Business Funding Alternatives: The Problem Is Your Processor

Why eCommerce operators borrow money to cover gaps their own payment infrastructure created

Discover why most cash flow gaps aren’t funding problems—they’re settlement timing problems. Learn how optimizing payment processing cadence can eliminate the need for costly business funding alternatives.

TL;DR

- Cash flow gaps are often processor-made, not business-made – Slow settlement schedules, misaligned batch times, and legacy payment rails create artificial delays between earning revenue and accessing it.

- Borrowing to bridge deposit delays is a symptom, not a strategy – When businesses use credit lines or cash advances to cover timing mismatches, they’re paying interest on a problem their payment infrastructure could solve.

- Settlement speed is architecture, not a perk – Your gateway, processor cut-off times, bank relationships, and underwriting all determine deposit timing. These are configurable variables, not fixed constraints.

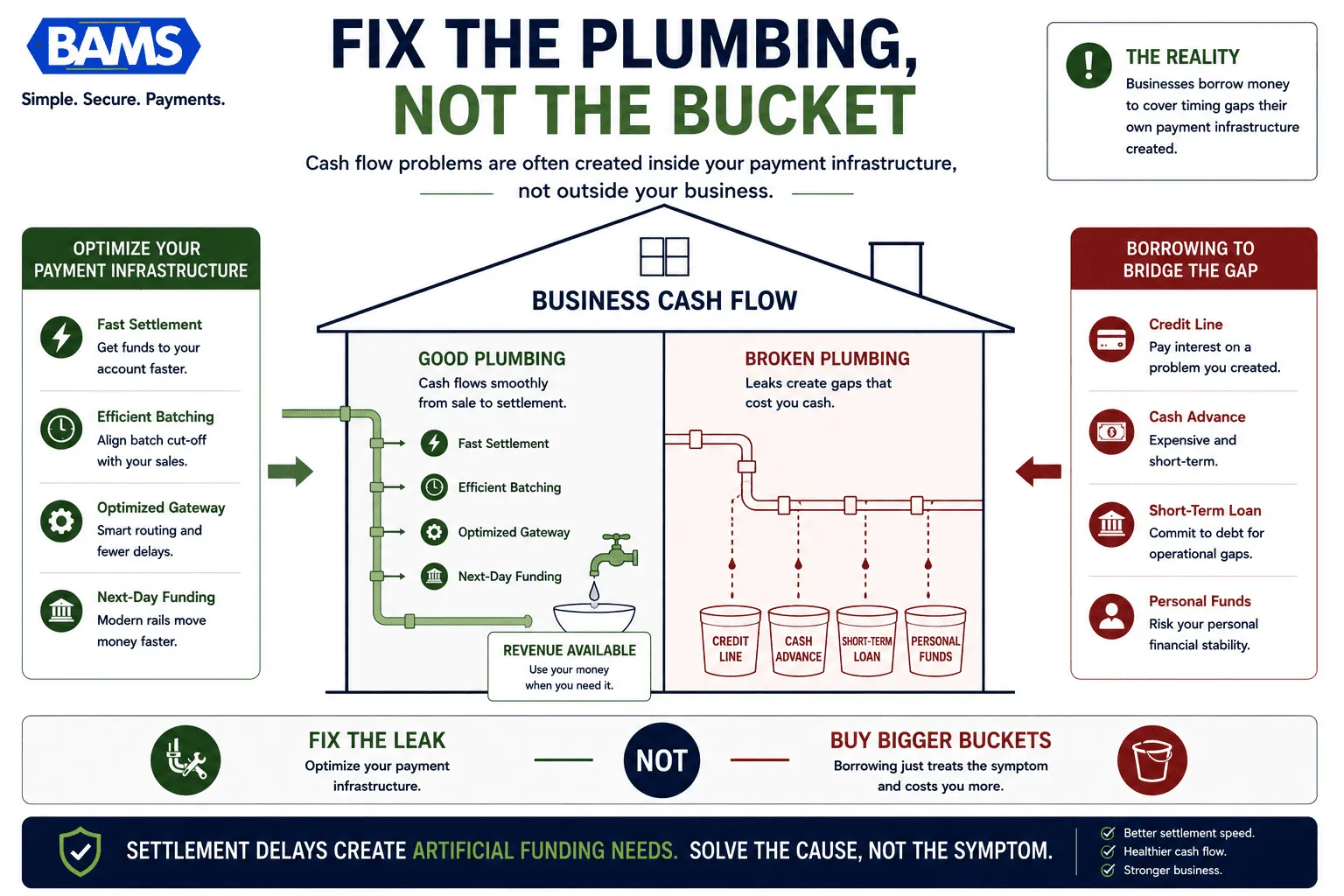

- Fix the plumbing before buying a bigger bucket – Evaluate your payment processing stack for deposit speed before turning to business funding alternatives. Next-day funding eliminates most of the gap that drives reactive borrowing.

You’re Not Underfunded. You’re Waiting Too Long to Get Paid.

There’s a quiet absurdity in eCommerce right now. Businesses are generating revenue every single day, then turning around and borrowing money to cover the gap between earning it and actually holding it. We’re not talking about capital for growth or inventory expansion. We’re talking about business funding alternatives used to bridge a delay created by their own payment processing setup.

That’s not a funding problem. That’s a plumbing problem.

The Borrowed-Time Economy Everyone Accepts

The conventional wisdom goes like this: cash flow gaps are an inevitable cost of running a business online. You sell on Friday night, your processor batches on Monday, your bank settles on Wednesday. In the meantime, you need to pay suppliers, cover payroll, fund ad spend. So you open a line of credit, swipe a personal card, or take a merchant cash advance to keep things moving.

