Contactless Payments: The Fraud Risk Nobody Mentions

Digital wallets reduce fraud at the network level — but merchants still lose revenue where it counts

Learn why tokenized transactions don’t protect merchants from chargebacks the way the industry implies. This piece exposes the gap between network-level fraud reduction and the dispute evidence eCommerce operators actually need to protect revenue.

TL;DR

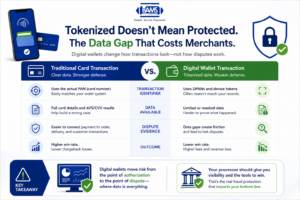

- Digital wallets reduce authorization fraud, not chargebacks – Tokenization and biometrics protect the payment rail, but friendly fraud and disputes still hit your bottom line the same way.

- Wallet transactions make dispute defense harder – Tokenized data (DPANs, Device Account Numbers) often doesn’t map cleanly to your order system, weakening your chargeback evidence.

- Your processor matters more than your payment method – The real differentiator is whether your processor surfaces usable dispute data and provides proactive chargeback defense for wallet transactions.

- Think of digital wallets as fraud redistribution – Risk moved from the point of authorization to the point of dispute, exactly where most merchants have the least visibility.

The Safest Transaction You’ll Ever Lose Money On

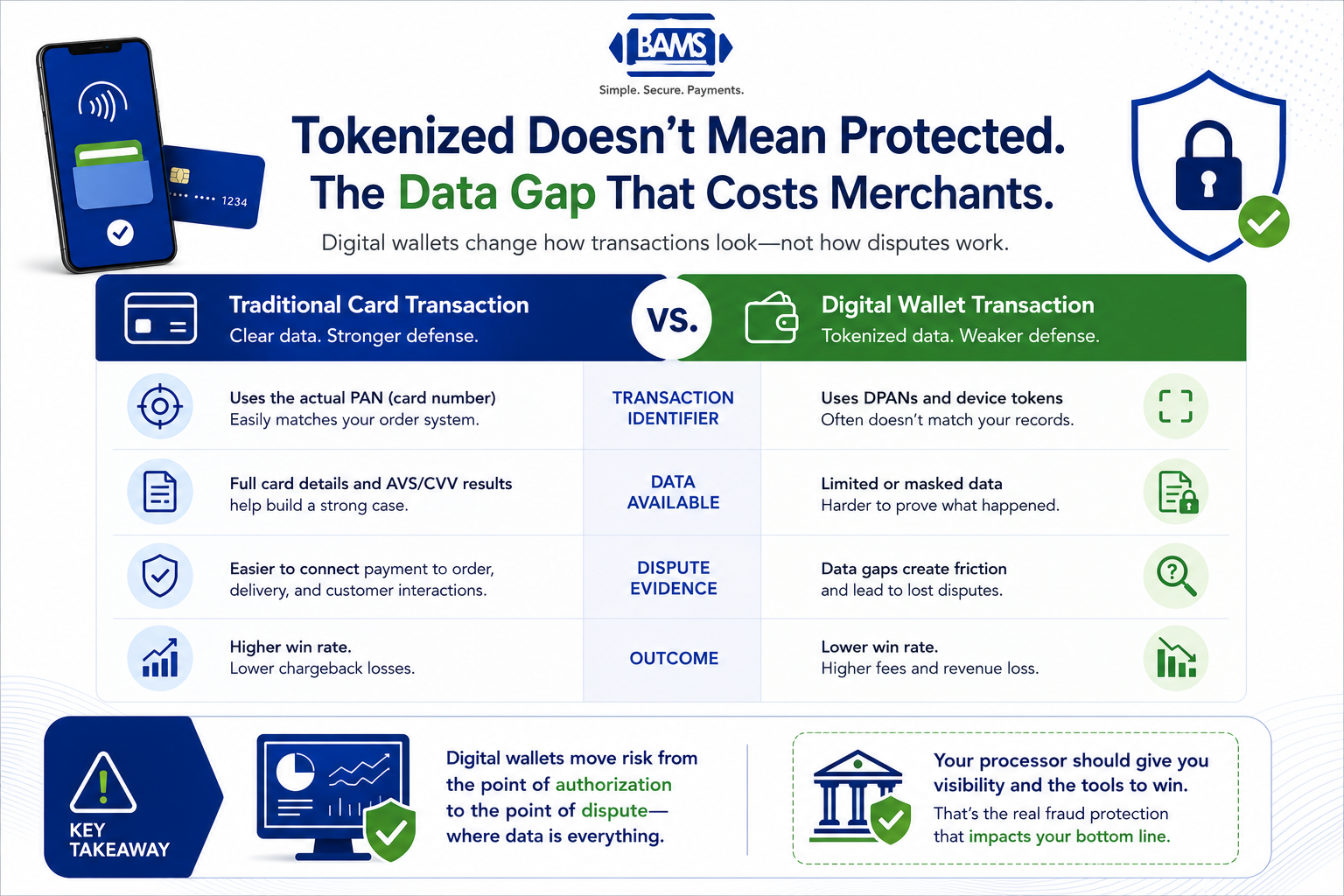

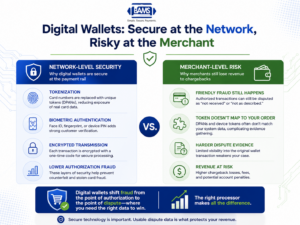

Digital wallets are everywhere. Apple Pay, Google Pay, Samsung Pay. Your customers love them. The payments industry loves talking about how secure they are. And they’re right, technically. Tokenization, biometric authentication, encrypted Device Account Numbers: the technology is genuinely impressive.

But here’s the part nobody mentions at the conference keynote: you can still get hit with a chargeback on a tokenized transaction, and when you do, the dispute process is harder to navigate than it was with a plain old credit card number. For eCommerce operators watching contactless payments volume climb, that gap between “safer” and “protected” is where revenue quietly disappears.

The Industry’s Favorite Half-Truth About Digital Wallets

The standard narrative goes like this: mobile wallets replace card numbers with tokens, add biometric verification, and make fraud nearly impossible. The card networks publish case studies. Processors repeat the talking points. Everyone agrees that accepting contactless payments is a net positive for security.

And at the network level, that’s true. Tokenization does reduce counterfeit fraud. Biometrics do make unauthorized use harder. The aggregate numbers look good.

