Same-Day Funding vs Next-Day: Payment Rails Compared

How cut-off times, processing rails, and weekend gaps create deposit delays that marketing claims won’t tell you about

Learn how same-day and next-day funding actually work at the infrastructure level. This comparison breaks down payment rails, cut-off times, and weekend reliability so eCommerce operators can choose based on mechanics, not marketing.

TL;DR

- Next-day funding wins for most eCommerce businesses — It’s cheaper, more predictable, and captures more of your daily transactions thanks to later cut-off times.

- Same-day funding is conditional, not automatic — It depends on your processor’s submission timing, your bank’s rail support, and strict cut-off windows that often exclude evening sales.

- Neither option solves the weekend gap — Saturday and Sunday sales sit until Monday (or Tuesday on holiday weekends) regardless of whether you have same-day or next-day funding.

- The payment rail matters more than the label — Standard batch ACH, Same-Day ACH, and FedNow each have different capabilities, costs, and limitations. Ask your processor which rail they actually use.

- Predictability beats raw speed — Knowing exactly when deposits arrive lets you time inventory purchases, payroll, and ad spend with confidence, which is worth more than shaving a few hours off settlement.

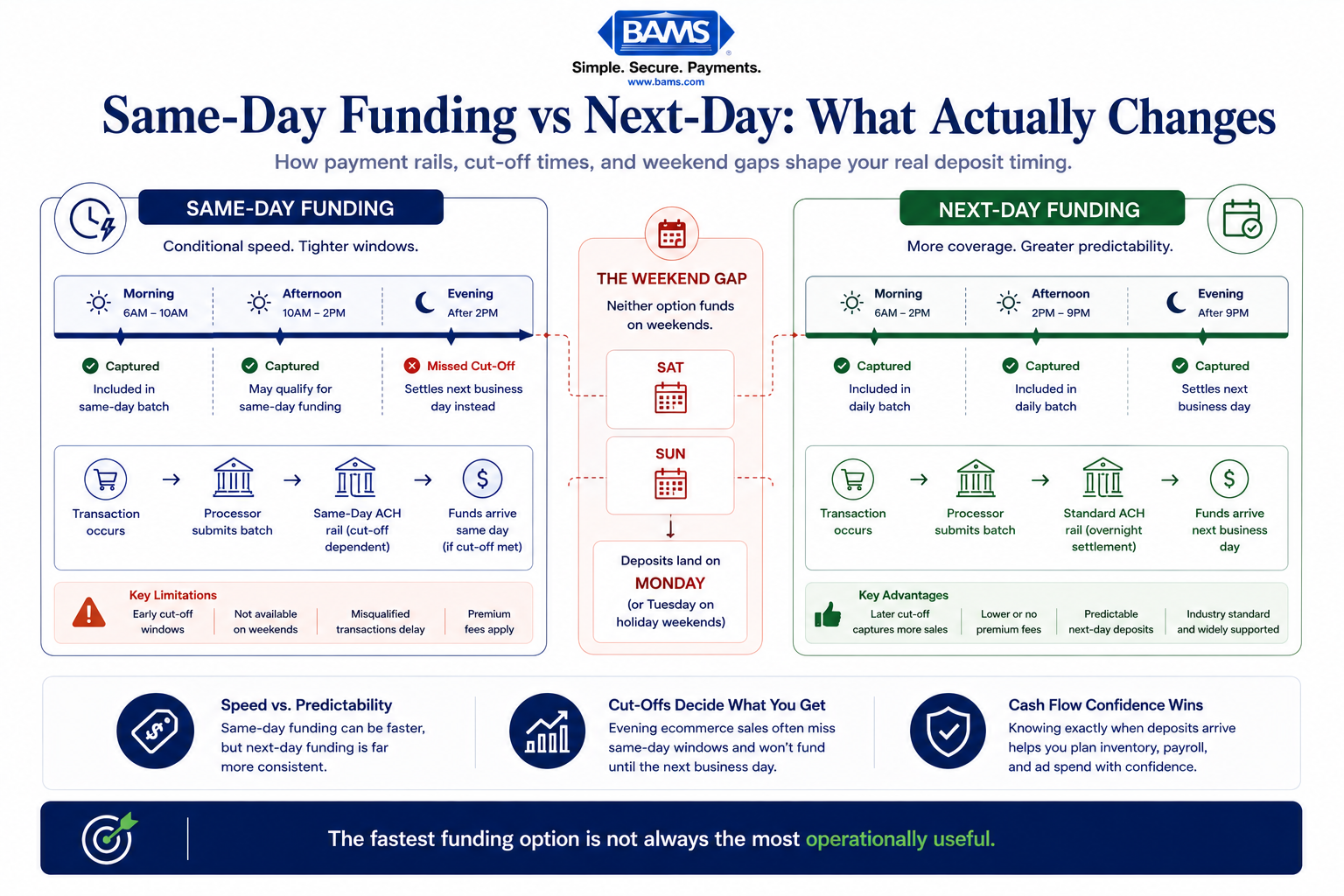

Same-Day vs Next-Day Funding: What Actually Changes for Your Business

The difference between same-day funding and next-day funding looks small on paper. One business day. Maybe 24 hours. But for eCommerce operators managing inventory, payroll, and ad spend, that gap compounds in ways most payment processing marketing materials never explain.

The real question isn’t which option sounds faster. It’s which payment rails your processor actually uses, what cut-off times govern your deposits, and whether the “same-day” promise holds when your biggest sales hit on a Saturday night. This comparison breaks down the mechanics behind both options so you can make a decision based on infrastructure, not branding.

Quick Verdict: Same-Day Funding vs Next-Day Funding

The biggest difference between same-day funding and next-day funding is not speed. It is predictability, cut-off timing, and rail limitations.

Choose same-day funding if your business has urgent, daily cash flow needs (think perishable inventory or same-day fulfillment) and you’re willing to pay premium fees and work within tight submission windows. Choose next-day funding if you want reliable, predictable deposits at a lower cost and your operations can absorb a one-business-day delay. For most eCommerce businesses processing $50K to $500K monthly, next-day funding delivers the better balance of speed, cost, and consistency.

|

Criterion |

Same-Day Funding |

Next-Day Funding |

Winner |

|---|---|---|---|

|

Deposit Speed |

Hours (if cut-off met) |

Next business day |

Same-Day |

|

Cost |

Higher per-transaction fees |

Standard or low fees |

Next-Day |

|

