Same-Day Funding vs Next-Day: Impact on eCommerce

How an 18-hour deposit gap reshapes your inventory restocks, ad spend timing, and supplier payments

Learn how same-day funding and next-day funding actually affect eCommerce reinvestment cycles. This comparison breaks down real operational impacts on inventory turns, ad budgets, and scaling decisions.

TL;DR

- Next-day funding is the better choice for most eCommerce businesses – It delivers predictable, fast deposits at lower cost, and your reinvestment decisions rarely hinge on a few extra hours.

- Same-day funding solves a narrow problem – It’s worth the premium only if you deploy capital intraday (perishable inventory, real-time ad scaling, same-day supplier payments).

- Neither option fixes the weekend gap – Friday through Sunday sales typically don’t settle until Monday regardless of your funding speed, so build cash reserves around that reality.

- Your bank matters as much as your processor – Even with same-day or next-day funding from your processor, your bank’s posting schedule can add hours or a full day to actual fund availability.

- Cost compounds quickly – Same-day funding premiums eat into margins over time. With 37% of small firms already relying on external financing, paying extra for funding speed you don’t operationally need adds unnecessary expense.

Same-Day vs Next-Day Funding: What Actually Changes for Your Business

The difference between same-day funding and next-day funding looks trivial on a feature comparison chart. One business day. Maybe 18 hours. But for an eCommerce operator managing inventory turns, ad budgets, and supplier payments, that gap isn’t about convenience. It’s about whether revenue from Monday’s sales can fund Tuesday’s restock or whether you’re floating expenses on a credit line until Wednesday.

This comparison breaks down how each funding speed actually affects your reinvestment cycle, your operational flexibility, and your bottom line. We’re not comparing abstract features. We’re examining what happens to real purchasing decisions, ad campaigns, and supplier relationships when your deposit lands a few hours earlier or later.

If you run an established eCommerce business doing consistent daily volume, the funding speed you choose shapes how aggressively you can scale without borrowing.

