Faster Payment Settlement: Why It Beats Low Rates

Mid-market eCommerce businesses lose more chasing cheap rates than they save — settlement speed and qualification drive real cost.

Learn why headline processing rates mislead B2B eCommerce teams and how faster payment settlement and Level 3 qualification rates determine what actually hits your bank account. A framework for evaluating processors on cash flow, not basis points.

TL;DR

- Headline rates mislead – Your effective processing rate, driven by interchange qualification and hidden fees, matters far more than the markup a processor advertises.

- Level 3 data qualification is the biggest savings lever – Properly submitting enhanced transaction data on B2B orders can save 30-40 basis points per transaction, often worth $9,000-$12,000+ annually on mid-market volume.

- Faster payment settlement reduces real costs – Next-day funding eliminates carrying costs, credit line draws, and missed vendor discounts that slow settlement quietly creates.

- Evaluate processors on yield, not rate – Your true cost is what lands in your bank account, when it arrives, and how much friction it took to get there. The lowest quoted rate often delivers the worst yield.

The Cheapest Rate on the Table Might Be the Most Expensive Decision You Make

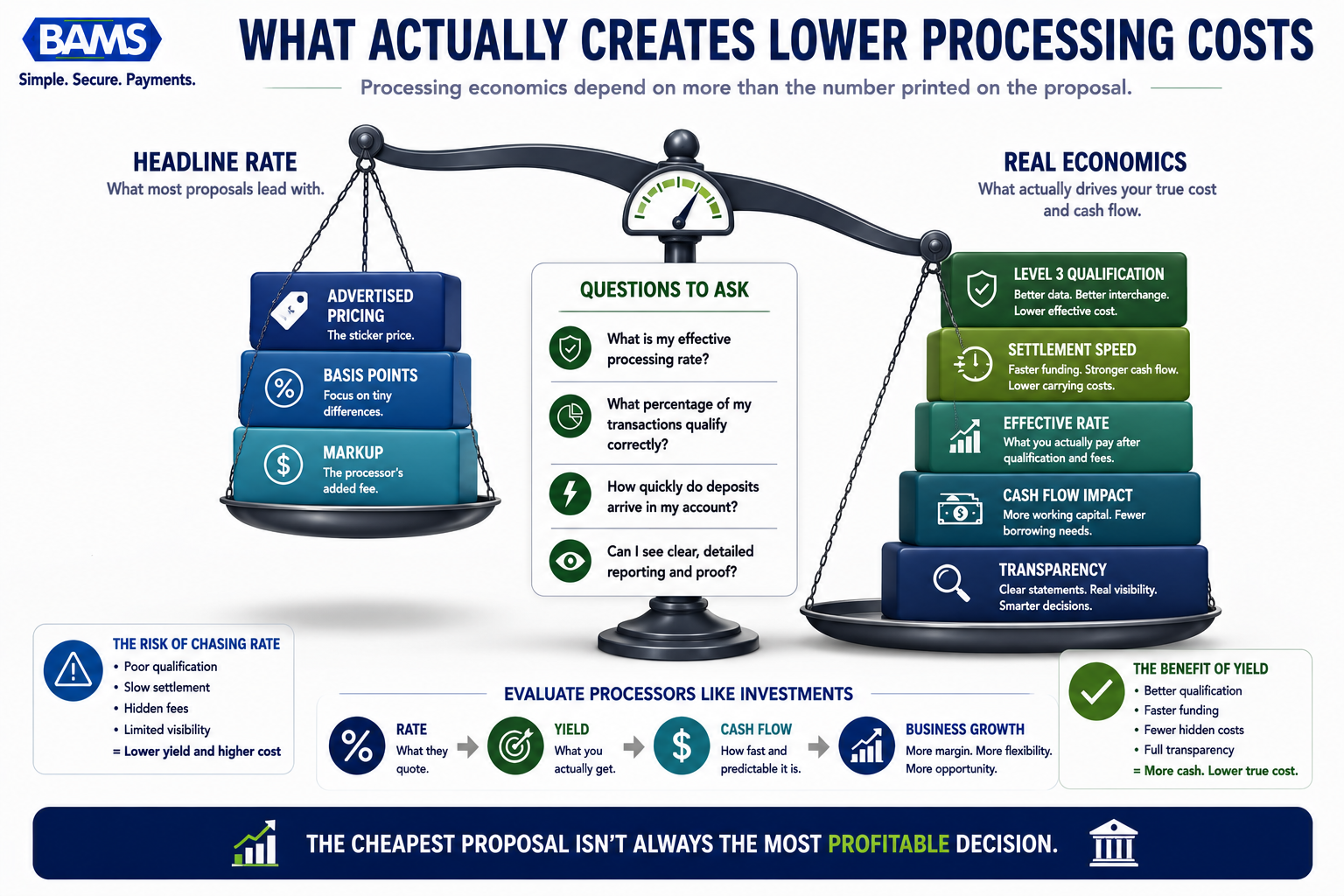

Every eCommerce manager with a $2M+ B2B book has received the pitch: “We’ll beat your rate.” It sounds like a gift. It feels like progress. But chasing low cost merchant services based on headline rates is costing mid-market eCommerce businesses far more than the credit card processing fees they’re trying to escape. The real cost isn’t printed on the rate sheet. It’s hiding in the gap between what you were promised and what actually hits your bank account.

