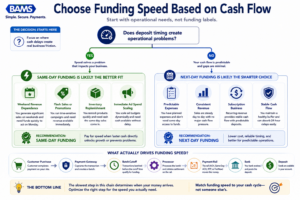

Same-Day vs Next-Day Funding: What Changes

How payment rails, batch timing, and bank participation determine when money actually hits your account

Learn how same-day and next-day funding work at the infrastructure level — not the marketing level. This comparison breaks down deposit speed, cost, and cash cycle impact so you can choose the option that fits your real business needs.

TL;DR

- Same-day funding is faster but conditional — It only works as advertised when your processor uses a real-time rail (RTP or FedNow) and your bank participates in that network. Otherwise, you’re paying extra for marginal speed gains.

- Next-day funding wins for most eCommerce businesses — Later batch cutoffs capture more daily revenue, costs are lower, and the predictable deposit schedule makes cash flow planning straightforward.

- Batch cutoff times matter more than the funding label — Same-day funding often requires batching by 10 a.m., which means evening sales (your peak hours) miss the window entirely.

- Weekend deposits depend on the rail, not the marketing — Same-day ACH doesn’t run on weekends. Only RTP and FedNow operate 24/7, so ask your processor which rail they actually use.

- Match funding speed to your cash cycle — Don’t chase the fastest option by default. Evaluate where cash gaps actually hurt your business, then pick the funding speed that solves that specific problem.

Same-Day vs Next-Day Funding: What Actually Changes for Your Business

The difference between same-day funding and next-day funding sounds simple: one is faster. But when you dig into how money actually moves from a customer’s card to your bank account, the picture gets more complicated. The speed of your deposits depends on payment rails, batch timing, bank participation, and transaction windows that most processors never explain.

If you manage payments for an established eCommerce business, you’ve probably seen “fast funding” marketed as a feature. What you haven’t seen is a clear breakdown of the infrastructure behind that promise. This comparison strips away the marketing language and examines what each funding speed actually delivers for your cash cycle, your operations, and your bottom line.

The path your money takes matters more than the funding label attached to it

Quick Verdict: Same-Day Funding vs Next-Day Funding

Choose same-day funding if your business runs on thin cash margins, processes high weekend volume, or needs to reinvest revenue into inventory the same day it comes in. The speed premium is worth it when cash gaps directly threaten operations.

Choose next-day funding if you want reliable, predictable deposits without paying extra per transaction. For most eCommerce operators processing steady daily volume, next-day funding delivers the speed you actually need at a lower cost.

|

Criterion |

Same-Day Funding |

Next-Day Funding |

Winner |

|---|---|---|---|

|

Deposit Speed |

4–12 hours (varies by rail) |

Next business day |

Same-Day |

|

Cost per Transaction |

Higher (premium fees typical) |

Lower or included |

Next-Day |

|

Weekend/Holiday Handling |

Depends on rail (RTP works 24/7; ACH does not) |

Deposits skip to next business day |

Same-Day (if on RTP) |

|

Batch Timing Flexibility |

Strict early cutoffs (often 10 a.m.) |

Later cutoffs (often 10 p.m.) |

Next-Day |

|

Bank Compatibility |

Requires receiving bank on compatible rail |

Works with nearly all banks |

Next-Day |

|

Predictability |

Variable (rail, timing, bank posting) |

Consistent daily rhythm |

Next-Day |

|

Best for Cash-Sensitive Ops |

Restaurants, pop-ups, inventory-heavy retail |

Steady eCommerce, subscription models |

Tie (context-dependent) |

Evaluation Criteria: What Actually Matters for Payment Processing Speed

Funding speed comparisons fall apart when they treat “fast” as a single metric. Here are the dimensions that actually determine whether same-day or next-day funding works better for your business.

- Deposit speed — How many hours from batch close to cash in your account. This is the headline number, but it’s shaped by everything below.

- Cost — Premium fees, per-transaction charges, or monthly add-ons that come with faster funding.

- Weekend and holiday behavior — Whether your Saturday and Sunday sales sit idle until Monday or move on real-time rails.

- Batch cutoff timing — The deadline that determines whether today’s sales land today or tomorrow. This is where most merchants lose hours without realizing it.

- Bank compatibility — Your receiving bank must support the rail your processor uses. If it doesn’t, “same-day” becomes “next-day” anyway.

- Predictability — Consistency matters for cash flow forecasting. Erratic deposit timing creates more problems than slightly slower deposits.