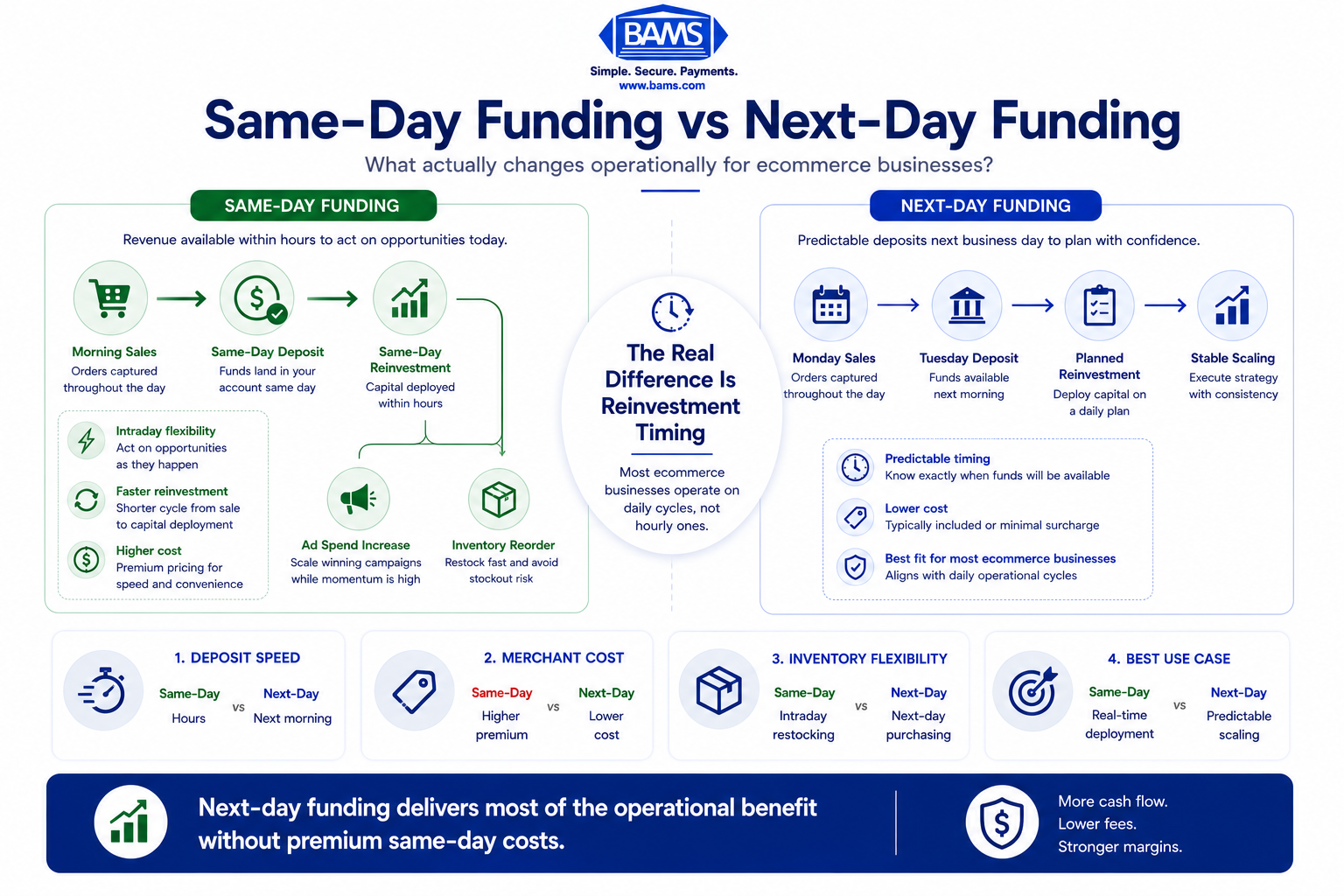

Quick Verdict: Same-Day Funding vs Next-Day Funding

Choose same-day funding if your business depends on intraday cash deployment (perishable inventory, time-sensitive ad arbitrage, or supplier payment windows that close before end of business). Choose next-day funding if you need reliable, fast access to deposits without paying premium fees, and your reinvestment decisions operate on a daily or weekly planning cycle rather than an hourly one.

A strategic comparison of how same-day and next-day funding affect eCommerce reinvestment speed and operational flexibility.

For most eCommerce businesses in the 10-50 employee range, next-day funding delivers 90% of the operational benefit at a fraction of the cost. Same-day funding solves a narrower, more urgent problem.

|

Criterion |

Same-Day Funding |

Next-Day Funding |

Winner |

|---|---|---|---|

|

Deposit Speed |

Funds available within hours |

Funds available next business day |

Same-Day |

|

Cost to Merchant |

Higher per-transaction or flat fees |

Typically included or minimal surcharge |

Next-Day |

|

Inventory Reinvestment Timing |

Enables intraday restocking decisions |

Supports next-morning purchasing |

Same-Day (marginal) |

|

Weekend/Holiday Behavior |

Often paused or delayed on non-banking days |

Often paused or delayed on non-banking days |

Tie |

|

Ad Spend Flexibility |

Can fund campaigns same day as revenue |

One-day lag on reinvestment |

Same-Day |

|

Availability Across Processors |

Limited, often requires specific rails |

Widely available from most merchant services providers |

Next-Day |

|

Predictability & Reliability |

Variable cut-off times, more exceptions |

Consistent, well-understood timelines |

Next-Day |

How We’re Evaluating: The Criteria That Matter for eCommerce

Most comparisons between same-day and next-day funding focus on the clock. We’re focusing on what that clock does to your business decisions. Here are the seven dimensions we’re measuring, weighted by what actually matters to an eCommerce operator managing daily volume.

- Deposit speed: Raw time from transaction batch to available balance. The headline metric.

- Cost to merchant: What you pay (directly or indirectly) for faster access. This includes per-transaction surcharges, monthly fees, and hidden requirements.

