Volume-Based Pricing Tiers Won’t Save You

Why eCommerce teams that chase lower rates keep losing margin — and what system-level visibility actually fixes

Learn why negotiating better processing rates rarely reduces total costs, and how automated reconciliation and transparent pricing models give eCommerce teams control over what they actually pay per transaction.

TL;DR

- The problem isn’t your rate – It’s the gap between your quoted rate and your effective rate, inflated by interchange downgrades, unapplied volume-based pricing tiers, and hidden fees you never audit.

- Reconciliation is infrastructure, not a task – 61% of finance teams still reconcile manually, which means discrepancies compound undetected for months. Automated reconciliation catches what humans structurally cannot.

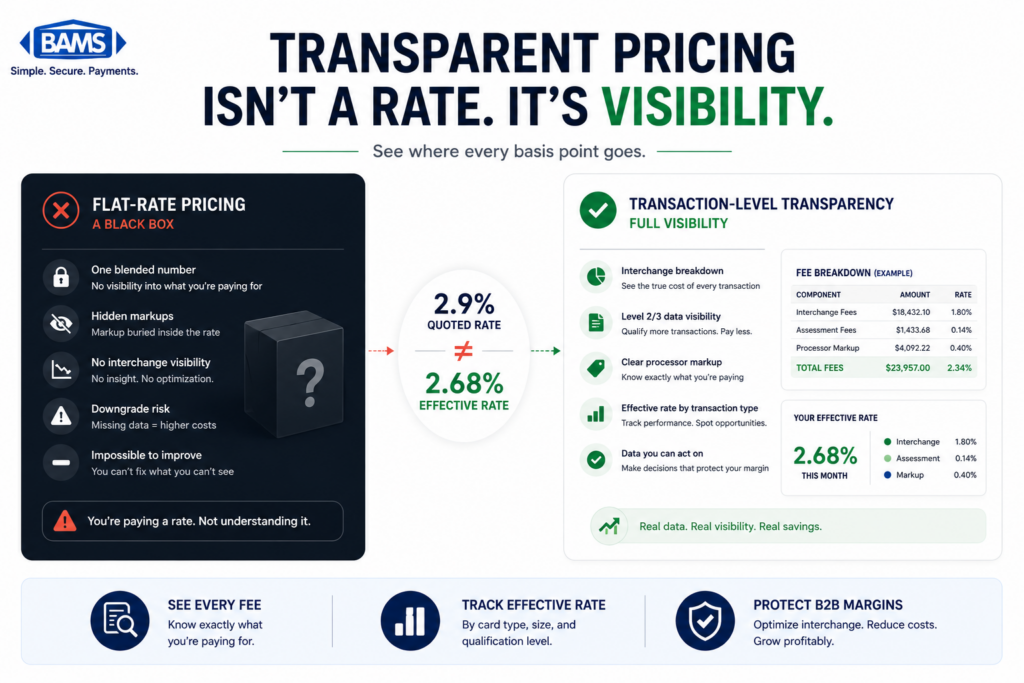

- A transparent pricing model beats a low rate – A fair rate with full visibility will always cost less over time than a low rate with opaque billing. Treat pricing like plumbing: inspect the system, not just the price tag.