Head-to-Head Breakdown

Deposit Speed: The Headline Difference

Same-day funding can deliver deposits in as few as 4 to 8 hours after batch close. Some processors use debit-card-linked payouts that claim under 5 hours. But the actual speed depends on which payment rail your processor uses. If it’s same-day ACH, you’re still working within Nacha’s processing windows. If it’s the RTP network (now with over 1,053 participating financial institutions), transfers can settle in seconds.

Next-day funding typically means your batch closes in the evening and deposits arrive the following business morning. The ACH Network remains the primary infrastructure supporting most next-day deposit programs, making ACH processing windows and bank posting schedules important factors in actual funding speed. The gap is roughly 12 to 18 hours. That’s slower than same-day, but it’s also more consistent. You know when the money lands.

Verdict: Same-day wins on raw speed, but only when the underlying rail and your bank both cooperate. If your bank isn’t on a real-time network, the gap between same-day and next-day shrinks to a few hours.

Cost: What You Pay for Speed

Same-day funding almost always carries a premium. This can take the form of a per-transaction surcharge, a higher processing rate, or a flat monthly fee. For high-volume eCommerce operations, those fractions of a percent compound quickly across thousands of transactions.

Next-day funding is frequently included in standard merchant account pricing, especially with processors that prioritize it as a core feature rather than an upsell. The cost difference between next-day and standard 2–3 day funding is often zero or minimal.

Verdict: Next-day funding wins on cost. Unless same-day speed directly prevents a cash shortfall that would cost you more (missed inventory buys, late vendor payments), the premium rarely pays for itself in a typical eCommerce operation.

Weekend and Holiday Behavior: The Hidden Variable

Same-day funding on RTP or FedNow can process on weekends and holidays because these rails operate 24/7/365. FedNow reached over 1,400 participating organizations and processed more than 1 million transactions in December 2024 alone, showing rapid adoption. But same-day ACH does not run on weekends. If your processor uses ACH for “same-day” payouts, Saturday sales don’t move until Monday.

Next-day funding skips weekends and holidays entirely. Friday evening batches arrive Monday morning. For eCommerce businesses with weekend sales surges, this creates a predictable but sometimes painful two-day gap.

Verdict: Same-day funding wins here, but only if your processor actually uses a real-time rail (RTP or FedNow) rather than same-day ACH. Ask your processor which rail they use. The answer determines whether “same-day” means anything on a Saturday.

Batch Cutoff Timing: Where Merchants Lose Hours

This is the criterion most merchants overlook. Same-day funding typically requires batches to close early, often by 10 a.m. or earlier. If your heaviest sales window is afternoon or evening (common in eCommerce), those transactions miss the same-day cutoff and roll into the next cycle. You’re paying for same-day speed but only getting it on a portion of your volume.

Next-day funding batches commonly close at 10 p.m. or later. That captures a full day of sales in one batch. The result: a higher percentage of your daily revenue arrives in a single, predictable deposit.

Verdict: Next-day funding wins for eCommerce businesses with sales spread throughout the day. Same-day cutoffs are too early to capture peak online shopping hours, which means the “same-day” label applies to less of your revenue than you’d expect.

Bank Compatibility: The Bottleneck Nobody Mentions

Same-day funding requires your receiving bank to participate in whatever rail your processor uses. Real-time payment networks only deliver their full speed advantage when both the sending and receiving institutions support the rail being used. If your bank isn’t on RTP or FedNow, the transfer defaults to slower settlement methods regardless of what your processor promises.

Next-day funding works through standard ACH and card settlement networks that virtually every U.S. bank supports. There’s no compatibility question. Your deposits arrive on schedule.

Verdict: Next-day funding wins on universality. Before signing up for same-day funding, confirm your bank participates in the specific rail your processor uses. Otherwise, you’re paying a premium for a speed boost that never reaches your account.

Predictability: What Your Cash Flow Model Needs

Same-day funding introduces variability. Deposits can arrive at different times depending on when you batch, which rail is used, and how quickly your bank posts. This makes cash flow forecasting harder because you’re working with a moving target rather than a fixed schedule.

Next-day funding creates a rhythm. Sales from Tuesday arrive Wednesday morning. Every day follows the same pattern (with weekends as the known exception). For eCommerce operators managing payroll, ad spend, and inventory purchasing on tight timelines, this consistency is operationally valuable.

Verdict: Next-day funding wins for businesses that prioritize planning over raw speed. Predictable cash arrival lets you automate payments, schedule vendor orders, and manage working capital with confidence.

Use Case Mapping: Which Funding Speed Fits Your Business

The right funding speed depends on where cash delays actually create business friction.

If you run a high-volume eCommerce store with steady daily sales, choose next-day funding. The late batch cutoffs capture more of your revenue, and the consistent deposit schedule simplifies your financial operations. Processors like BAMS offer next-day funding as a standard feature, which means you get speed without paying a per-transaction premium.