- Inventory reinvestment timing: How quickly you can convert today’s revenue into tomorrow’s stock.

- Weekend and holiday behavior: What happens to your deposits during your highest-volume sales periods.

- Ad spend flexibility: Whether your funding speed lets you scale campaigns in sync with revenue.

- Availability and qualification: How easy it is to actually get the funding speed your processor advertises.

- Predictability: Whether the timing is consistent enough to build operational workflows around.

Head-to-Head Breakdown

Deposit Speed

Same-day funding gets your money into your bank account within hours of batch settlement. Depending on the payment rails involved (same-day ACH or, increasingly, the FedNow Service), deposits can arrive in as little as 2-4 hours after your processor submits the batch. This is genuinely fast.

Next-day funding typically delivers deposits by the following business morning. Your processor batches transactions at a daily cut-off (often between 8 PM and 11 PM ET), and the funds arrive before you open for business the next day. For most eCommerce operations, this means revenue from Monday’s sales is available Tuesday morning.

Verdict: Same-day wins on raw speed, but the practical difference is smaller than it appears. If your purchasing and ad decisions happen in the morning, next-day funding already puts cash in your account before you need it. Same-day only creates meaningful advantage when you need to deploy capital within the same business day it was earned.

Cost to Merchant

Same-day funding almost always costs more. Processors that offer it typically charge a per-transaction premium, a flat monthly fee, or both. The underlying payment rails (same-day ACH windows, real-time payment networks) carry higher interchange and network costs, and processors pass those through. Some providers also require higher monthly minimums or reserve requirements to qualify.

Next-day funding, by contrast, has become a competitive baseline in merchant services. Many processors include it at no additional charge, especially for businesses with consistent volume and low chargeback rates. The cost difference between next-day and standard 2-3 day funding is often zero or negligible.

Verdict: Next-day funding wins decisively. The premium you pay for same-day access often exceeds the financial benefit of having funds a few hours earlier, unless your business model depends on intraday capital deployment. For most eCommerce operators, the math doesn’t justify the surcharge.

Inventory Reinvestment Timing

This is where the comparison gets interesting. If you sell physical products, your ability to reorder inventory is directly tied to when revenue hits your account. Same-day funding lets you place supplier orders the same afternoon your sales come in. For businesses managing tight inventory with fast-moving SKUs, this can mean the difference between restocking before a stockout and losing two days of sales.

Next-day funding introduces a one-day lag. Monday’s revenue funds Tuesday’s purchase orders. For most product categories and supplier lead times, this delay is absorbed without issue. But during high-velocity events (flash sales, holiday weekends, viral product moments), that 24-hour gap can compound. You sell out Monday, can’t reorder until Tuesday, and your supplier ships Wednesday.

Verdict: Same-day funding has a marginal edge here, but only for businesses with extremely fast inventory turns and suppliers who can fulfill same-day orders. If your supplier lead time is 3-7 days regardless, getting your deposit 18 hours earlier doesn’t change when product arrives.

Weekend and Holiday Behavior

Here’s the uncomfortable truth neither funding speed fully solves: weekends and bank holidays freeze the pipeline. The U.S. banking system still largely operates on business-day rails. Modern Treasury payment operations resources continue to highlight how banking schedules and settlement timing create operational delays for merchants, especially during weekends and holidays.

For eCommerce businesses, this creates a painful mismatch. Your highest-volume sales days are often Friday through Sunday. But whether you have same-day or next-day funding, Saturday and Sunday deposits typically don’t arrive until Monday (or Tuesday if Monday is a holiday). Both options leave you flying blind over the weekend.

Verdict: Tie. Neither option reliably solves the weekend deposit gap. This is a systemic limitation of current payment infrastructure, not a processor-specific shortcoming. Plan your cash reserves around it.

Ad Spend Flexibility

Paid advertising on platforms like Meta and Google operates on daily budgets. When a campaign is performing, you want to increase spend immediately. With same-day funding, revenue from morning sales can theoretically fund an afternoon budget increase. You’re reinvesting within the same news cycle, the same trend window, the same algorithmic moment.

