Cost-Elimination Models: ACH vs. Card for B2B Orders

How to route high-ticket transactions off card networks and reclaim per-order margin structurally

Learn which B2B and high-ticket orders belong on ACH instead of card networks, how to calculate per-transaction savings, and how to build routing logic that cuts processing costs without disrupting checkout or cash flow.

TL;DR

- Not every transaction belongs on a card network — B2B and high-ticket orders processed on card rails pay percentage-based fees that scale with order value. Routing these to ACH (flat-fee, bank-to-bank transfers) can cut per-transaction costs from $125 to under $3 on a $5,000 order.

- Audit your transaction mix first — Segment your orders by value and buyer type. Most mid-market eCommerce businesses find that 10% to 20% of transactions generate 40% to 60% of total processing fees. That concentration is your savings opportunity.

- Verify Level 2/3 data qualification on remaining card transactions — Many processors claim to support Level 2/3 optimization but don’t consistently submit the data. Ask for qualification reports. Proper submission can reduce interchange by 0.3% to 0.9% per B2B card transaction.

- Implement conditional routing at checkout — Present ACH as the default for logged-in wholesale accounts and orders above your value threshold. Keep cards available for consumer and low-value orders where convenience matters more than fee savings.

- Measure monthly and watch for drift — Track effective rate by payment method, total fees, and ACH adoption rate. Interchange rates change twice a year, and processors adjust ancillary fees without fanfare. Monthly reviews prevent cost creep from eroding your gains.

Guide Orientation: What This Covers and Who It’s For

This guide maps a specific cost-elimination model for eCommerce businesses processing B2B and high-ticket orders: routing qualifying transactions off card networks and onto ACH payment processing. You’ll learn which order types are candidates for this shift, how to quantify the transaction cost savings per order, and what infrastructure changes are required to make it work without disrupting your checkout or cash flow.

This is written for eCommerce managers at established online businesses (roughly 10 to 50 employees) who already process a meaningful volume of B2B orders alongside their direct-to-consumer sales. If you’re paying interchange on every transaction regardless of size or buyer type, this guide will show you where that’s costing you the most and how to fix it structurally.

By the end, you’ll be able to audit your current transaction mix, identify orders better suited to ACH, calculate realistic savings per transaction, and build a routing logic that reduces per-order costs without slowing down settlement. We won’t cover enterprise treasury management, multi-acquirer strategies, or wholesale platform migrations. This is about one high-leverage fix you can implement with your existing payment infrastructure.

Why Eliminating Hidden Processing Costs Matters Now

Routing high-value B2B orders through ACH instead of card networks can significantly reduce payment processing costs and recover lost margin.

U.S. enterprise SG&A costs have climbed to 14.3% of revenue, the highest level in five years. For mid-market eCommerce businesses, payment processing fees are one of the largest line items inside that overhead. Yet most managers treat processing costs as fixed, accepting whatever rate their processor quotes without examining whether every transaction type actually needs to travel the same (expensive) rails.

The pressure to cut costs is real. 69% of companies reported a major cost reduction initiative in recent years, up from 65% the year prior. But ambition doesn’t equal execution. BCG found that companies achieved only 48% of their cost-saving targets on average, and those that missed their targets underperformed peers on total shareholder return by 9 percentage points. The pattern is clear: broad cost-cutting programs underdeliver. Tightly targeted, structural fixes are what actually move the number.