Why “Lowest Rate Wins” Became the Default

It makes intuitive sense. Processing fees are a line item. A lower percentage means lower costs. For years, that logic held up well enough, especially when most transactions were simple consumer card swipes with predictable interchange categories.

The payments industry leaned into this. Processors competed on basis points. Comparison sites ranked providers by advertised rates. Merchants learned to shop by spreadsheet, stacking proposals side by side and picking the smallest number. And for straightforward retail, it worked. Or at least, it didn’t visibly fail.

But B2B eCommerce isn’t straightforward retail. Your average order values are higher and your card-not-present mix is larger. Your interchange categories are more complex. And the gap between what a processor quotes and what you actually pay widens dramatically when qualification and settlement timing enter the picture.

The Metric That Actually Determines Your Cost

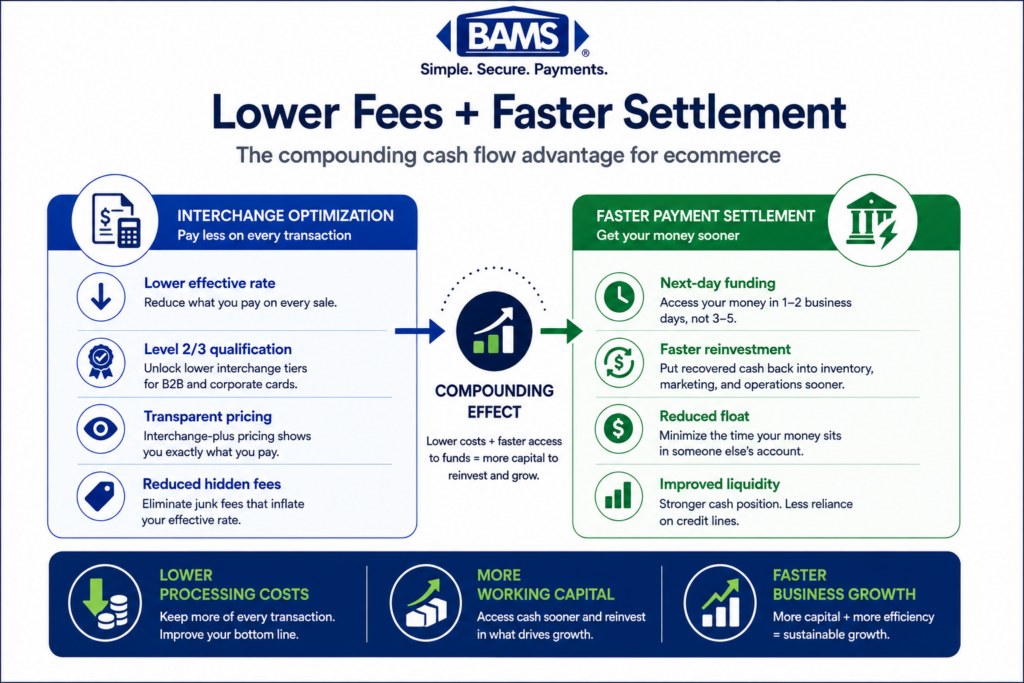

Here’s what we believe: for mid-market eCommerce operations running B2B volume, your effective processing rate and your settlement speed matter more than any quoted rate. Full stop. The businesses saving the most on processing aren’t the ones who negotiated the lowest markup. They’re the ones whose transactions consistently qualify at the best interchange tiers and whose cash hits their account the next business day.