With next-day funding, you’re always investing yesterday’s revenue into today’s campaigns. For steady-state operations, this works fine. But during a breakout moment (a product goes viral, a competitor runs out of stock), the 24-hour delay means you’re scaling spend one day behind the opportunity curve.

Verdict: Same-day funding offers a real advantage for businesses that actively manage daily ad budgets. If you’re running automated campaigns with fixed weekly budgets, next-day funding provides all the flexibility you need.

Availability and Qualification

Same-day funding is not universally available. Many processors restrict it to businesses with established processing history, low chargeback ratios, and specific banking relationships. Some require you to use a particular bank or payment gateway. The qualification process can take weeks, and approval isn’t guaranteed.

Next-day funding is widely available across the merchant services landscape. Most reputable processors offer it as a standard or easily accessible feature. Qualification typically requires a verified merchant account, reasonable processing history, and compliance with basic risk thresholds. If you’re choosing a payment processor today, next-day funding should be a baseline expectation, not a premium add-on.

Verdict: Next-day funding wins on accessibility. Same-day funding’s qualification barriers make it impractical for many small-to-midsize eCommerce businesses, even those with clean processing histories.

Predictability and Reliability

Consistency matters more than speed for operational planning. If you can reliably predict when deposits land, you can build purchasing schedules, payroll timing, and supplier payment workflows around that rhythm.

Same-day funding introduces more variables. Cut-off times vary by processor and by the underlying rail. A batch submitted at 2 PM might settle by 5 PM, but a batch submitted at 4 PM might not settle until the next morning. The window is tighter and less forgiving. Next-day funding, by contrast, offers a simple promise: batch before the cut-off, get funds tomorrow morning. The rhythm is predictable and easy to operationalize.

Verdict: Next-day funding wins. Predictable cash flow is more valuable than occasionally faster cash flow. You can build systems around a reliable next-morning deposit. You can’t build systems around a variable same-day window.

Use Case Mapping: Which Funding Speed Fits Your Situation

A decision framework for choosing the right funding speed based on inventory, ad spend, and operational needs.

If you manage perishable or ultra-fast-turn inventory (food, trending consumer goods, limited drops), choose same-day funding. The ability to reorder within hours of selling can prevent stockouts that cost more than the funding premium.

If you run a steady eCommerce operation with 3-7 day supplier lead times, choose next-day funding. The extra hours don’t change your reorder timeline, and you save on fees. This is where most established online businesses land.

If you aggressively scale paid ads based on daily performance data, same-day funding gives you a tighter feedback loop between revenue and reinvestment. But only if you’re actively managing budgets daily, not running automated rules.

If you’re growing from $50K to $500K in monthly volume, next-day funding paired with disciplined cash management will serve you better than same-day funding with premium fees eating into your margins.

If your business peaks on weekends, neither option fully solves your problem. Build a cash buffer that covers Friday-through-Monday expenses without relying on weekend deposits.

What Both Options Get Wrong

Neither same-day nor next-day funding addresses the fundamental weekend settlement gap that hits eCommerce businesses hardest. Both options also assume your bank can receive and post funds on the processor’s timeline, which isn’t always true. Your bank’s own posting schedule can add hours or even a full day to the process.

Additionally, neither funding speed helps with cross-border transactions, which often follow entirely different settlement timelines. If a meaningful portion of your revenue comes from international sales, your effective funding speed may be 3-5 days regardless of what your processor advertises. According to the Federal Reserve’s 2025 employer-firm survey, 37% of firms applied for a loan, line of credit, or merchant cash advance in the prior 12 months, a signal that even businesses with “fast” funding still face cash flow gaps that force them into external financing.

Plaid payment infrastructure resources also emphasize that faster payment visibility alone does not eliminate liquidity pressure when settlement timing and banking schedules remain inconsistent across providers.