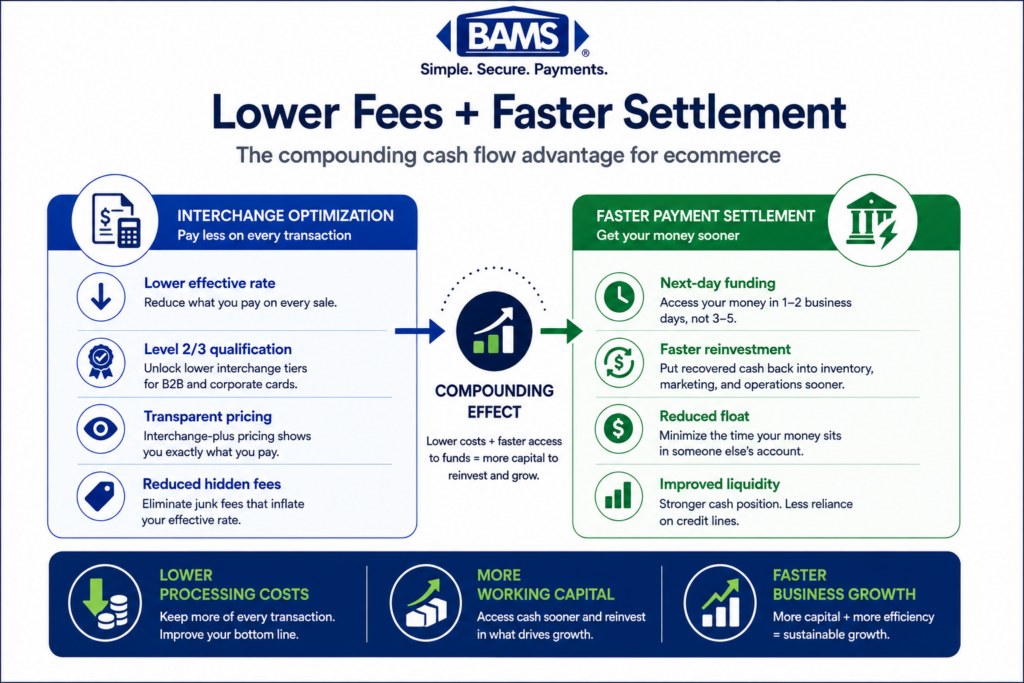

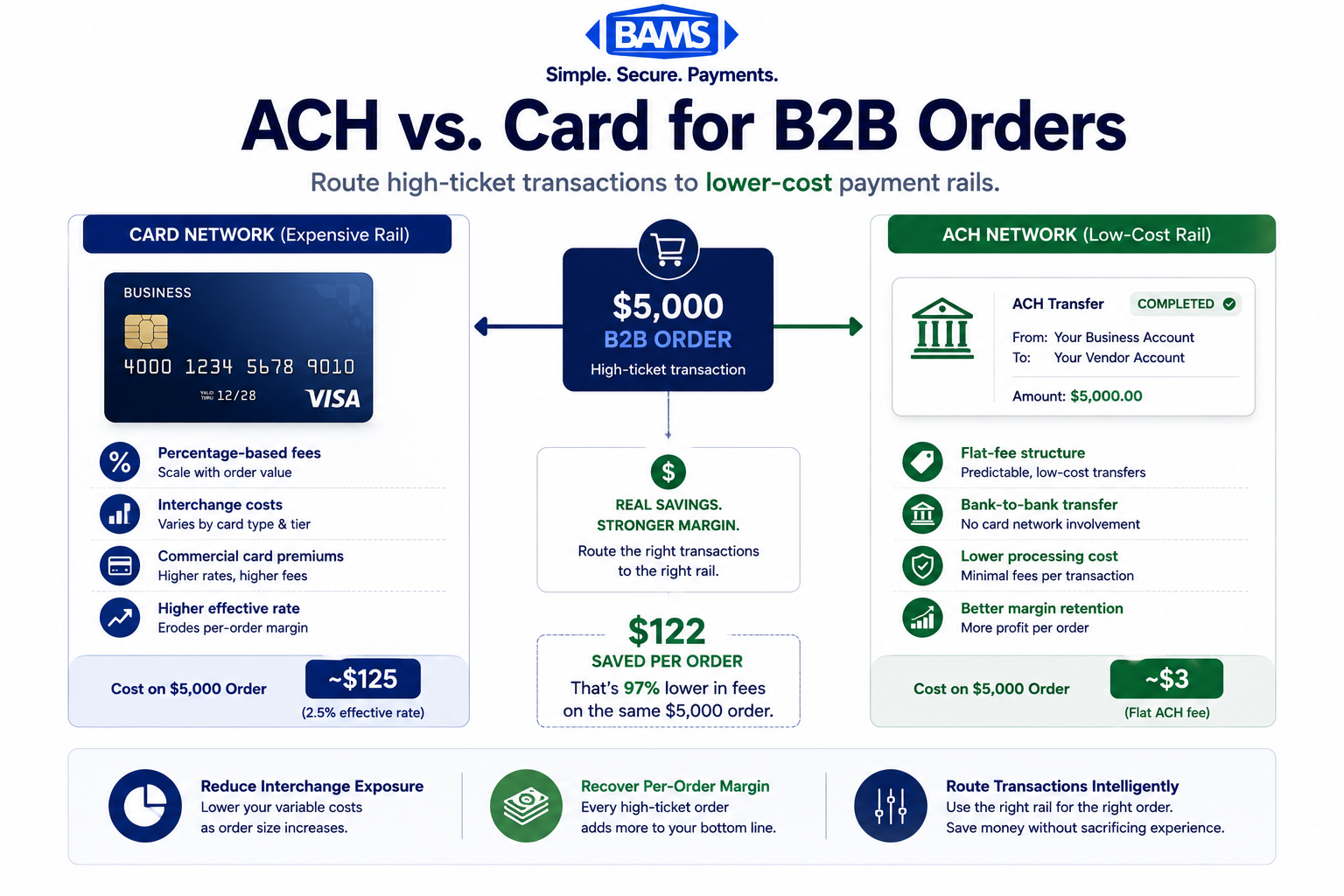

For eCommerce businesses running B2B orders on card networks, the fix is specific and measurable. A $5,000 wholesale order processed on a credit card at a 2.5% effective rate costs $125 in fees. That same order routed through ACH might cost $0.50 to $3.00. When you multiply that gap across hundreds of qualifying orders per month, you’re looking at margin recovery that compounds every cycle. This isn’t an optional upgrade. It’s a structural fix to per-transaction margin erosion that most mid-market businesses simply haven’t addressed yet.

Core Concepts: Payment Rails, Interchange, and ACH Payment Processing

Card Networks vs. ACH: Two Different Cost Structures

Every electronic payment travels on a “rail,” which is the network infrastructure that moves money from buyer to seller. Card networks (Visa, Mastercard, Amex) charge percentage-based fees on every transaction, typically 1.5% to 3.5% depending on card type, transaction data, and risk profile. ACH (Automated Clearing House) is a bank-to-bank transfer network that charges flat fees, usually between $0.20 and $5.00 per transaction regardless of order size.

This distinction is the entire leverage point. Percentage-based fees scale with order value. Flat fees don’t. On a $50 consumer order, the difference is negligible. On a $5,000 B2B order, it’s the difference between $125 and $3.

Nacha ACH Network resources explain how ACH transfers operate on a bank-to-bank settlement model with lower transaction costs compared to percentage-based card network pricing.

Interchange and Why It Inflates B2B Costs

Interchange is the fee the card-issuing bank charges on every card transaction. It’s the largest component of your credit card processing fees, typically 70% to 80% of the total. For B2B transactions specifically, interchange rates are often higher because commercial cards carry elevated risk profiles and