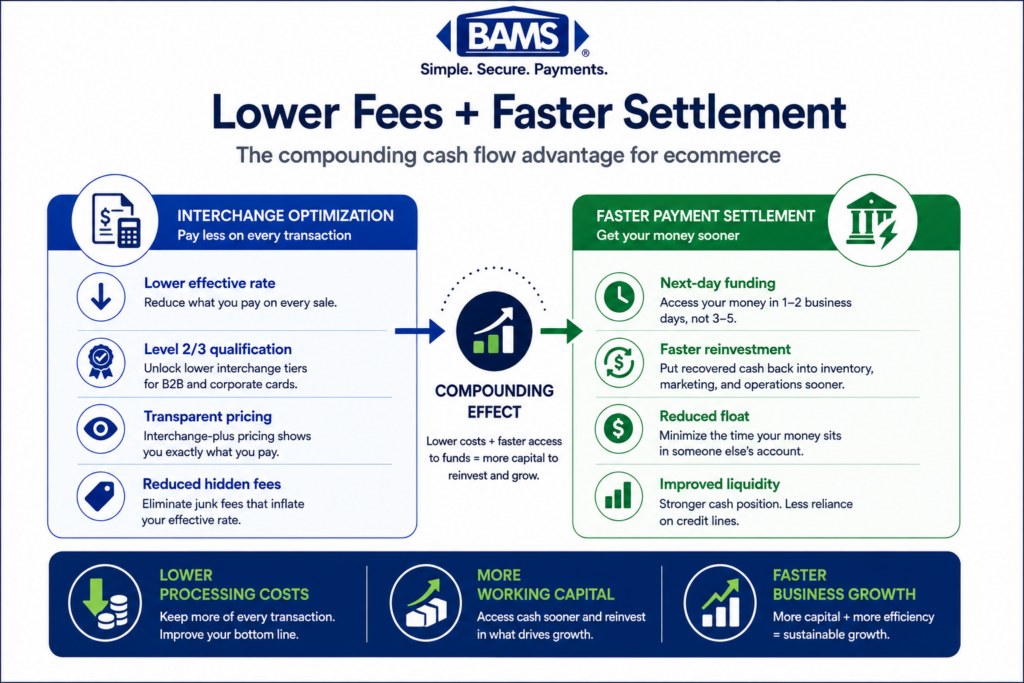

- Level 2/3 data qualification is where real savings hide – If your processor claims to support it but you’re not verifying qualification rates per transaction, you’re likely overpaying on every B2B order.

You Already Negotiated a Better Rate. So Why Are Your Costs Still Climbing?

Every eCommerce manager has been there. You spend weeks comparing processors, negotiate what looks like a competitive rate, switch providers, and then six months later your effective processing cost is right back where it started. Or higher. The problem isn’t your negotiation skills. It’s that you’re optimizing the wrong layer of the stack. Most eCommerce businesses don’t have a processing cost problem. They have a visibility problem, and no amount of rate shopping fixes what you can’t see.

The Rate Shopping Trap Everyone Falls Into

The conventional playbook for reducing B2B processing costs goes like this: benchmark your rates, call your processor, threaten to leave, get a basis-point concession, repeat annually. It’s logical. It feels productive. And for a long time, it worked well enough.

But the payments industry has evolved. Pricing structures have gotten more layered. Interchange categories alone number in the hundreds. Assessment fees shift. PCI compliance charges appear. Batch fees, statement fees, and “technology” fees stack up in places most managers never audit. The headline rate you negotiated? It might represent 30% of what you actually pay per transaction.

Rate negotiation became the default strategy because it’s the most visible lever. But visibility into one number isn’t the same as visibility into your entire cost structure. And that gap is where margin disappears.

The Real Thesis: You Can’t Cut What You Can’t Reconcile

Here’s what we believe: chasing lower rates without fixing reconciliation just moves the leak. The businesses that actually control their processing costs aren’t the ones with the best-negotiated rates. They’re the ones with system-level visibility into every line item on every statement, every month, without exception.

A transparent pricing model and automated reconciliation aren’t cost-cutting tactics. They’re infrastructure decisions. And the distinction matters enormously.

Automated reconciliation is not an accounting convenience. It is a visibility system for protecting margin.

Where the Money Actually Goes (and Why You Can’t Find It)

Let’s trace the problem. A mid-market eCommerce business processing $2M monthly in B2B orders might have an advertised rate of 2.4%. That sounds manageable. But when you pull the actual statement apart, you find interchange downgrades on transactions that should have qualified at Level 2 or Level 3 data rates, adding 50 to 100 basis points per transaction. You find PCI non-compliance fees that nobody flagged. You find batch fees charged daily instead of monthly.

None of these show up in the rate you negotiated. All of them show up in your effective processing rate.

Federal Reserve Small Business Survey data continues to show that operational efficiency and cash flow visibility remain major concerns for growing businesses. When reconciliation processes remain manual, discrepancies compound undetected and effective processing costs drift upward over time.

Consider interchange qualification. On B2B and high-ticket orders, submitting Level 2/3 transaction data (tax amounts, line-item detail, customer codes) can meaningfully reduce interchange fees. But here’s the catch: your processor might claim they support Level 2/3 optimization, while your transactions consistently downgrade to standard commercial rates. Without automated reconciliation that flags those downgrades transaction by transaction, you’d never know. You’d just see a slightly higher effective rate and assume that’s the cost of doing business.

