Ecommerce Profitability: The Checkout Fields Tax

Why missing L3 data fields silently inflate every B2B and government card transaction you process

Learn how incomplete checkout data costs eCommerce merchants hundreds of basis points on commercial and government card transactions. Discover why L3 line-item data is the most overlooked lever for eCommerce profitability in B2B selling.

TL;DR

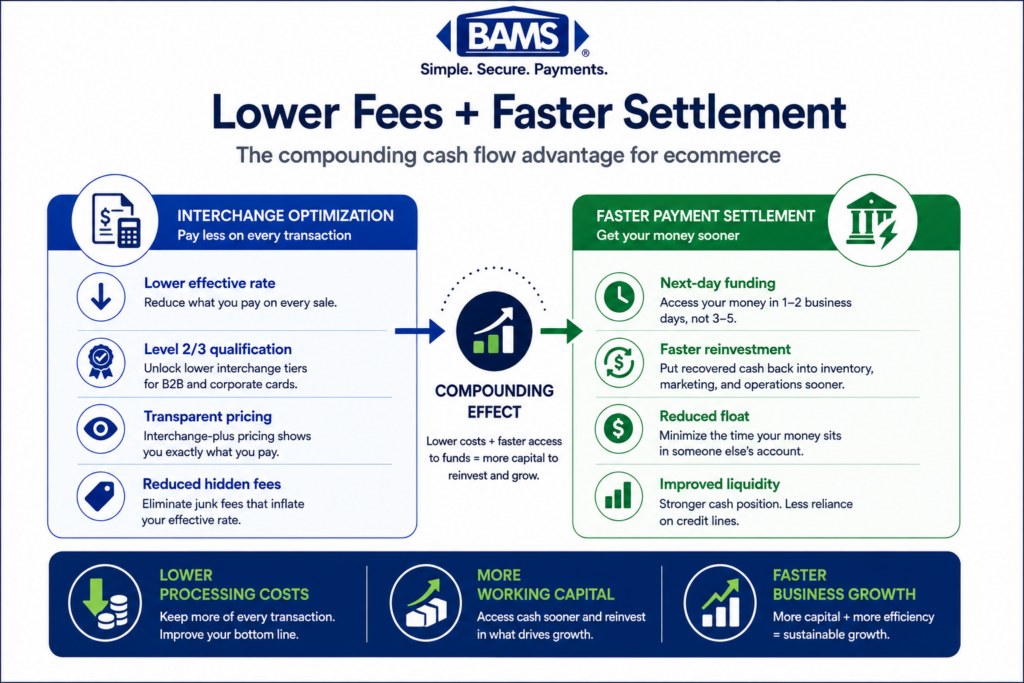

- Level 3 data is a margin lever, not a technical detail – Passing tax, freight, and line-item fields with commercial card transactions can lower interchange rates by 0.30% to 1.00%+ per transaction.

- Most eCommerce checkouts drop critical fields – The data exists in your platform, but gaps between your cart, gateway, and processor mean it never reaches the card network in the right format.

- Your effective rate is built, not negotiated – The merchants with the lowest processing costs aren’t better negotiators. They configure their checkout to qualify every transaction at the lowest possible tier.

- Every month you delay costs real money – On B2B and government card volume, downgrade fees compound quickly, often dwarfing the processor markup merchants spend weeks negotiating.

The Discount You’re Leaving on the Table at Checkout

Most eCommerce merchants obsess over conversion rates, ad spend, and shipping costs. Almost none of them look at the checkout fields they’re failing to pass to their payment processor. That’s a problem, because those missing fields are quietly inflating every transaction fee on every commercial, government, and corporate card order you process.

If you sell B2B or accept procurement cards, the gap between what you pay and what you could pay on processing fees isn’t a market rate. It’s a configuration choice. And it’s one of the most overlooked levers for eCommerce profitability that exists today.

Most B2B ecommerce merchants already collect the required data. The problem is that the checkout never sends it correctly.