reward structures. Unless your processor submits Level 2 or Level 3 transaction data (line-item detail, tax amounts, customer codes), your B2B card transactions default to the highest interchange tier. Many processors claim to support Level 2/3 optimization but don’t actually submit the data consistently.

The Hidden Fee Layer

Beyond interchange, most businesses underestimate their true processing costs by 20% to 40%. Assessment fees, PCI compliance charges, card-not-present premiums, and batch fees accumulate quietly on monthly statements. These fees apply to every card transaction. When you move qualifying orders to ACH, you eliminate the entire fee stack for those transactions, not just the interchange component.

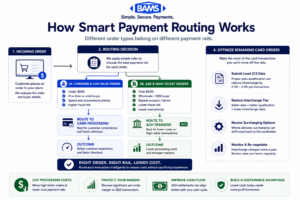

The Cost-Elimination Framework: Route by Order Type, Not by Default

The framework here is straightforward. Instead of routing every transaction through your card processor by default, you evaluate each order against three criteria and route it to the lowest-cost rail that still meets your settlement and buyer-experience requirements.

The framework has four stages:

- Audit — Analyze your current transaction mix to identify which orders are high-ticket, repeat, or B2B

- Qualify — Determine which of those orders are candidates for ACH based on buyer type, order value, and payment timing tolerance

- Route — Implement payment-method logic that steers qualifying orders to ACH while keeping consumer and low-value orders on cards

- Measure — Track effective rate by payment method monthly to verify savings and catch drift

Each stage builds on the previous one. Skipping the audit and jumping straight to implementation is the most common reason this kind of initiative underdelivers. You need to know your numbers before you change your routing.

Smart payment routing reduces processing costs by matching high-ticket B2B orders to ACH while keeping consumer transactions on card rails.