Weekend/Holiday Reliability |

Depends on rail (often fails) |

Predictable next-business-day |

Tie (both limited) |

|

Cut-Off Flexibility |

Strict, early windows |

More generous windows |

Next-Day |

|

Availability |

Limited processors/banks |

Widely available |

Next-Day |

|

Cash Flow Predictability |

Variable |

Consistent |

Next-Day |

The Payment Rails That Actually Determine Your Funding Speed

Before comparing same-day and next-day funding, you need to understand the three settlement systems your deposits travel through. Your processor’s marketing might promise “fast funding,” but the rail they use determines whether that promise survives a holiday weekend.

The funding speed promise depends entirely on which payment rail your processor actually uses.

Standard Batch ACH

This is the default for most merchant accounts. Transactions are batched (usually once per day), submitted to the ACH network, and settled in one to two business days. Weekends and federal holidays pause the clock entirely. If your batch closes Friday evening, funds may not arrive until Tuesday or Wednesday.

Same-Day ACH

Same-Day ACH offers three processing windows per business day, with the latest submission deadline typically around 4:45 PM ET. If your processor submits before a window closes, settlement can happen that same day. But “same day” only applies to business days. Same-Day ACH volume reached 1.3 billion payments in 2024, up from 1.08 billion in 2023, reflecting growing demand for faster settlement. Still, the system doesn’t run on weekends or holidays.

FedNow (Instant Payments)

The Federal Reserve’s FedNow service operates 24/7/365, settling transactions in seconds. By early 2025, more than 1,000 organizations had joined the network, serving over 100 million account holders. However, FedNow adoption among payment processors and merchant banks remains uneven. Your processor may advertise instant capability, but if your receiving bank isn’t on the FedNow network, the promise breaks down at the last mile.

Evaluation Criteria: What Matters for eCommerce Operators

We’re comparing same-day and next-day funding across six dimensions, weighted by what actually affects eCommerce businesses running 10 to 50 employees.

- Deposit speed — How quickly funds hit your account after a sale. Directly affects your ability to reinvest in inventory and advertising.

- Cost per transaction — Faster rails typically cost more. The question is whether the speed premium pays for itself.

- Weekend and holiday behavior — eCommerce sales spike on weekends. How your funding option handles non-business-day transactions matters more than the average case.

- Cut-off time flexibility — A same-day promise with a 10 AM cut-off may be less useful than next-day funding with a 9 PM cut-off.

- Processor and bank availability — Not every processor or bank supports every rail. Availability limits your real options.

- Cash flow predictability — Consistent deposit timing lets you forecast accurately. Variable timing creates operational friction.

