate in a low-chargeback category, the premium for same-day speed rarely justifies itself.

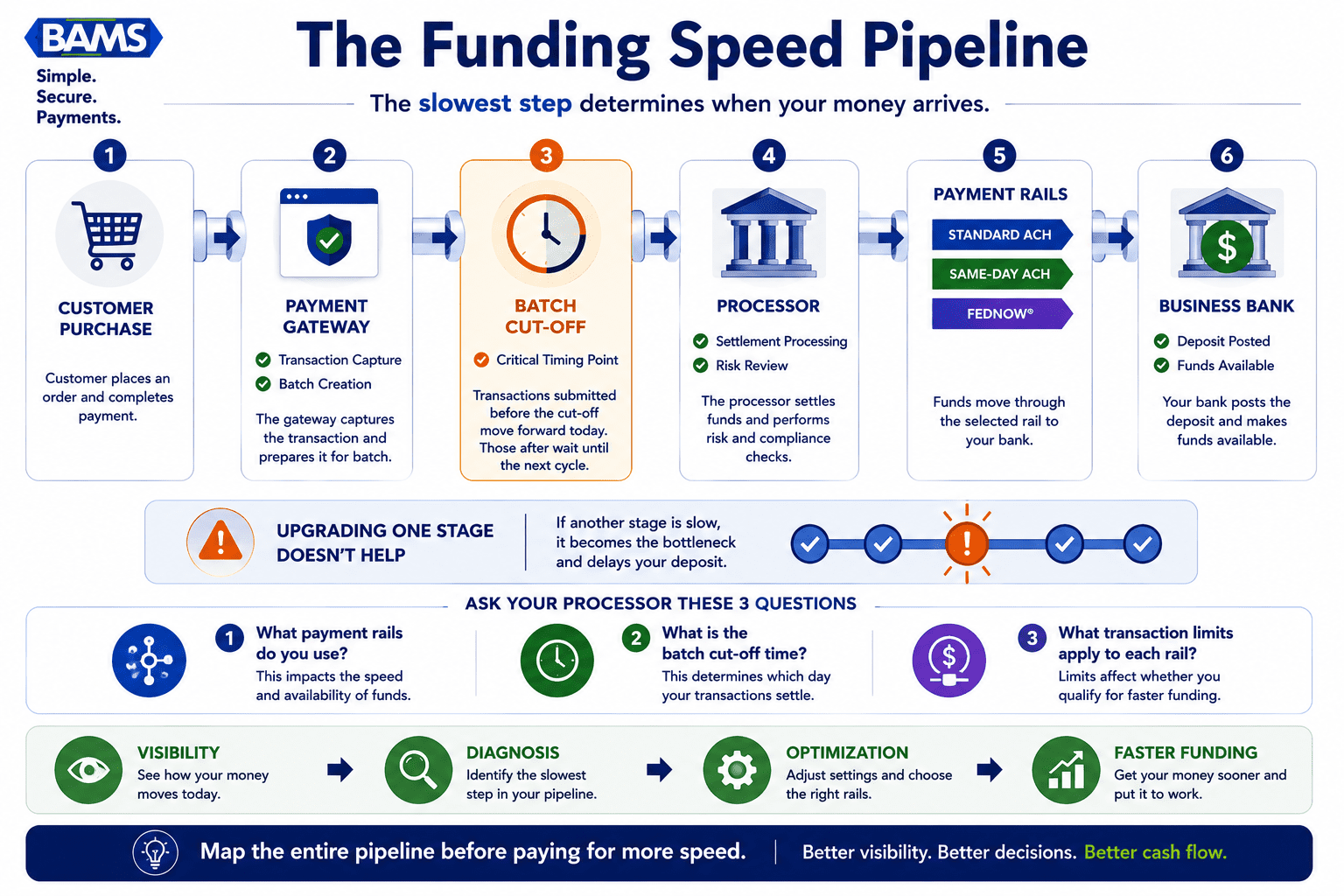

- Funding speed is a supply chain variable, not just a payment feature – Your gateway, processor, payment rails, and bank form a pipeline. The slowest link sets your real deposit speed, so map the whole chain before upgrading any single stage.

- Start with data, not assumptions – Pull 12 weeks of deposit timing and overlay it against your major expense dates. This reveals whether a gap exists and whether faster funding or lower processing costs is the better investment.