Step-by-Step: Eliminating Hidden Fees Through Payment Routing

Step 1: Audit Your Transaction Mix by Order Value and Buyer Type

Objective: Identify exactly how many of your monthly transactions are high-ticket, B2B, or repeat wholesale orders currently running on card rails.

Pull your last three months of processor statements and your eCommerce platform’s order data. Sort transactions into buckets: orders under $500, orders between $500 and $2,000, and orders above $2,000. Then tag each bucket by buyer type: consumer (one-time or DTC), repeat business buyer, or wholesale/B2B account.

What you’re looking for is concentration. Most mid-market eCommerce businesses discover that 10% to 20% of their transactions account for 40% to 60% of their total processing fees. These are the high-value B2B orders where percentage-based card fees do the most damage. A $3,000 order at a 2.8% effective rate generates $84 in fees. That same order on ACH costs a flat $1 to $3.

Anti-patterns: Don’t average your effective rate across all transactions. The average hides the problem. A blended 2.2% rate looks reasonable until you realize your B2B orders are running at 2.9% while your consumer orders sit at 1.8%. Also avoid relying solely on your processor’s reporting. Cross-reference with your platform data to catch transactions that may be miscategorized.

Success indicator: You have a clear dollar figure for total monthly fees paid on orders above $500 from repeat or B2B buyers. This is your addressable savings pool.

Step 2: Calculate Your Effective Rate on B2B Transactions Specifically

Objective: Determine the true per-transaction cost on your highest-value orders, including all hidden fee layers.

Your effective processing rate is total fees divided by total volume. But you need this number segmented, not blended. Take the B2B and high-ticket orders you identified in Step 1 and calculate their effective rate separately. Pull the interchange charges, assessment fees, processor markup, and any per-transaction fees from your statement for those specific transactions.

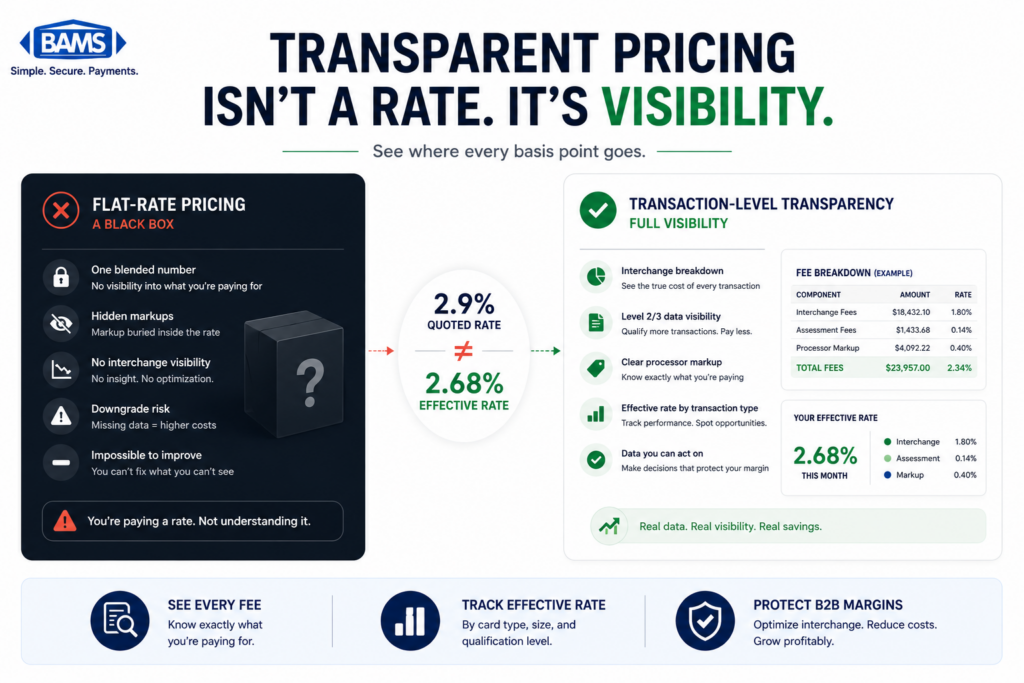

If your processor uses tiered pricing rather than interchange-plus, this calculation becomes harder because tiered models bundle costs opaquely. In that case, request a detailed breakdown or consider switching to interchange-plus pricing as a prerequisite to this entire optimization. You can’t fix what you can’t see.