But aggregate numbers don’t pay your bills. The question that matters to a 30-person eCommerce operation isn’t “is the payment ecosystem safer?” It’s “when a customer disputes an Apple Pay transaction, do I have what I need to win?” The industry answers the first question loudly and ignores the second almost entirely.

Security Theater Doesn’t Prevent Chargebacks

Here’s what we actually believe: the real payment fraud risk for eCommerce merchants isn’t that digital wallets are insecure. It’s that the security narrative has made merchants complacent about dispute readiness, while the tools processors give them to fight chargebacks on wallet transactions haven’t kept pace with the technology itself.

The framing needs to flip. Stop asking “are digital wallets safe?” Start asking “when a wallet transaction goes sideways, can my processor show me what happened?”

Digital wallets improve payment security through tokenization and biometrics, but merchants still face chargeback risks without strong dispute data and processor support.

Where the Revenue Actually Leaks

Let’s walk through what happens in practice. A customer buys a $180 item from your store using Apple Pay in their browser. The transaction is tokenized. A Device Account Number replaces the real card number. Biometric authentication confirms the buyer’s identity on their device. Everything checks out.

Three weeks later, a chargeback lands. The reason code says “product not received” or “not as described.” This isn’t card-not-present fraud in the traditional sense. The cardholder authorized the purchase. The token worked perfectly. But the customer wants their money back, and the issuing bank sided with them.

Now you need to build a dispute response. And this is where things break down for most eCommerce merchants.

With a traditional card transaction, you’d pull the card number, match it to your order system, cross-reference shipping confirmation, and submit your evidence. Straightforward. With a tokenized wallet transaction, the card number you see in your processor dashboard may be a DPAN (Device Primary Account Number) that doesn’t match anything in your CRM. The transaction ID format might differ. The metadata your fraud tools rely on, like AVS matches or CVV verification, often doesn’t apply to wallet payments the same way. Mastercard Developers documents the secure tokenization architecture used by digital payment credentials, including Device Primary Account Numbers (DPANs) and related transaction data.