If you operate a restaurant or retail location with high weekend foot traffic, choose same-day funding on a real-time rail. Weekend sales sitting idle until Monday can create genuine cash gaps, especially if you’re restocking inventory on Monday morning.

If you run flash sales or seasonal promotions with unpredictable volume spikes, same-day funding helps you reinvest revenue immediately. During a Black Friday surge, getting deposits within hours lets you restock or scale ad spend in real time.

If you’re a subscription-based eCommerce business with predictable recurring revenue, next-day funding is the clear choice. Your revenue is already predictable. Paying extra for same-day speed adds cost without solving a real problem.

If you process cross-border transactions, neither option fully solves the delay. International settlement involves additional intermediaries, currency conversion, and compliance checks that add time regardless of domestic funding speed.

What Both Funding Speeds Get Wrong

Neither same-day nor next-day funding addresses the full settlement pipeline. Both still depend on batch processing rather than continuous, transaction-level settlement. Your individual 2 p.m. sale doesn’t move independently; it waits in a batch with every other transaction until the cutoff.

Both also leave merchants with limited visibility into where their money is at any given moment. The gap between “transaction approved” and “funds deposited” remains a black box for most businesses. Until processors offer real-time deposit tracking (the way shipping carriers track packages), merchants are left estimating rather than knowing.

Migration and Switching Costs

Switching from standard 2–3 day funding to next-day funding is usually straightforward. Most processors that offer it require a brief underwriting review and may ask for a few months of processing history. There’s minimal technical integration work if you’re staying on the same eCommerce payment setup.

Switching to same-day funding can involve more friction. You may need to change your batch schedule, verify your bank’s rail compatibility, and adjust your accounting workflows to handle deposits arriving at variable times. Some processors also require higher monthly minimums or longer contract terms for same-day access.

If you’re switching processors entirely, factor in gateway migration, PCI compliance re-certification, and the 1–2 week transition period where deposit timing may be unpredictable. The switching cost is real but manageable. The bigger risk is lock-in: some processors bundle same-day funding into contracts with early termination fees, making it expensive to leave if the speed doesn’t deliver the value you expected.

Final Recommendation: Same-Day Funding vs Next-Day Funding

For most established eCommerce businesses, next-day funding is the better choice. It captures a full day of sales with later batch cutoffs, works with virtually every bank, costs less, and creates the predictable deposit rhythm your cash flow model needs. The few hours you “lose” compared to same-day funding rarely justify the premium.

Same-day funding earns its place in businesses where cash gaps are acute and immediate: restaurants restocking after a weekend rush, retailers running flash sales, or any operation where a 12-hour delay creates a real operational problem. Before committing, verify that your processor uses a true real-time rail (RTP or FedNow) and that your bank participates. Without both, you’re paying for a label, not a result.

The smartest move isn’t chasing the fastest possible deposit. It’s understanding your actual cash cycle and matching your funding speed to it. Start there, and the right choice becomes obvious.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your processor batches the day’s transactions (typically by a 10 p.m. cutoff) and deposits the funds into your bank account the following business day. It’s faster than the standard 2–3 day settlement most processors offer, and it usually works through standard ACH or card settlement networks that nearly every bank supports.

Why is next-day funding important for small businesses?

Faster access to revenue means you can pay vendors, restock inventory, and cover payroll without relying on credit lines to bridge cash gaps. For small businesses operating on tight margins, reducing the float period from 3 days to 1 day can free up meaningful working capital every month.

How can a business qualify for next-day funding?

Most processors require a brief underwriting review that looks at your processing history, chargeback ratio, and business type. Established businesses with consistent volume and low chargeback rates typically qualify without difficulty. Some processors may require a minimum monthly processing volume.

What’s the difference between same-day ACH and real-time payments (RTP)?

Same-day ACH processes payments in batches during set windows on business days only. RTP, operated by The Clearing House, settles individual transactions in seconds, 24/7/365. When a processor offers “same-day funding,” the rail they use determines whether deposits actually arrive the same day or follow ACH’s limited schedule.

Do same-day deposits work on weekends?

Only if your processor uses a real-time rail like RTP or FedNow and your bank participates in that network. Same-day ACH does not process on weekends or federal holidays, so Saturday and Sunday transactions would roll to Monday regardless of the “same-day” label.

Which factors affect how quickly deposits actually arrive?

Four main factors: the payment rail your processor uses (ACH, RTP, FedNow, or debit-card payout), your batch cutoff time, whether your receiving bank participates in the chosen rail, and when your bank posts incoming transfers. The same funding product can produce different results across different banks and transaction windows.

Sources