Why Everyone Treats Processing Fees Like the Weather

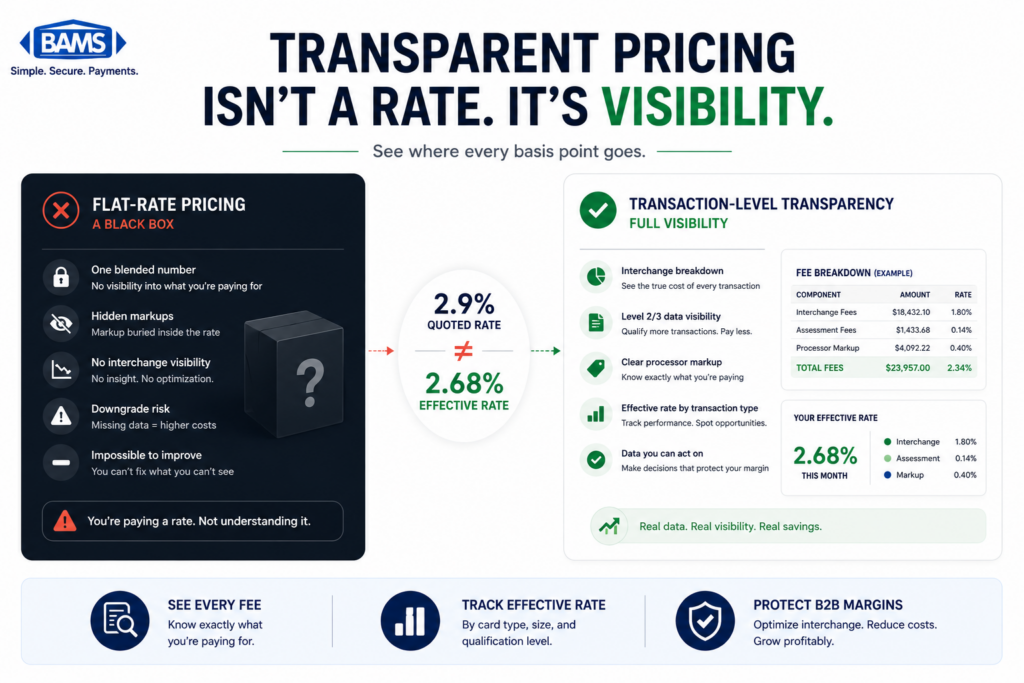

The conventional wisdom goes like this: processing fees are a cost of doing business. You shop around, maybe negotiate a few basis points, pick a flat-rate or interchange-plus plan, and move on. The rate is the rate.

This thinking made sense when most online orders came from consumer credit cards. But commercial and B2B payment volume continues to grow rapidly, and Merchant Payments Coalition resources continue to highlight the increasing financial impact interchange and swipe fees have on merchants processing corporate and procurement card transactions. These cards play by different rules. They qualify for significantly lower interchange rates, but only if the merchant passes specific line-item data with the transaction.

Most eCommerce platforms don’t do this by default. So merchants pay the highest possible rate on every single one of those orders, and they assume that’s just what processing costs.

Processing Fees Aren’t Fixed. They’re Configured.

Here’s what we actually believe: every B2B or government order processed without Level 3 data is a voluntary surcharge, one that compounds across every wholesale and procurement transaction your store handles. The checkout fields you skip are the discount you don’t collect.