PCI Security Standards Council guidance explains how tokenization protects payment credentials while reducing exposure to stolen card data. Card-not-present fraud losses are projected to reach around $28 billion by 2026, a 40% jump from 2023. And a growing share of CNP transactions now flow through digital wallets. The fraud isn’t happening because tokenization failed. It’s happening because friendly fraud, first-party misuse, and social engineering don’t care about tokens. They exploit the dispute process, not the payment rail.

As payment technologies evolve, fraud increasingly shifts away from stolen card credentials toward account misuse, social engineering, and post-transaction disputes. Strong authentication alone does not eliminate the need for effective chargeback management.

Merchants continue to face fraud risks that extend beyond payment authorization, making operational visibility and dispute readiness just as important as fraud prevention. The threat is broad, persistent, and increasingly aimed at the operational seams between payment acceptance and dispute resolution.

This is where your processor matters more than your payment method. If your processor surfaces tokenized transaction data in a way that maps cleanly to your order management system, you can fight the chargeback. If it doesn’t, you’re submitting incomplete evidence and hoping for the best. Most small-to-midsize merchants we’ve seen are in the second camp and don’t realize it until the losses accumulate.

Tools like BAMS’ proactive chargeback defense exist specifically to close this gap, giving merchants dedicated support that translates wallet transaction data into usable dispute evidence before revenue walks out the door. That kind of hands-on account management matters more when the transaction data itself has gotten more complex.

What Changes If You Take This Seriously

If this framing is right, several things follow. First, evaluating a processor based on transaction fees alone becomes dangerously incomplete. The processor that saves you eight basis points but leaves you blind on wallet dispute data costs you far more in lost chargebacks over a quarter.

Second, your chargeback defense workflow needs a wallet-specific layer. The evidence package for an Apple Pay dispute is not the same as a keyed-in Visa transaction. If your team treats them identically, your win rate will reflect that.

Third, the merchants who understand how different mobile payment types flow through their systems will have a structural advantage over those who just “accept everything” and sort it out later. Cumulative online payment fraud losses are expected to hit around $300 billion for merchants between 2023 and 2027. The operators who survive that wave won’t be the ones with the best fraud walls. They’ll be the ones with the best dispute infrastructure.

Tokenization changes how payment information is stored, but merchants still need accessible transaction data to successfully defend against chargebacks.

A Better Way to Think About Payment Fraud Risks

Stop thinking of digital wallets as a fraud solution. Think of them as a fraud redistribution. Tokenization moved risk away from the point of authorization and toward the point of dispute. The vulnerability didn’t disappear. It migrated downstream, to the part of the process where most merchants have the least visibility and the fewest resources.

The useful question isn’t “do we accept Apple Pay?” Of course you do. Your customers expect it. The useful question is: “When an Apple Pay transaction becomes a chargeback, does our processor give us the data and support to defend it?”

That’s the frame that protects revenue. Everything else is a press release.

The Merchants Who Win Disputes Win the Margin War

Digital wallets aren’t going away. Adoption will keep climbing. The payment rails will keep getting more secure at the network level. None of that changes the fact that chargebacks are an operational problem, not a cryptographic one.

The merchants who protect their revenue won’t be the ones who trusted the technology to do it for them. They’ll be the ones who demanded transparency from their processors and built dispute workflows that match the complexity of how people actually pay today.

According to the Federal Reserve Bank of St. Louis, card payment activity and related fee revenue continue to grow, making dispute management and payment transparency increasingly important for merchants.

Frequently Asked Questions

Does tokenization in Apple Pay eliminate chargeback risk for merchants?

No. Tokenization protects against counterfeit card fraud at the point of authorization, but it does not prevent chargebacks from friendly fraud, product disputes, or first-party misuse. Merchants still need robust dispute evidence and processor support to defend wallet-based chargebacks.

What are the risks of using Apple Pay for online transactions?

The primary risk isn’t unauthorized use. It’s that tokenized transaction data can be harder to match to order records during disputes, making chargeback defense more difficult. Merchants who lack processor tools that clearly surface wallet transaction details face higher loss rates on disputes.

How should merchants adjust their fraud prevention strategies for digital wallet payments?

Build a dispute workflow that accounts for wallet-specific data formats like DPANs and Device Account Numbers. Choose a processor that provides transparent, matchable transaction data and proactive chargeback support rather than relying solely on the wallet’s built-in security.