This is the pattern we see repeatedly. The leak isn’t in the rate. It’s in the gap between the rate you were quoted and the rate you’re actually charged, multiplied across thousands of transactions per month.

Modern Treasury payment operations resources continue to emphasize how automation improves reconciliation accuracy, operational visibility, and settlement monitoring across high-volume payment environments.

Volume-Based Pricing Tiers Aren’t Automatic Savings

Another common assumption: as your volume grows, your costs naturally decrease through volume-based pricing tiers. In theory, yes. In practice, many processors don’t proactively move you into lower tiers when your volume qualifies. You have to ask. You have to prove it. And you have to catch the month they don’t apply it.

This is another place where automated reconciliation pays for itself. Not by finding one dramatic overcharge, but by catching dozens of small ones that compound into real money over a fiscal year. A business processing $2M monthly that’s overpaying by even 15 basis points due to qualification failures and unapplied tier adjustments is losing $36,000 annually. That’s not a rounding error. That’s a headcount. Merchant Payments Coalition resources continue to highlight how interchange complexity and hidden fee structures create ongoing cost pressure for merchants processing significant transaction volume.

Partners like BAMS address this by combining interchange-plus pricing with dedicated account management that actively monitors qualification rates and fee structures, so the transparent pricing model you signed up for is the one you actually experience month over month. It’s a different philosophy: instead of promising the lowest rate, ensure the rate you’re quoted is the rate you pay.

What Changes If This Is Right

If the real cost problem is visibility, not rates, then several common strategies need rethinking. Annual rate renegotiations become less important than monthly statement audits. Switching processors becomes less urgent than implementing effective rate calculations that capture your true cost per transaction.

It also means that the businesses gaining the most ground right now aren’t the ones with the flashiest fintech integrations. They’re the ones who’ve built reconciliation into their operational rhythm, catching downgrades, verifying tier placement, and flagging fee creep before it compounds.

For eCommerce managers at companies with 10 to 50 employees, this is particularly acute. You’re big enough that basis-point differences represent real dollars, but lean enough that nobody’s full-time job is auditing processor statements. The cost of not seeing is proportionally higher for you than for anyone else.

A Better Mental Model: Pricing as Plumbing

Stop thinking of your processing rate as a price tag. Start thinking of it as plumbing. A price tag is static. You see it, you evaluate it, you accept it. Plumbing is a system. It has joints, valves, and pressure points. It can leak in places you don’t inspect. And a leak you don’t find costs more over time than a higher-priced system that doesn’t leak at all.

The businesses that control their processing costs treat pricing transparency and automated reconciliation the way they treat inventory management or fraud prevention: as infrastructure that runs continuously, not a negotiation that happens once a year.

A lower rate with hidden fees in merchant services will always cost more than a fair rate with full visibility. Always.

Most eCommerce businesses focus on the rate they negotiated instead of the system leaking margin behind it.

The Uncomfortable Truth About “Savings”

Most eCommerce businesses have already been sold on savings. They’ve switched processors, negotiated rates, maybe even explored ACH payment processing for certain order types. And yet the effective rate keeps drifting upward.

That drift isn’t a mystery. It’s the predictable result of optimizing a number while ignoring the system that produces it. Fix the system. The number takes care of itself.

Frequently Asked Questions

What are the common hidden fees in merchant services that businesses should watch out for?

The most common culprits are PCI non-compliance fees, batch processing fees, statement fees, and interchange downgrades on transactions that should qualify at lower rates. These rarely appear in your quoted rate but consistently inflate your effective processing cost.

How can companies effectively reduce their merchant service charges?

Focus less on negotiating headline rates and more on ensuring every transaction qualifies at the correct interchange level, particularly through Level 2/3 data submission on B2B orders. Pair that with automated reconciliation so you catch discrepancies monthly, not annually.

What is interchange-plus pricing and how does it work?

Interchange-plus separates the actual interchange fee (set by card networks) from your processor’s markup, so you see exactly what each party charges. It’s the most transparent pricing model available and makes it far easier to audit whether you’re being charged correctly.