For B2B card transactions specifically, check whether your processor is actually submitting Level 2/3 data. Ask them directly: “What percentage of my commercial card transactions qualified at Level 3 last month?” If they can’t answer with a specific number, they’re likely not optimizing your interchange qualification. This alone can mean you’re paying 0.3% to 0.5% more per transaction than necessary on every B2B card order.

Anti-patterns: Don’t accept your processor’s headline rate as your actual cost. The quoted rate excludes assessments, PCI fees, and transaction-level surcharges. Don’t skip the Level 2/3 verification. Many processors advertise this capability without consistently delivering it.

Success indicator: You have a documented effective rate for B2B transactions that includes all fee components, and you know whether your commercial card transactions are qualifying at Level 3.

Step 3: Identify Which Orders Qualify for ACH Routing

Objective: Build a clear decision framework for which transactions should move to ACH and which should stay on card rails.

Not every order belongs on ACH. The decision depends on three factors: order value, buyer relationship, and settlement timing tolerance. Here’s the routing logic:

- Order value above $500 from a known B2B buyer: Strong ACH candidate. The fee savings are material and the buyer likely prefers bank transfer anyway.

- Recurring wholesale orders at any value: Strong ACH candidate. Predictable orders from established accounts carry low risk and high routing efficiency.

- One-time consumer orders under $500: Keep on card. The convenience and buyer protection expectations of consumer transactions outweigh the small fee difference.

- High-ticket consumer orders (over $1,000): Evaluate case by case. Some consumers will accept ACH for large purchases if you offer a small discount or faster shipping incentive.

The key consideration is settlement timing. ACH transactions typically settle in 1 to 3 business days. If your business depends on next-day access to funds, you’ll want a processor that offers accelerated settlement on ACH. BAMS, for example, provides next-day funding that applies across payment methods, which removes the cash flow penalty that sometimes discourages businesses from adopting ACH for high-value orders.

Anti-patterns: Don’t try to force every transaction onto ACH. Consumer buyers expect card payment options, and removing them creates friction that costs you conversions. Don’t ignore chargeback dynamics either. ACH disputes follow different rules than card chargebacks, which can be an advantage for B2B sellers dealing with friendly fraud.

Success indicator: You have a written routing policy that specifies which order types go to ACH and which stay on cards, with clear thresholds for value, buyer type, and exceptions.

Step 4: Implement Payment Method Routing at Checkout

Objective: Configure your payment infrastructure to present and process the right payment method for each order type without adding friction.

Implementation depends on your platform. Most modern eCommerce platforms (Shopify Plus, WooCommerce, BigCommerce Enterprise) support multiple payment methods at checkout. For B2B buyers, you can present ACH/bank transfer as the default or preferred option, with card as a fallback. For wholesale portals or invoice-based ordering, you can make ACH the only option for orders above your threshold.

The technical setup typically involves three components: enabling ACH acceptance through your payment processor, configuring conditional payment method display at checkout (showing ACH prominently for logged-in wholesale accounts), and setting up automated reconciliation so ACH payments match to orders in your system without manual intervention.

If you’re on Shopify and already dealing with elevated transaction fees on refunds, adding ACH routing for B2B orders addresses two cost problems simultaneously: lower processing fees on the initial sale and no card-network fee retention on returns.

Anti-patterns: Don’t bury the ACH option below card fields at checkout. If it’s not visible and clearly labeled (“Pay by bank transfer and save”), adoption will be minimal. Don’t implement without testing the full cycle: order placement, payment confirmation, settlement, and reconciliation. Broken reconciliation creates more cost in manual labor than you save in fees.

Success indicator: B2B buyers can complete ACH payments through your standard checkout flow, payments settle on schedule, and orders reconcile automatically in your system.

Step 5: Optimize Remaining Card Transactions with Level 2/3 Data

Objective: Reduce interchange costs on the card transactions that can’t move to ACH by ensuring they qualify at the lowest possible interchange tier.

Even after routing qualifying orders to ACH, you’ll still process card transactions. For those remaining B2B card payments, Level 2 and Level 3 data submission is the next cost-elimination lever. Level 2 data includes customer code, tax amount, and merchant postal code. Level 3 adds line-item detail: product descriptions, quantities, unit costs, and freight amounts.