- Ask your processor three questions – What payment rails do they use, what is the batch cut-off time, and what are the transaction limits for each funding speed? The answers determine what “fast” actually means for your account.

The Real Cost of Faster Money

Delayed deposits are not just an inconvenience. For eCommerce operators managing inventory cycles, ad spend, and payroll on tight timelines, the gap between receiving a payment and accessing that cash determines what you can do next. More than two-thirds of small-business owners reported concern about their ability to access capital in a recent survey, and much of that anxiety traces back to timing rather than revenue volume.

Business capital access is rarely a binary problem. The question is not whether faster funding exists, but whether it solves a bottleneck you actually have. Same-day funding and next-day funding sit on different payment rails, carry different costs, and fit different operational profiles. Treating them as interchangeable leads to overpaying for speed you don’t need, or leaving money on the table when you do.

The fastest funding option isn’t always the best funding option. Match funding speed to your actual cash flow needs.

Who This Diagnostic Is For (and What It Skips)

This guide is built for eCommerce managers at established online businesses processing enough monthly volume that deposit timing has a measurable effect on operations. If you run a Shopify, WooCommerce, or custom-platform store with 10 to 50 employees, and you’ve ever delayed a restock or paused an ad campaign because funds hadn’t cleared, this applies to you.

We are not covering startup financing, SBA loans, or lines of credit. We are also not ranking processors head-to-head. Instead, this is a diagnostic: nine specific business conditions that tell you whether same-day funding will pay for itself or whether next-day funding is the smarter, cheaper default.

How These Signals Were Selected

Each condition below was evaluated against three criteria: does it create a measurable cash flow gap, does faster settlement close that gap in a way that offsets any added cost, and does it apply to a recurring pattern rather than a one-time event? The result is a framework grounded in settlement mechanics, not marketing claims. As the Bipartisan Policy Center noted, fintech tools that use faster, data-rich processes can meaningfully broaden capital access, but only when speed reduces a real opportunity cost.

6 Conditions Where Same-Day Funding Pays for Itself

1. Your Weekend Sales Represent More Than 30% of Weekly Revenue

Why it matters: Standard ACH settlement does not process on weekends. If your store generates a disproportionate share of revenue on Saturday and Sunday, those funds sit idle until Monday’s batch clears, often landing Tuesday or Wednesday. That is a 3-to-4 day gap on your highest-volume days.

What it looks like today: Same-day ACH windows and FedNow rails now allow processors to push settlements on the same calendar day the batch closes. Not every processor supports weekend-initiated same-day transfers, but the infrastructure exists. Your gateway’s batch cut-off time is the first bottleneck to check. The ACH Network continues to support faster movement of funds between businesses and financial institutions, making accelerated settlement options more widely available than in previous years.

How to apply it: Pull your last 12 weeks of sales data and calculate weekend revenue as a percentage of total weekly revenue. If it consistently exceeds 30%, model the cost of a same-day funding add-on against what you could do with that cash 2 to 3 days sooner (restock, reinvest in ads, cover Monday payroll).

2. You Run Flash Sales or Limited-Time Promotions at Least Monthly

Why it matters: Flash sales compress revenue into a narrow window, often 24 to 72 hours. If that cash takes 2 to 3 business days to arrive, you cannot reinvest it into the next promotion or replenish the inventory you just sold. The delay breaks your momentum cycle.

What it looks like today: eCommerce brands running frequent sale events increasingly treat deposit speed as a campaign variable. The question is whether your processor’s settlement schedule aligns with your promotional calendar, or fights against it.

How to apply it: Map your promotional calendar against your current settlement timeline. If post-sale cash consistently arrives after you need it for restocking or the next campaign’s ad budget, same-day funding closes a gap that directly affects revenue velocity.

3. Your Ad Spend Scales Dynamically with Available Cash

Why it matters: Many eCommerce operators manage paid acquisition on a cash-available basis rather than a fixed monthly budget. When deposits are delayed, ad spend gets throttled during high-performing windows. You lose impressions and conversions not because the campaign underperformed, but because the cash from yesterday’s sales has not arrived.

What it looks like today: Platforms like Meta and Google now offer automated budget scaling based on performance signals. If your funding cannot keep pace with the algorithm’s appetite for spend during a winning streak, you leave revenue on the table.