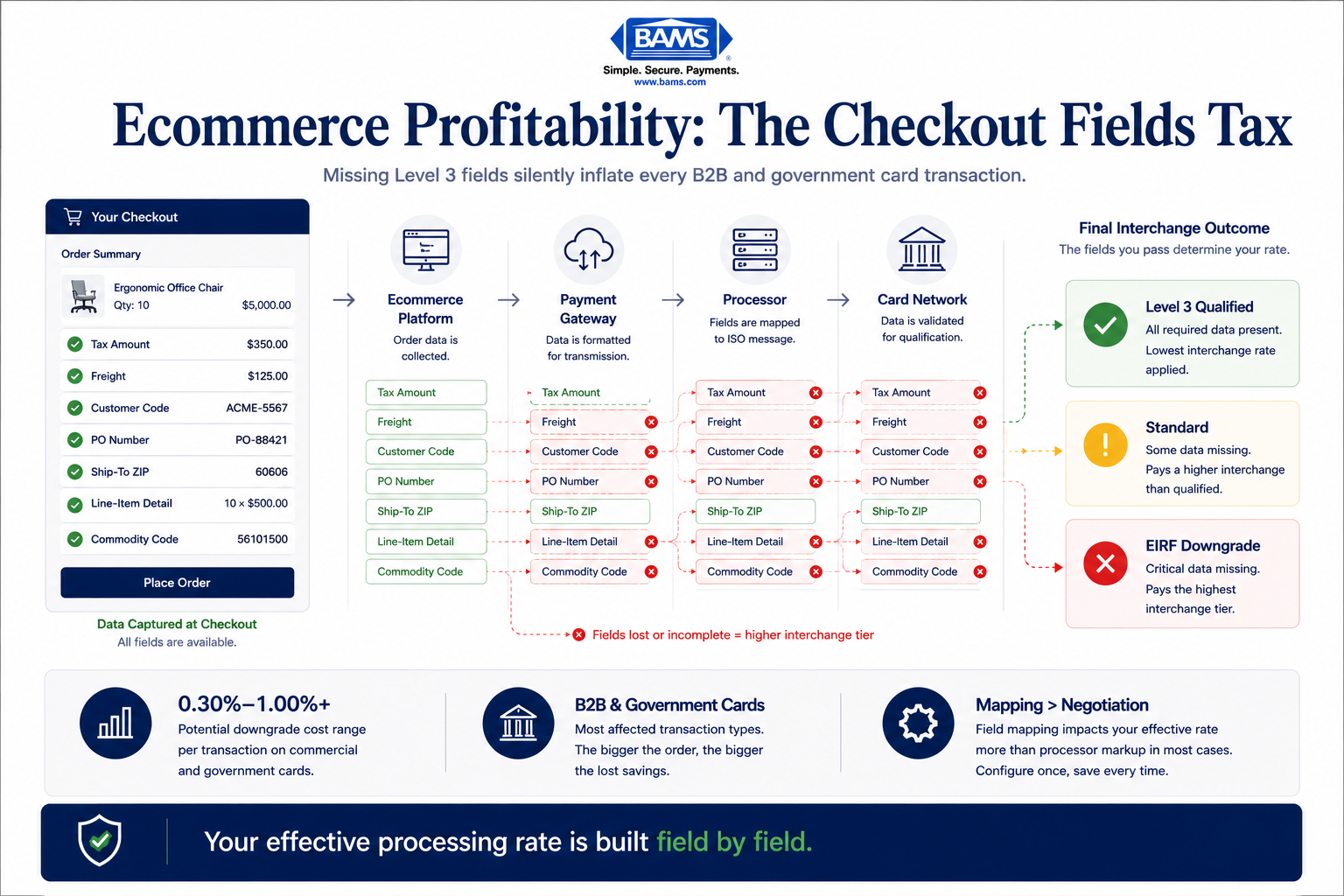

What Level 3 Data Actually Is (and Why Your Checkout Ignores It)

Card networks like Visa and Mastercard define three tiers of transaction data.

- Level 1 is the basics: card number, expiration, transaction amount.

- Level 2 adds tax amount, merchant postal code, and customer code.

- Level 3 goes further, requiring line-item detail: product descriptions, commodity codes, unit costs, quantities, freight amounts, and discount indicators.

When a commercial card transaction includes all three levels, it qualifies for the lowest interchange category. When it doesn’t, the transaction “downgrades” to a more expensive tier. The difference can range from 0.30% to over 1.00% per transaction.

On a $5,000 B2B order, that’s $15 to $50 in unnecessary fees. On 200 such orders a month, you’re looking at $3,000 to $10,000 in annual margin evaporating because your checkout didn’t pass a freight field.

The Field Mapping Problem Nobody Talks About

The real challenge isn’t understanding what Level 3 data is. It’s mapping the right fields from your eCommerce platform to your payment gateway to your processor, and making sure nothing gets dropped along the way.

Consider what has to happen: your platform calculates tax at the line-item level, but does your gateway pass that tax amount as a separate field, or does it bundle it into the total? Your shipping module generates a freight charge, but does it transmit as a distinct data element, or does it just appear as another line item without a commodity code?