When your processor submits this data with each transaction, the card networks recognize it as lower-risk and assign a lower interchange rate. The savings range from 0.3% to 0.9% per transaction depending on card type and network. On a $2,000 order, that’s $6 to $18 saved per transaction, just from passing data you already have in your order management system.

The challenge is verification. Ask your processor to provide a monthly report showing what percentage of your commercial card transactions qualified at Level 2 and Level 3. If the number is below 80%, either your processor isn’t submitting the data correctly or your system isn’t passing the required fields. This is a fixable integration issue, not a fundamental limitation.

Visa payment processing resources explain how enhanced transaction data improves qualification handling and authorization transparency for commercial card payments.

Anti-patterns: Don’t assume Level 2/3 is automatic. It requires specific data fields to be populated and transmitted with each authorization. Don’t accept “we support Level 3” without seeing qualification reports. The gap between capability and execution is where money disappears.

Success indicator: Your monthly statement shows 80%+ of commercial card transactions qualifying at Level 3, and your effective rate on those transactions has dropped measurably.

Step 6: Measure and Maintain Your Savings Monthly

Objective: Build a recurring review process that tracks actual savings, catches fee drift, and prevents cost creep from eroding your gains.

Create a simple monthly dashboard with three metrics: total processing fees (absolute dollars), effective rate by payment method (card vs. ACH), and percentage of B2B volume routed to ACH. Compare each month against your pre-optimization baseline from Step 1.

Fee drift is real. Card networks adjust interchange rates twice a year (April and October). Processors sometimes add or increase ancillary fees without prominent notification. Your monthly review should include a line-by-line scan of your statement for new or changed fees. If you spot something unfamiliar, call your processor and ask for an explanation. Transparency in pricing is a baseline expectation, not a premium feature.

Also track ACH adoption rate among your B2B buyers. If adoption stalls below your target, the issue is usually checkout UX or buyer communication. Consider adding a visible savings incentive (“Save 2% when you pay by bank transfer”) or reaching out to your top 20 wholesale accounts directly to walk them through the process.

Anti-patterns: Don’t set up the routing and then stop monitoring. Cost structures change, transaction mixes shift, and processors adjust fees. A quarterly review is the minimum; monthly is better. Don’t ignore small fee increases. A $0.02 per-transaction increase across 5,000 monthly transactions is $1,200 per year.

Success indicator: You have a documented month-over-month trend showing reduced effective rates and can attribute specific dollar savings to your ACH routing and Level 2/3 optimization.

Practical Example: The $12,000 Monthly Savings You’re Not Capturing

Consider a mid-market eCommerce business processing $400,000 in monthly volume. Of that, $150,000 comes from B2B wholesale orders averaging $2,500 each (60 orders per month). The remaining $250,000 is consumer DTC orders averaging $85.

Before optimization, every transaction runs on card rails at a blended effective rate of 2.6%. Total monthly processing fees: $10,400. The B2B orders alone generate $3,900 in fees (60 orders × $2,500 × 2.6%).

After implementing the routing framework above, 50 of those 60 B2B orders move to ACH at $2.50 per transaction. The remaining 10 B2B card transactions now qualify at Level 3, dropping their effective rate to 1.9%. Here’s the new math:

- 50 ACH orders: 50 × $2.50 = $125 (down from $3,250)

- 10 remaining B2B card orders: 10 × $2,500 × 1.9% = $475 (down from $650)

- DTC card orders (unchanged): $250,000 × 2.6% = $6,500

- New total: $7,100 per month

That’s $3,300 saved per month, or $39,600 annually, from a structural change that took two to four weeks to implement. The savings compound because they apply to every future transaction without ongoing effort. Organizations that surface spend patterns at this level of detail, as procurement automation platforms have demonstrated, consistently find that payment-method misalignment is one of the most addressable sources of unnecessary cost.

Common Mistakes and Pitfalls

Treating all transactions identically. The single biggest mistake is running every order through the same payment rail. A $50 consumer order and a $5,000 wholesale order have completely different cost profiles, and treating them the same leaves money on the table every month.

Trusting your blended rate. Your average effective rate masks the problem. You need segmented rates by transaction type and payment method. If you only look at the blended number, you’ll never see where the real cost concentration lives.

Assuming your processor handles Level 2/3 automatically. Many processors advertise Level 2/3 support but don’t consistently submit the data. Verify with qualification reports, not marketing claims.