Credit Card Processing Fees Are Decided Before Your Processor Touches Them

Let’s unpack this, because the mechanics matter.

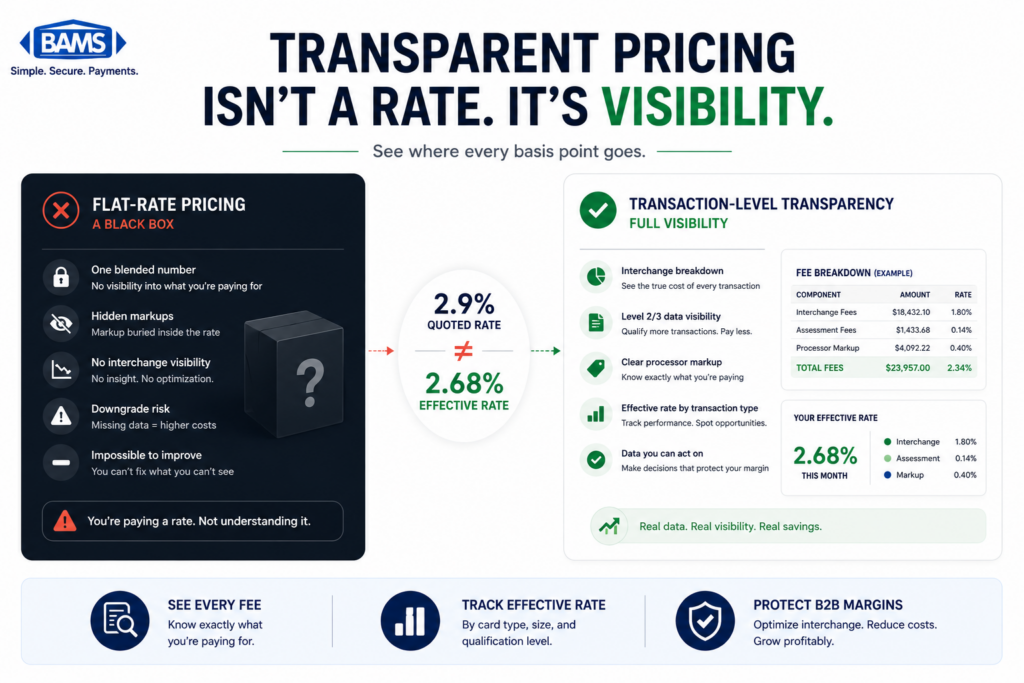

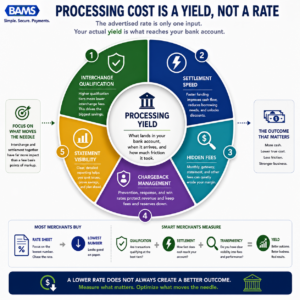

Interchange fees, set by Visa and Mastercard, account for roughly 70-80% of what you pay per transaction. Your processor’s markup sits on top. So even if a processor offers you a razor-thin markup, the interchange tier your transaction lands in determines the bulk of your cost.

This is where Level 2 and Level 3 data qualification becomes the most underleveraged savings tool in B2B eCommerce. When you submit enhanced transaction data (purchase order numbers, item-level detail, tax amounts, ship-to addresses), card networks reward you with lower interchange rates. The savings on properly qualified Level 3 transactions can reach 30-40 basis points per transaction compared to a standard Level 1 submission.

That’s not a rounding error. On $3M in annual B2B card volume, the difference between Level 1 and Level 3 qualification can exceed $9,000 to $12,000 per year. And most mid-market merchants have no idea what percentage of their transactions are actually qualifying.

We’ve seen this pattern repeatedly: a business signs with a processor advertising interchange-plus pricing at a competitive markup, assumes they’re getting the best deal, and never checks whether their transactions are actually hitting Level 3. Their processing statements quietly leak margin month after month.

The Cash Flow Dimension Nobody Quotes

Now layer in settlement timing. Most processors batch and fund in two to three business days. Some stretch to four or five. That delay has a real cost, and it compounds in ways that don’t show up on a rate comparison.