How to apply it: Track instances where you manually paused or reduced ad spend because of cash availability (not performance). If this happens more than twice a month, faster settlement likely pays for itself in recovered ROAS.

4. You Manage Inventory with Just-in-Time Purchasing

Why it matters: Just-in-time inventory minimizes warehousing costs but demands precise cash flow timing. A 48-hour deposit delay can mean the difference between placing a restock order and missing a supplier’s cut-off window, leading to stockouts that cost more than any processing fee.

What it looks like today: Suppliers increasingly offer tighter order windows, especially for trending or seasonal products. Your payment processor’s funding speed is now part of your supply chain, whether you designed it that way or not.

How to apply it: Identify your top 5 SKUs by velocity. For each, compare the typical reorder lead time against your average deposit arrival. If the gap creates stockout risk even once per quarter, same-day funding is a supply chain investment, not just a payment feature.

5. Your Business Operates Across Multiple Time Zones or Cross-Border

Why it matters: Cross-border transactions and multi-timezone customer bases introduce additional settlement complexity. Currency conversion, international card network routing, and mismatched banking hours can add 1 to 2 days on top of standard domestic settlement. These hidden delays compound.

What it looks like today: Domestic same-day ACH and FedNow do not apply to international transactions, but having faster domestic settlement frees up working capital that would otherwise be tied up waiting for cross-border deposits to clear. It is a partial solution that still moves the needle.

How to apply it: Segment your transaction data by domestic versus international. If international sales create unpredictable deposit timing, accelerating the domestic side gives you a more stable cash position to absorb the variance.

6. Payroll Timing Creates a Recurring Cash Crunch

Why it matters: If your payroll cycle lands mid-week and your deposits consistently arrive a day or two late, you are either maintaining a larger cash reserve than necessary or risking a shortfall. Both are expensive. The reserve ties up capital. The shortfall damages trust.

What it looks like today: Businesses with 10 to 50 employees often run biweekly payroll. When deposit timing is unpredictable, owners compensate by holding excess cash in checking accounts earning nothing, effectively paying an invisible fee for slow funding.

How to apply it: Compare your payroll dates against your average deposit arrival over the last 6 months. If you routinely hold more than one payroll cycle’s worth of cash as a buffer, same-day funding can reduce that reserve and free the difference for growth.

3 Conditions Where Next-Day Funding Is the Smarter Default

7. Your Monthly Processing Volume Is Below $50,000

Why it matters: Same-day funding often comes with per-transaction or monthly premium fees. At lower volumes, the math rarely works out. The cost of faster settlement exceeds the value of having cash a few hours sooner, especially if your expenses are predictable and your cash cycle is stable.

What it looks like today: Many processors offer next-day funding as a standard feature at no additional cost, while same-day funding carries a surcharge. For businesses under $50,000 per month, next-day funding provides the speed improvement that matters most (compared to the traditional 2-to-3 day cycle) without the premium. BAMS includes next-day funding as a standard part of their merchant accounts, which makes it a practical baseline for businesses in this volume range.

How to apply it: Calculate your average monthly volume and compare same-day funding surcharges against the actual cash flow benefit. If you cannot identify a specific, recurring cost that faster funding eliminates, next-day is the cost-effective choice.

8. Your Expense Timing Is Predictable and Weekly

Why it matters: If your major expenses (inventory orders, ad payments, payroll) land on predictable weekly cycles and your deposits arrive reliably the next business day, there is no gap to close. Same-day funding solves a timing mismatch. If no mismatch exists, you are paying for speed without a purpose.

What it looks like today: Businesses with stable, recurring expense patterns and reliable next-day deposits often find that their cash flow is already optimized. The constraint is not deposit speed but margin, pricing, or volume. In those cases, reviewing your processing fee structure will likely yield more savings than upgrading settlement speed.

How to apply it: Map your top 5 recurring expenses by date against your deposit arrival pattern for the last 8 weeks. If deposits consistently arrive before expenses are due, next-day funding already covers your needs.

9. You Operate in a Low-Chargeback, Low-Refund Category

Why it matters: Same-day funding introduces a subtle risk: if funds hit your account before chargebacks or refunds are processed, you need to maintain a buffer for those reversals. In high-chargeback categories, this can create accounting complexity and unexpected shortfalls. In low-risk categories, this is less of a concern, but the benefit of same-day speed is also smaller because the cash flow is already stable.