Ignoring buyer communication. ACH routing only works if buyers use it. If you add the option without explaining the benefit to your wholesale accounts, adoption will be low. A direct email to your top accounts explaining the change (and any pricing incentive) dramatically improves uptake.

Setting and forgetting. Payment costs shift. Interchange rates change, processors adjust fees, and your transaction mix evolves. Build a monthly review into your operations calendar or the savings will erode quietly.

What to Do Next

Start with the audit. Pull your last three months of statements and sort your transactions by value and buyer type. Calculate the effective rate on your B2B orders separately from your consumer orders. That single exercise will tell you whether this optimization is worth $500 a month or $5,000.

If the number is meaningful (and for most businesses processing $100K+ monthly with a B2B component, it will be), take the routing framework one step at a time. Qualify your ACH candidates, configure the payment method at checkout, and measure the results after 30 days. You don’t need to overhaul your entire payment stack. You need to route the right orders to the right rails.

Federal Reserve payment systems resources also highlight the continued growth of faster payment infrastructure and electronic bank transfer adoption across U.S. businesses.

Revisit this guide as your transaction mix changes. What qualifies for ACH today might expand as you add more wholesale accounts or as instant payment adoption continues to grow. The framework stays the same. The thresholds evolve with your business.

Frequently Asked Questions

What is interchange-plus pricing and how does it work?

Interchange-plus pricing separates your processing costs into two transparent components: the interchange fee set by the card network (which your processor cannot control) and a fixed markup charged by your processor. This model gives you visibility into exactly what you’re paying and why. It’s the opposite of tiered pricing, which bundles costs into opaque categories that make it nearly impossible to identify overcharges. For any business serious about cost optimization, interchange-plus is the baseline requirement for transparency.

Why should businesses consider Level 2/3 optimization for B2B transactions?

Level 2 and Level 3 data submission tells the card network that a transaction is lower-risk by providing detailed purchase information (tax amounts, line items, customer codes). In return, the network assigns a lower interchange rate. For B2B transactions on commercial cards, this can reduce interchange by 0.3% to 0.9% per transaction. On a $5,000 order, that’s $15 to $45 saved from a single data submission. The data already exists in your order management system. It just needs to be passed through to your processor correctly.

How can companies effectively reduce their merchant service charges?

The most effective approach is segmenting your transactions by type and routing each to the lowest-cost payment rail. High-ticket B2B orders should move to ACH where possible. Remaining card transactions should qualify at Level 2/3 for lower interchange. Beyond routing, audit your statements monthly for hidden fees like PCI non-compliance charges, batch fees, and card-not-present premiums. Finally, ensure you’re on interchange-plus pricing so you can actually see what you’re paying at the transaction level.

When is the best time to negotiate processing fees with your merchant services provider?

The best time is when you have data. Complete the audit described in this guide so you know your effective rate by transaction type, your Level 2/3 qualification rate, and your total addressable savings. Processors respond to informed merchants differently than they respond to general complaints about rates. Also consider negotiating after a volume increase, as higher processing volume gives you more leverage. If your processor can’t match competitive rates or provide transparent reporting, that’s your signal to evaluate alternatives.

What are the common hidden fees in merchant services that businesses should watch out for?

The most common hidden fees include: PCI non-compliance fees (charged monthly if you haven’t completed your PCI questionnaire), statement fees, batch processing fees, card-not-present surcharges, monthly minimum fees, and early termination fees. Some processors also charge “downgrade” fees when transactions don’t qualify at the expected interchange tier, which is often the processor’s fault for not submitting proper data. Review every line on your monthly statement and question anything you don’t recognize.

Which payment processing model is more cost-effective for high-volume transactions?

For high-volume businesses, interchange-plus pricing almost always wins because it passes the actual interchange rate through to you with a small, fixed markup. Tiered pricing bundles transactions into qualified, mid-qualified, and non-qualified categories with inflated margins on the latter two. At high volumes, even a 0.1% difference in markup compounds into thousands of dollars annually. Pair interchange-plus pricing with ACH routing for qualifying B2B orders, and you’ll achieve the lowest possible effective rate across your entire transaction mix.

Sources

- Nacha ACH Network Resources

- Federal Reserve Payment Systems Resources

- Visa Payment Processing Resources