And the numbers confirm how normalized this has become. According to the Federal Reserve’s 2025 Small Business Credit Survey, many businesses continue to seek outside financing to support operations and manage cash flow challenges. The U.S. Department of the Treasury found the most common source of alternate funding is personal savings or credit cards. Everyone treats this as the price of doing business. Nobody asks whether the business itself is creating the problem.

The Problem Isn’t Capital. It’s Cadence.

Many cash flow problems begin long before a lender enters the picture.

Here’s what we actually believe: taking on debt to bridge a cash gap caused by your own processor’s settlement schedule isn’t a funding strategy. It’s a system failure you’re paying interest on.

The distinction matters enormously. When you frame slow deposits as “just how it works,” you accept a recurring cost that compounds quietly. When you frame it as a controllable variable in your payment infrastructure, you can actually fix it.

Inside the Settlement Pipeline Most Merchants Never See

Let’s trace what actually happens after a customer clicks “buy” on your site. Their card information passes through your payment gateway, hits the card network, reaches the issuing bank, gets authorized, and returns a confirmation. That’s the part you see. What you don’t see is where the delays hide.

After authorization, your processor batches your transactions. Some batch once a day. Some batch at a fixed cut-off time that may not align with when your sales actually peak. If your batch closes at 3 PM Eastern but your biggest sales window is 7 PM to midnight, every evening transaction rolls to the next day’s batch before the settlement clock even starts.

Then the batch enters the settlement network. Traditional ACH settlement takes one to two business days. Weekends and holidays don’t count. So a Friday night sale batched Saturday morning might not begin settlement until Monday, with funds arriving Tuesday or Wednesday. That’s a four-to-five day gap between revenue and access, on a transaction your customer completed in 30 seconds.

Now multiply that by a weekend sales surge, a flash sale, or a holiday shopping event. Suddenly you’re sitting on tens of thousands in earned revenue you can’t touch. And the instinct, understandably, is to look for financial stability solutions: a credit line, a cash advance, a short-term loan to bridge the gap.

But the gap itself is artificial.

It’s created by batch timing, settlement schedules, and the specific relationship between your processor, your gateway, and your bank. Those are all configurable. The Federal Reserve has noted that small businesses “seek financing from a variety of sources” and increasingly turn to nonbank lenders when they need funds quickly. Speed and access are driving these decisions. But what if the need for speed was manufactured by the very system processing your payments?

Same-day ACH and newer rails like FedNow have changed what’s mechanically possible. Yet most processors haven’t updated their default settlement schedules to match. They’re running modern transaction volumes on legacy timing. The result: you’re modern on the front end (instant checkout, digital wallets, one-click buy) and stuck in a time warp on the back end.

This is where your specific setup matters more than any generic “next-day funding” feature. The gateway you use, the cut-off times your processor enforces, whether your merchant account is underwritten for faster settlement, and even which bank receives your deposits all create compounding micro-delays. A provider like BAMS, which offers next-day funding as a standard part of its merchant services, eliminates much of this friction by design. But the broader point is that deposit speed isn’t a perk. It’s architecture.

Customers finish paying long before many businesses can actually use the money.

What Changes When You Stop Borrowing Against Your Own Revenue

If this thesis is right, the implications ripple outward. Every dollar you spend on interest to cover a settlement-induced cash gap is margin you’re burning and every hour you spend managing a credit line or reconciling a cash advance is time not spent on growth. Every decision you make under cash pressure (delaying a restock, pulling back ad spend, negotiating worse supplier terms) is a strategic compromise forced by your processor’s schedule, not your business’s performance.

The eCommerce operators who figure this out first gain a structural advantage. Not because they found cheaper debt, but because they stopped needing it for this purpose entirely. When your deposits arrive the next business day, your cash flow management shifts from reactive to predictable. You restock based on demand signals, not deposit dates. You scale ad spend when the data says to, not when your balance allows it.

Rethinking the Funding Question Entirely

We’d offer this reframe: stop asking “how do I fund the gap?” and start asking “why does the gap exist?” The first question leads you to lenders. The second leads you to your payment infrastructure.

Think of it like heating a house with the windows open. You can always buy a bigger furnace. Or you can close the windows. Business funding alternatives have their place, genuinely, for inventory expansion, new market entry, capital equipment. But when you’re borrowing to cover a timing mismatch your own processor created, you’re buying the furnace.

Settlement speed isn’t a feature. It’s the foundation your entire cash flow sits on.

The Real Cost of “Just How It Works”

We’ve watched too many eCommerce operators treat three-to-five day settlement as gravity. Something fixed and immovable. It isn’t. It’s a choice embedded in your payment processing stack, and it’s a choice you can change.

The businesses that thrive aren’t necessarily the ones with the most capital. They’re the ones with the least friction between earning revenue and deploying it. That’s not a funding insight. That’s an infrastructure one.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your processed transactions are deposited into your bank account the following business day instead of the typical two-to-five day wait. It’s a settlement speed determined by your processor’s infrastructure, batch timing, and banking relationships.

Why do so many small businesses borrow to cover cash flow gaps?

Most cash flow gaps in eCommerce aren’t caused by low revenue. They’re caused by slow settlement schedules that delay access to money already earned, pushing businesses toward credit lines or cash advances to cover operational costs in the meantime.

Which factors affect how fast a business receives its deposits?

Batch cut-off times, the settlement network your processor uses (traditional ACH vs. same-day ACH), your bank’s processing speed, and whether your merchant account is underwritten for faster funding all play a role. Weekend and holiday schedules add further delays.