When your deposits lag, you carry more working capital. You draw on credit lines and you delay vendor payments or miss early-pay discounts. You make inventory decisions with incomplete cash positions. 86% of U.S. businesses used faster or instant payments in 2023, and the reason isn’t trend-chasing. It’s because faster payment settlement directly reduces the operational drag that slow funding creates.

Research from the Bank for International Settlements confirms that fast payment adoption accelerates when systems offer broader use cases and participation. For B2B eCommerce, the use case is clear: 92% of businesses rank B2B payments as the most valuable instant-payment application.

The market is telling us that speed isn’t a luxury. It’s infrastructure.

A processor offering next-day funding at a slightly higher markup can deliver better net economics than one offering a lower rate with three-day settlement, once you factor in the carrying cost of that cash gap. This is the math that rate-first evaluations miss entirely. Many businesses continue to identify cash flow management and operating expenses as significant challenges. According to the Federal Reserve’s 2025 Small Business Credit Survey, improving cash availability and working capital visibility remains an important operational priority for many firms.

This is exactly where a partner like BAMS changes the equation. Their next-day funding and transparent interchange-plus pricing let eCommerce operations see the real cost per transaction while getting cash into their accounts a full one to two days faster than the industry norm. Combined with dedicated account management that actively monitors Level 2/3 qualification rates, the result is a lower effective processing rate and better cash flow, not one or the other.

What Changes If Qualification and Speed Are the Real Levers

Processing economics depend on more than the number printed on the proposal.

If this framing is right, then most mid-market eCommerce businesses are optimizing the wrong variable. They’re spending cycles negotiating basis points on markup when the real savings sit in interchange qualification and settlement velocity.

It means your next processor conversation should start with two questions: “What percentage of my B2B transactions are qualifying at Level 3?” and “What is my actual effective processing rate after all fees?” If your current provider can’t answer both clearly, that silence is itself a cost.

It also means that the hidden fees draining your margins aren’t always labeled as fees. They’re the interchange downgrades you never noticed, the settlement delays you absorbed, and the qualification gaps nobody flagged. The most expensive processor isn’t the one with the highest rate. It’s the one that doesn’t tell you what you’re actually paying.

A Better Way to Think About Processing Cost

The advertised rate is only one input. Your actual yield is what reaches your bank account.

Stop evaluating processors like you’re buying a commodity. You’re not shopping for the cheapest pipe. You’re choosing the system that determines how fast your revenue converts to usable cash and how much of each transaction you actually keep.

Think of it this way: your processing cost isn’t a rate. It’s a yield. The rate is one input. Qualification tier is another. Settlement speed is a third. Hidden fees, chargeback handling, and reconciliation complexity are the rest. Your yield is what lands in your bank account, when it lands, and how much work it took to get there.

When you evaluate processors through a yield lens, the “lowest rate” option often finishes last.

The Rate Sheet Is a Distraction

Mid-market eCommerce businesses don’t fail because they chose a processor with a 15 basis point higher markup. They bleed margin because nobody told them their B2B transactions were downgrading to Level 1, because their cash sat in limbo for 72 hours, and because they spent hours reconciling statements that were designed to be hard to read.

The businesses that win on processing aren’t the ones with the best rate. They’re the ones who know their yield.

Frequently Asked Questions

What is interchange-plus pricing and how does it work?

Interchange-plus pricing separates the card network’s base cost (interchange) from your processor’s markup, so you see exactly what you’re paying and to whom. It’s the most transparent pricing model for mid-market eCommerce because it exposes whether your transactions are qualifying at optimal interchange tiers.

Why should B2B eCommerce businesses care about Level 2/3 data optimization?

Level 2 and Level 3 data submission can lower your interchange rate by 30-40 basis points per transaction on qualifying B2B orders. Most processors don’t proactively optimize for this, which means you could be overpaying on every corporate card transaction without knowing it.

What are the most common hidden fees in merchant services?

Beyond obvious surcharges, the costliest hidden fees are interchange downgrades from poor data qualification, batch fees, PCI non-compliance charges, and inflated chargeback handling costs. Reviewing your effective processing rate (total fees divided by total volume) is the fastest way to spot them.