Head-to-Head Breakdown: Same-Day Funding vs Next-Day Funding

Deposit Speed

Same-day funding can deliver deposits within hours of batch submission, assuming the transaction clears before one of the Same-Day ACH windows. For processors leveraging FedNow, settlement can happen in seconds, though FedNow transaction volume is still climbing from a relatively small base compared to ACH. The speed is real, but conditional.

Next-day funding deposits land in your account by the following business day, typically by early morning. The timing is slower in absolute terms but far more consistent. You know when the money arrives, which makes planning easier.

Verdict: Same-day wins on raw speed. But speed only matters if you can consistently meet the submission requirements. For most eCommerce operations, next-day deposits arriving predictably by morning are more operationally useful than same-day deposits that sometimes arrive and sometimes don’t.

Cost Per Transaction

Same-day funding typically carries a per-transaction premium. Some processors charge a flat fee per same-day deposit; others add basis points to your effective rate. These costs add up quickly at scale. If you’re processing 500 transactions daily, even a few cents per transaction creates meaningful monthly overhead.

Next-day funding is generally included in standard processing agreements or available at minimal additional cost. Many processors offer it as a baseline feature for qualified merchants, making it a key factor when choosing a payment processor.

Verdict: Next-day funding wins clearly. Unless your business model requires same-day access to cash (perishable goods, same-day delivery logistics), the cost premium of same-day rarely justifies itself for standard eCommerce operations.

Weekend and Holiday Behavior

Same-day funding via Same-Day ACH does not process on weekends or federal holidays. Your Saturday and Sunday sales sit in limbo until Monday’s processing windows open. FedNow technically operates 24/7, but your processor and receiving bank both need to support real-time settlement for this to work. In practice, most merchants still experience weekend gaps.

Next-day funding faces the same limitation. Weekend transactions batch and settle on the next business day (Monday, or Tuesday if Monday is a holiday). The difference is that next-day funding doesn’t promise to eliminate this gap, so there’s no expectation mismatch.

Verdict: Tie. Neither option reliably solves the weekend deposit gap today. This is the single biggest pain point for eCommerce businesses that see 30% to 40% of weekly revenue on Saturday and Sunday. Both options leave you waiting until Monday or Tuesday.

Cut-Off Time Flexibility

Same-day funding requires transactions to be submitted before specific windows. The final Same-Day ACH window closes around 4:45 PM ET. If your processor batches at 3 PM PT, you may miss the window entirely. Late-afternoon and evening sales (which dominate eCommerce) often fall outside same-day eligibility.

Next-day funding typically offers more generous cut-off times, sometimes as late as 9 or 10 PM ET. This means a larger percentage of your daily transactions qualify for next-business-day settlement.

Verdict: Next-day funding wins. The later cut-off captures more of your daily sales volume, especially the evening transactions that make up a significant share of online purchases. A “same-day” option that only covers morning transactions is less useful than it sounds.

Processor and Bank Availability

Same-day funding requires both your processor and your bank to support the faster rail. While Same-Day ACH is broadly available through Nacha’s network, FedNow-based instant settlement is still limited. Your bank may not participate, or your processor may not have integrated the rail yet.

Next-day funding is available from most major processors and works with virtually any business bank account. Qualification requirements exist (transaction history, chargeback ratios, business type), but the infrastructure barrier is low.

Verdict: Next-day funding wins on accessibility. You don’t need to verify that your bank supports a specific rail or worry about integration gaps. It simply works with the existing ACH infrastructure.

Cash Flow Predictability

Same-day funding introduces variability. Did the batch make the cut-off? Is the rail operational today? Did the receiving bank process it in time? Each variable creates uncertainty about when deposits actually land. For businesses that rely on automated reconciliation and cash flow forecasting, this variability creates friction.

Next-day funding delivers deposits on a consistent, predictable schedule. You batch today, money arrives tomorrow morning (business days). This consistency lets you build cash flow management systems around reliable deposit timing.

Verdict: Next-day funding wins. Predictability compounds over time. When you know exactly when money arrives, you can time inventory purchases, payroll runs, and ad spend with confidence.

Use Case Mapping: Which Option Fits Your Business

If you run a standard eCommerce store with steady daily volume, choose next-day funding. The cost savings and predictability outweigh the marginal speed benefit of same-day settlement. Your operations can plan around a one-business-day delay.

If you operate a business with perishable inventory or same-day fulfillment obligations, same-day funding may justify its premium. When you need to purchase fresh inventory daily based on yesterday’s revenue, hours matter.