Migration and Switching Costs

Switching from one funding speed to another (or from one processor to another) isn’t free. If you’re moving processors to get faster funding, expect 1-3 weeks of onboarding, during which your deposits may follow the old processor’s timeline or experience temporary holds. You’ll also need to update your payment gateway integration, which can mean development time if you’re on a custom platform.

Data portability is another consideration. Your transaction history, chargeback records, and customer payment tokens may not transfer cleanly. Some processors make it straightforward; others create friction. Before switching, verify that your new processor supports your eCommerce platform, your current gateway, and your bank’s deposit capabilities.

Lock-in factors are real but often overstated. Most modern merchant services agreements don’t carry early termination fees, but some do. Read the contract. If you’re currently on a processor with 2-3 day standard funding, upgrading to a provider like BAMS that offers next-day funding as a standard feature can meaningfully improve your cash flow without the cost premium of same-day services. Their transparent pricing model also helps you avoid the hidden fees that often accompany “fast funding” marketing from other providers.

Final Recommendation: Same-Day Funding vs Next-Day Funding for Merchant Services

For most established eCommerce businesses, next-day funding is the right choice. It delivers fast, predictable access to your revenue at a lower cost, and it’s widely available without restrictive qualification requirements. You can build reliable operational workflows around it, and the one-day lag rarely affects real purchasing or advertising decisions.

Same-day funding is a specialized tool. It solves a real problem for businesses with intraday capital needs, but those businesses are the exception, not the rule. If you’re not sure you need it, you almost certainly don’t.

The highest-leverage move for most eCommerce operators isn’t chasing the fastest possible deposit. It’s ensuring your processor delivers consistent next-day funding, transparent fees, and support that actually helps you optimize your settlement workflow. Start there, and upgrade to same-day only when your reinvestment cycle genuinely demands it.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your processor deposits the previous day’s credit card transactions into your bank account by the next business morning. You batch your transactions before a daily cut-off time (usually between 8 PM and 11 PM ET), and the funds are available when you start business the following day. It’s the fastest widely available funding option that doesn’t carry premium surcharges.

How can a business qualify for next-day funding?

Most processors require a verified merchant account, a consistent processing history, and a chargeback ratio below their risk threshold (typically under 1%). Some processors also require your bank to support same-day ACH deposits. If you have a clean processing record and a compatible bank account, qualification is usually straightforward. Check with your processor about specific cut-off times and any volume requirements.

What are the differences between next-day funding and standard funding?

Standard funding typically delivers deposits in 2-3 business days after batch settlement. Next-day funding compresses that to one business day. The practical difference is significant for cash flow management: with standard funding, Monday’s sales don’t arrive until Wednesday or Thursday. With next-day funding, they arrive Tuesday morning. This lets you make purchasing and budgeting decisions with more current revenue data.

When should a business consider using same-day funding services?

Consider same-day funding if your business requires intraday capital deployment. This includes businesses with perishable inventory that must be reordered within hours, operations that scale paid advertising budgets based on real-time sales data, or businesses with supplier payment windows that close before end of business. If your restocking and reinvestment decisions happen on a daily or weekly cycle, next-day funding typically provides sufficient speed.

Which factors affect the approval for next-day funding?

The primary factors are your chargeback ratio, monthly processing volume, business type (industry risk category), time in business, and your bank’s ability to receive accelerated deposits. High-risk industries (travel, digital goods, subscription services) may face additional scrutiny. Processors also evaluate your average transaction size, since higher-ticket businesses carry more settlement risk.

Do same-day and next-day funding work on weekends?

In most cases, no. Both funding speeds are tied to banking system hours, and the majority of U.S. banks don’t process merchant deposits on Saturdays, Sundays, or federal holidays. This means Friday, Saturday, and Sunday transactions typically settle on Monday (or Tuesday if Monday is a holiday). The FedNow Service operates 24/7, but most processors haven’t fully integrated it for merchant settlements yet. Plan your weekend cash needs accordingly.

Sources