What it looks like today: Processors evaluate chargeback ratios and transaction limits when approving same-day funding eligibility. If your category carries low dispute rates and your refund volume is minimal, you qualify easily but benefit least. Next-day funding gives you nearly the same operational advantage at a lower cost.

How to apply it: Check your chargeback ratio and monthly refund rate. If both are consistently below industry averages and your cash flow is stable, next-day funding is the pragmatic choice. Reserve same-day funding for periods when your business conditions change (seasonal spikes, new product launches).

The Pattern Underneath These Signals

Your processor does not determine funding speed alone. The entire payment pipeline does.

Three themes connect all nine conditions. First, funding speed is a supply chain variable, not a payment feature. It interacts with inventory cycles, ad spend pacing, and payroll timing in ways that are specific to your business, not generic to your industry. Second, the value of faster settlement is proportional to the volatility of your cash flow. Predictable businesses benefit less. Businesses with spiky revenue patterns or tight reinvestment loops benefit more.

Third, and most overlooked: your processor, gateway, batch cut-off time, and bank all form a pipeline. Upgrading one stage (say, same-day ACH) does not help if another stage (say, a 9 PM batch cut-off that your gateway misses) is the actual bottleneck. Before paying for faster funding, map the entire pipeline from transaction to deposit. The slowest link sets your real speed.

Where to Start: A Payment Processor Comparison Framework

You do not need to act on all nine signals at once. Start with two steps. First, pull 12 weeks of deposit data and overlay it against your major expense dates. This reveals whether a timing gap exists and how large it is. Second, ask your processor three questions: what payment rails do they use for settlement, what is the batch cut-off time, and what are the transaction limits for same-day versus next-day funding?

If you discover that next-day funding already covers your needs, focus your energy on reducing processing costs instead. If you find a recurring gap that same-day funding would close, calculate the cost of that gap (missed restocks, throttled ads, payroll buffers) and compare it to the premium. The right answer is the one that matches your cash flow pattern, not the one that sounds faster.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means the money from your credit and debit card transactions is deposited into your bank account by the next business day after your batch closes. Standard funding typically takes 2 to 3 business days. Next-day funding uses faster ACH processing and tighter batch schedules to shorten that gap. Most processors require you to close your batch before a specific cut-off time (often between 7 PM and 11 PM ET) to qualify for next-day deposit.

How does same-day funding differ from next-day funding?

Same-day funding pushes deposits to your bank account on the same calendar day the batch closes, using same-day ACH or newer rails like FedNow. Next-day funding deposits arrive the following business day. Same-day funding typically carries a per-transaction or monthly surcharge and may have stricter eligibility requirements, including lower transaction limits and minimum processing history. The practical difference is hours, not days, but those hours matter when cash flow timing is tight.

How can a business qualify for next-day funding?

Qualification depends on your processor, but common requirements include a minimum processing history (often 3 to 6 months), a chargeback ratio below a set threshold, a U.S.-based bank account, and batching before the processor’s daily cut-off time. Some processors also require a minimum monthly volume. BAMS offers next-day funding as a standard feature for qualifying merchants, with clear batch cut-off guidelines.

Which factors affect the speed of my deposits beyond my processor?

Four factors form a pipeline: your payment gateway’s batch schedule, your processor’s settlement window, the payment rails used (standard ACH, same-day ACH, or FedNow), and your bank’s posting schedule. A delay at any stage slows the entire chain. For example, if your gateway batches at midnight but your processor’s same-day ACH cut-off is 10 PM, you miss the window regardless of what you paid for. Always ask about the full pipeline, not just the processor’s advertised speed.

When should a business consider upgrading to same-day funding?

Consider same-day funding when you can identify a specific, recurring cost created by deposit delays. Examples include throttled ad spend during high-performing campaigns, stockouts caused by late restock orders, or payroll buffers that tie up working capital. If you cannot point to a concrete cost, next-day funding is likely sufficient and more cost-effective.

Are there transaction limits that affect same-day or next-day funding?

Yes. Same-day ACH currently has a per-transaction limit of $1 million set by NACHA, but individual processors may impose lower caps based on your account history and risk profile. Next-day funding transaction limits vary by processor and are generally more flexible. High-ticket eCommerce businesses should confirm their processor’s specific limits before assuming all transactions qualify for accelerated settlement.

Sources