If you’re scaling rapidly and reinvesting revenue into paid acquisition, next-day funding gives you a reliable daily cash injection to fuel ad spend without the cost overhead of same-day rails. Pair this with a payment gateway optimized for deposit speed to maximize the benefit.

If your business is seasonal with extreme volume spikes (Black Friday, holiday sales), neither option fully solves the weekend and holiday gap. Plan for a 2 to 3 day cash buffer during peak periods regardless of which funding speed you choose.

If you process high volumes of cross-border transactions, be aware that international settlement adds its own delays. Neither same-day nor next-day domestic funding speeds up cross-border settlement, which depends on correspondent banking relationships and currency conversion timing.

What Both Options Get Wrong

Neither same-day nor next-day funding solves the fundamental weekend gap. Ecommerce businesses generate significant revenue on Saturdays and Sundays, and both ACH-based settlement systems pause during non-business days. FedNow could eventually close this gap, but adoption among merchant processors and banks isn’t there yet.

Both options also assume your processor’s internal batching and risk review processes are efficient. A processor that holds transactions for manual review or batches only once daily can add hours or days to your effective settlement time, regardless of which rail they use on the back end.

Migration and Switching Costs

Switching from next-day to same-day funding (or vice versa) within the same processor is usually straightforward. It may require a new agreement or fee schedule, but your integration stays intact. Switching processors entirely is a bigger decision.

Expect 2 to 4 weeks for a full processor migration, including gateway integration, testing, and PCI compliance verification. Data portability varies: transaction history typically stays with your old processor, while recurring billing profiles may need to be re-established. For eCommerce businesses on platforms like Shopify or WooCommerce, the gateway swap process is generally well-documented but still requires careful testing.

The biggest lock-in factor isn’t technical. It’s the qualification process. If you’ve built a strong processing history with low chargebacks, your current processor may offer you better funding terms than a new one would initially provide. Factor this into your switching calculus.

Where BAMS Fits In

For eCommerce businesses that prioritize reliable deposit timing over marginal speed gains, BAMS offers next-day funding as a core feature alongside transparent interchange-plus pricing. Their dedicated account managers can walk you through how your specific setup (platform, gateway, bank) affects your actual settlement timeline, which is the kind of technical clarity most processors don’t provide.

Final Recommendation

For most eCommerce businesses processing between $50K and $500K monthly, next-day funding is the better choice. It’s cheaper, more predictable, more widely available, and captures a larger share of your daily transactions thanks to later cut-off times. The one-business-day delay is a manageable trade-off that pays for itself in lower fees and simpler operations.

Same-day funding makes sense for a narrow set of businesses where daily cash access directly enables revenue (perishable goods, same-day delivery, event-based commerce). If that’s not your model, the premium isn’t worth it today. As FedNow adoption expands and real-time settlement becomes cheaper, this calculus will shift. But right now, the smartest move for most online merchants is reliable next-day deposits paired with a cash buffer strategy for weekends and holidays.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your credit and debit card sales are deposited into your business bank account by the following business day. Your processor batches the day’s transactions, submits them through the ACH network, and funds typically arrive by early morning. Business days exclude weekends and federal holidays, so Friday sales usually arrive Monday.

Why is next-day funding important for small businesses?

Faster access to revenue lets you reinvest in inventory, cover payroll, and fund marketing without relying on credit lines or reserves. For eCommerce businesses with tight margins, the difference between a 1-day and 3-day deposit delay can mean the difference between capturing a restocking opportunity and missing it.

How can a business qualify for next-day funding?

Most processors evaluate your transaction history, chargeback ratio, business type, and monthly processing volume. Businesses with consistent sales patterns, low chargeback rates, and established processing history typically qualify. New businesses or those in high-risk categories may need to build a track record before eligibility.

What are the differences between next-day funding and standard funding?

Standard funding (also called standard batch ACH) typically takes 2 to 3 business days for deposits to arrive. Next-day funding uses the same ACH network but with prioritized submission timing and later cut-off windows, reducing the settlement period to one business day. The fee difference is usually modest.

When should a business consider using same-day funding services?

Same-day funding is most valuable when your business model requires daily cash access to operate. Examples include businesses purchasing perishable inventory daily, same-day delivery services that need to pay drivers immediately, or event-based businesses with short operational windows. If you can plan around a one-day delay, next-day funding is typically more cost-effective.

Does same-day funding work on weekends and holidays?

Same-Day ACH does not process on weekends or federal holidays. FedNow operates 24/7/365 in theory, but both your processor and your receiving bank must support real-time settlement for weekend deposits to actually work. In practice, most merchants still experience a gap between weekend sales and Monday deposits regardless of which funding speed they’ve selected.

Sources