Every platform handles this differently. Shopify, WooCommerce, BigCommerce, and Magento all structure order data in their own way. The gateway sitting between your store and your processor may or may not support L3 fields. And even when it does, the mapping between “what your cart calls it” and “what the card network expects” is rarely automatic.

This is why so many eCommerce merchants are bleeding basis points they could recover. The data exists in their systems already. It’s just not reaching the processor in the right format. Federal Reserve interchange fee data continues to demonstrate how qualification differences materially affect merchant processing costs over time.

The difference between qualified and downgraded transactions is often just one missing field.

Where the Money Actually Goes

Let’s be specific. When a government purchasing card transaction downgrades from Level 3 to Level 1, the interchange rate can jump from roughly 1.55% to over 2.65%. On a $10,000 order, that’s the difference between $155 and $265 in interchange alone.

Modern Treasury payment operations resources continue to emphasize how transaction-level visibility and reconciliation workflows directly affect operational efficiency and cost management for merchants handling complex payment flows. If even a fraction of your revenue comes from commercial or government cards, the cumulative downgrade cost is likely one of your largest hidden expenses.

The irony is that merchants will spend weeks negotiating their processor markup down by 0.05%, while ignoring the 0.50% to 1.00% they’re overpaying on interchange because their checkout doesn’t pass a tax field correctly. Common myths about processing fees keep merchants focused on the wrong number entirely.

What Changes When You Treat Payment Processing as a Margin Strategy

If this thesis is right, then the implications go beyond saving a few basis points. It means your checkout configuration is a direct input to your gross margin, not an IT afterthought.

It means the decision about which payment gateway to use isn’t just about uptime and fraud tools. It’s about whether that gateway supports L3 passthrough for your specific platform. It means your payment gateway is costing you more than you think, and not just in deposit delays.

It means that when you evaluate a processor, the first question shouldn’t be “what’s your rate?” It should be “do you support Level 3 qualification, and will you help me map the fields from my platform?” A partner like BAMS, which pairs interchange-plus pricing with dedicated account management, can identify exactly where your transactions are downgrading and help you fix the field mapping to capture lower rates.

And it means that every month you delay this work, you’re compounding a fee that didn’t have to exist.

Rethinking Cost-Effective Payment Solutions

We’d suggest a different mental model for cost-effective payment solutions. Stop thinking of processing fees as a single line item you negotiate once a year. Start thinking of them as a spectrum, where every transaction lands somewhere between “fully optimized” and “maximum cost,” based on the data you pass.

Your effective processing rate isn’t a number your processor gives you. It’s a number you build, transaction by transaction, field by field. Tax amount. Freight charge. Commodity code. Ship-to zip. Each one either qualifies your transaction for a lower tier or lets it slide into a more expensive one.

The merchants who win on processing costs aren’t the ones who negotiate hardest. They’re the ones who configure best.

The Fields Are the Strategy

We’re not going to tell you to go renegotiate your rates. You’ve probably already done that. What we will say is this: look at your checkout data. Trace it from your cart to your gateway to your processor. Find out where the tax field drops off, where the freight amount disappears, where the commodity code never existed in the first place.

That’s where your margin is hiding. Not in a better rate. In better data.

Frequently Asked Questions

How does optimizing transaction data affect processing fees?

Passing detailed line-item data (tax amounts, freight charges, product codes) with commercial card transactions qualifies them for lower interchange tiers set by Visa and Mastercard. Without this data, transactions automatically downgrade to the most expensive rate category, costing merchants 0.30% to over 1.00% more per transaction.

What are the best payment processing strategies to reduce fees on B2B orders?

The highest-impact strategy is ensuring your eCommerce platform passes Level 2 and Level 3 data through your gateway to your processor. Combined with interchange-plus pricing (which passes through actual interchange costs transparently), this approach targets the largest component of your fees rather than just the processor markup.

Which eCommerce platforms support Level 3 data passthrough?

Most major platforms (Shopify, WooCommerce, BigCommerce, Magento) capture the necessary order data, but gateway compatibility and field mapping vary significantly. The key is confirming that your specific gateway and processor combination supports L3 fields and that the mapping between your platform’s data structure and the card network’s requirements is correctly configured.